-450x250h.webp)

-150x150h.webp)

Home Textiles & Soft Furnishings: Inside the $140 Billion Market Redefining Modern Living in 2026

Table of Contents

The global Home Textiles & Soft Furnishings industry serves consumers worldwide with diverse solutions.

1. Industry Overview

The global home textiles and soft furnishings market will exceed $140 billion in 2026, a figure that represents far more than mere décor spending—it signals a fundamental shift in how consumers prioritize their living spaces. After years of peripheral importance, soft furnishings have emerged as a primary driver of interior design identity, with sofa covers, curtain systems, and layered textiles now accounting for a significant share of household furnishing budgets worldwide. This transformation accelerated during the post-2020 era when remote work and extended home occupancy compelled consumers to invest heavily in comfort, aesthetics, and functional textile solutions. The industry, which includes products ranging from basic cushion covers to sophisticated blackout curtain systems, has responded with unprecedented innovation in materials, customization options, and sustainable manufacturing processes. Market researchers now predict this momentum will sustain, with the broader home furnishing sector projected to reach $2.15 trillion by 2033, up from $1.11 trillion in 2026, reflecting a compound annual growth rate that outpaces many traditional manufacturing sectors.

Industry Scope & Characteristics

Broad Product Portfolio

Products span sofa covers, cushion covers, curtains, blinds, bedspreads, throws, carpets, rugs, wall hangings, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

What distinguishes this industry is its unique position at the intersection of manufacturing excellence and design sensibility. Unlike rigid furniture categories, soft furnishings allow consumers to refresh their environments seasonally without major expenditure, creating a recurring demand cycle that benefits both manufacturers and retailers. The supply chain spans continents, with raw material production concentrated in South Asia, manufacturing hubs across Southeast Asia and Eastern Europe, and premium design capabilities centralized in Scandinavia, Japan, and Western Europe. This global complexity creates both opportunities and vulnerabilities, as shipping disruptions, raw material price fluctuations, and evolving trade policies continuously reshape competitive dynamics. The $137.81 billion valuation recorded in 2025 has already set a new baseline, and with projected growth to $231.40 billion by 2033 at a CAGR of 6.9%, the industry offers substantial opportunity for informed market entrants and established players alike.

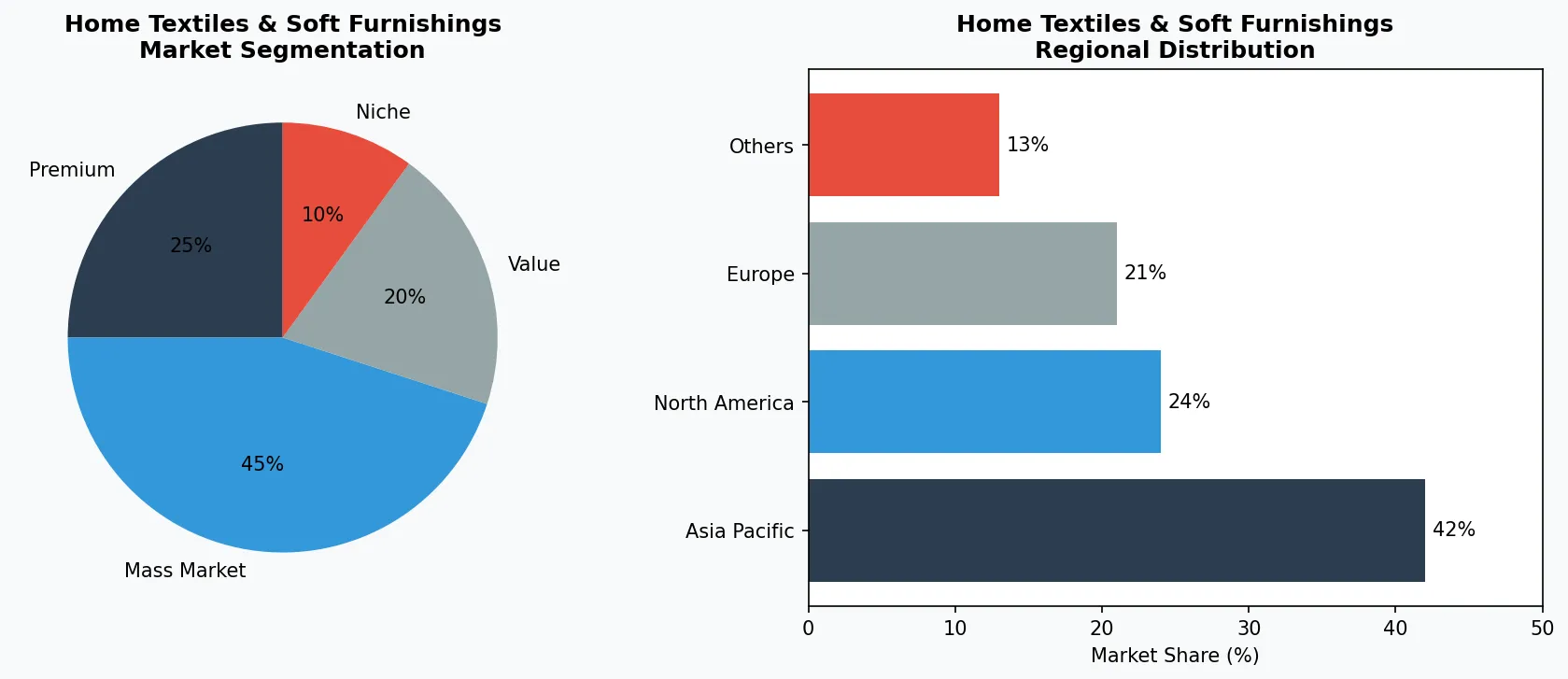

Key market segments and growth drivers in the Home Textiles & Soft Furnishings sector.

2. Market Analysis

The home textiles market reached $137.81 billion in 2025 and stands poised to breach $231.40 billion by 2033, representing a compound annual growth rate of 6.9% that reflects sustained consumer investment in residential comfort and aesthetics. When examining the broader home furnishing landscape, the numbers become even more striking: the global market is expected to expand from $1.11 trillion in 2026 to $2.15 trillion by 2033, achieving a 9.9% CAGR that positions soft furnishings as one of the fastest-growing segments within the larger home goods ecosystem. Three primary drivers fuel this expansion: rising disposable incomes across developing economies, the continued normalization of home-centric lifestyles in post-pandemic markets, and the growing demand for sustainable and hypoallergenic textile solutions.

Geographically, North America and Europe remain the largest consuming markets by average spend per capita, with American households allocating increasing portions of furnishing budgets to premium curtain systems, washable rug innovations, and customizable upholstery solutions. The Asia-Pacific region, however, represents the most dynamic growth corridor, with China, India, and Southeast Asian markets experiencing double-digit expansion rates as urbanization accelerates and middle-class populations expand. The Chinese market deserves particular attention: its appetite for both domestically manufactured products and imported premium brands has transformed it into the world's largest home textiles consumer, with local e-commerce platforms like Tmall and JD.com reporting year-over-year growth rates exceeding 20% for soft furnishing categories. Meanwhile, the Middle East and Africa region is emerging as an unexpected growth hotspot, driven by construction booms in Saudi Arabia, the UAE, and Nigeria that are generating sustained demand for residential soft furnishings across all price points.

Within the market, segmentation reveals distinct growth patterns. The curtain and blinds subcategory commands the largest share, driven by functional demands for light control and privacy alongside aesthetic considerations. Bedding textiles, while substantial, have experienced relatively slower growth as market saturation increases in developed markets. The standout performer is decorative accessories—cushion covers, throws, and wall hangings—which have benefited from the layered interiors trend that encourages consumers to accumulate multiple textile elements rather than replacing single statement pieces. Industry analysts note that this fragmentation of demand across subcategories has compelled manufacturers to diversify their portfolios, with successful players maintaining capabilities across at least three distinct product families to capture cross-selling opportunities and reduce seasonal dependency.

Market segmentation and regional distribution analysis for Home Textiles & Soft Furnishings.

3. Product Categories

Sofa Covers and Upholstery Solutions represent the largest value category within soft furnishings, driven by consumer demand for furniture refreshment without full replacement costs. The market has responded with increasingly sophisticated offerings, including stretch-fit covers compatible with modular sofa systems, water-resistant fabrics designed for households with children or pets, and seasonal collections that allow consumers to update their living spaces quarterly. Major retailers like IKEA have expanded their upholstery accessory lines significantly, recognizing that covers represent both a sales opportunity and a customer retention mechanism—consumers who purchase initial furniture pieces return repeatedly for complementary covers and accessories. The subcategory also benefits from the growing rental furniture market, where tenants require reversible solutions that protect existing furnishings while allowing personalization within landlord restrictions.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Window Treatment Systems encompass an expanding range of products beyond traditional curtains and blinds. The blackout curtain segment has achieved particular prominence, with manufacturers developing triple-weave fabrics that achieve complete light blocking without the chemical coatings that previously limited washability and longevity. Motorized and smart curtain systems represent a premium subsegment, with companies like IKEA's TRÅDFRI ecosystem and third-party manufacturers offering app-controlled rail systems that integrate with home automation platforms. These smart window treatments have found particular traction in bedrooms and media rooms, where precise light control enhances sleep quality and viewing experiences. The market has also witnessed innovation in sustainable window treatments, with manufacturers developing curtains made from recycled ocean plastics and organic cotton that appeal to environmentally conscious consumers willing to pay premium prices for responsible production.

Rugs, Carpets, and Washable Floor Textiles constitute a category transformed by manufacturing advances in machine-washable construction and sustainable fiber development. Traditional area rugs required professional cleaning and careful maintenance, factors that limited adoption in high-traffic households and rental properties. The introduction of machine-washable rug technologies—featuring detachable backing systems and quick-dry constructions—has democratized floor textiles, with brands like Ruggable pioneering direct-to-consumer models that have disrupted established retail channels. Contemporary washable rugs incorporate antimicrobial treatments and stain-resistant finishes that extend product lifespans while reducing maintenance requirements, addressing one of the primary barriers to purchase that historically limited market expansion. The category has also benefited from the layered rug trend, which encourages consumers to layer smaller accent rugs over larger foundation pieces, effectively doubling per-household purchase volume.

4. Leading Players

IKEA maintains its position as the dominant global force in accessible home textiles, leveraging its vertically integrated supply chain to offer products at price points that competitors struggle to match while simultaneously expanding its premium offerings to capture higher-margin segments. The Swedish retailer's strategy in soft furnishings centers on volume-driven design iteration, with the company releasing seasonal collections that refresh aesthetic appeal without requiring fundamental manufacturing changes. Recent moves include significant investment in sustainable materials, with commitments to phase out virgin petroleum-based synthetics from textile production by 2030. IKEA's proprietary curtain systems, including its expanding motorized and smart lighting integration options, demonstrate how the company uses soft furnishings as entry points to broader smart home ecosystems, creating customer lock-in that extends beyond individual product transactions.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the home textiles & soft furnishings space.

MUJI pursues an antithetical market position, emphasizing minimalism, natural materials, and understated design that appeals to consumers seeking alternatives to mass-market aesthetic uniformity. The Japanese retailer's soft furnishing strategy focuses on tactile quality and material authenticity, with products featuring unbleached organic cotton, natural linen, and traditional weaving techniques that justify premium pricing. MUJI's approach to market expansion prioritizes selective presence in upscale retail environments and strategic e-commerce partnerships rather than aggressive geographic scaling. This positioning has proven particularly effective in urban markets with high concentrations of design-conscious consumers, where the brand's restraint and quality perception generate strong customer loyalty despite limited product variety compared to competitors like IKEA.

Zarahome, the Spanish retailer's home goods subsidiary, occupies a distinctive niche that combines Mediterranean design sensibilities with rapid trend responsiveness. The company's soft furnishing collections feature bold color palettes and pattern options that differentiate it from Scandinavian competitors' preference for neutral tones, appealing to consumers in Southern European, Latin American, and Middle Eastern markets where decorative expressiveness carries greater cultural weight. Zarahome's product development cycle prioritizes speed to market for emerging trends, with the company reportedly reducing concept-to-shelf timelines to under twelve weeks for fast-moving accessories like cushion covers and throws. This agility enables the company to capitalize on seasonal trends and social media-driven aesthetic movements that require rapid inventory response, a capability that more vertically integrated competitors often lack.

Wendre, operating from Finland with global distribution, specializes in premium bedding and textile products that command some of the highest price points in the industry through uncompromising material quality and craftsmanship positioning. The company's strategy emphasizes Scandinavian sustainability credentials, with products certified across multiple environmental and social responsibility standards that appeal to institutional buyers in hospitality and luxury residential sectors. Wendre's B2B channel—serving hotels, cruise lines, and furnished rental operators—represents a growing share of revenue and provides demand stability that offsets consumer market seasonality. The company's recent investments in digital customization capabilities, enabling corporate clients to order bespoke products in commercial quantities, position it to capture share in the expanding premium hospitality sector across Asia and the Middle East.

5. Market Trends

1. BLACKOUT INNOVATION

BLACKOUT INNOVATION — The demand for complete light control has driven manufacturers beyond simple dark fabrics to develop technologically advanced curtain systems that achieve zero light transmission without chemical coatings. Triple-weave constructions, micro-fiber innovations, and proprietary light-blocking technologies now enable washable blackout curtains that maintain effectiveness after hundreds of laundering cycles. This technical advancement addresses the primary consumer complaint about traditional blackout products—their inability to be effectively cleaned—and has expanded the market beyond bedroom applications to include home theaters, nursery rooms, and shift-worker housing. The trend has compelled major retailers like IKEA to dramatically expand their light-control ranges, with motorized blackout systems representing the fastest-growing subcategory.

2. WASHABLE RUG REVOLUTION

WASHABLE RUG REVOLUTION — Machine-washable area rugs have transformed from niche products to mainstream offerings, with multiple manufacturers entering the category and retail prices declining as production scales. The innovation addresses a fundamental market barrier: traditional rugs required professional cleaning, creating ongoing maintenance costs and limiting adoption in households with children, pets, or high-traffic areas. Modern washable rugs feature detachable designs that allow machine laundering of both face and backing materials, with quick-dry constructions enabling same-day replacement after washing. The trend has proven particularly disruptive in rental housing markets, where tenants can now incorporate area rugs without risk of permanent staining, and in student housing, where furniture restrictions encourage portable textile solutions.

3. SEASONAL TEXTILE ROTATION

SEASONAL TEXTILE ROTATION — The practice of rotating soft furnishings seasonally—swapping heavier throws and curtains for lighter alternatives—has evolved from European tradition to global consumer behavior, driven by social media influence and the democratization of affordable premium textiles. This trend has created a new consumption pattern where consumers purchase twice-yearly rather than once, effectively doubling market volume per household over time. Manufacturers and retailers have responded with coordinated seasonal launches that coordinate with spring cleaning and fall preparation behaviors, with brands like Zarahome and H&M Home leading trend-driven collections that encourage full textile refreshment. The trend particularly benefits smaller accessory categories like cushion covers, where the low individual cost and high visual impact support impulse purchasing behavior.

6. Regional Markets

North America represents the most mature and highest-spending soft furnishings market per capita, characterized by strong preference for practical functionality, sustainable materials, and integrated smart home features. The United States drives regional demand through a combination of housing market activity, renovation spending, and the continued normalization of home-centric lifestyles established during the 2020-2022 period. American consumers demonstrate particular affinity for washable products and easy-care textiles, reflecting busy household schedules and the influence of social media on aesthetic expectations. Major retail chains have responded with expanded soft furnishing square footage, with Target, Walmart, and Wayfair competing aggressively for market share through exclusive collaborations and rapid trend response. The Canadian market, while smaller, shows similar consumption patterns with higher-than-average spending on premium window treatments.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

China's home textiles market has achieved unprecedented scale, with domestic consumption now exceeding the combined totals of Western European markets. The Chinese consumer demonstrates distinctive preferences that diverge significantly from Western norms: strong preference for bold colors and decorative patterns over neutral tones, rapid adoption of smart home-integrated window treatments, and growing enthusiasm for sustainable and organic textile options. Local platforms like Taobao, JD.com, and Pinduoduo have created distribution channels for small-scale manufacturers that supply customized and personalized soft furnishings at price points that challenge both domestic established brands and international competitors. The market's continued expansion depends heavily on residential construction activity and housing turnover, which have shown signs of moderation after years of explosive growth, prompting established players to emphasize renovation and replacement cycles over new installation demand.

The Middle East and Africa region presents exceptional growth potential despite political and economic volatility that creates uneven market conditions across territories. The Gulf Cooperation Council states—Saudi Arabia, the United Arab Emirates, Qatar, and Kuwait—drive premium demand through luxury residential construction, hospitality expansion, and government investment in diversified economies that reduce oil dependency. Saudi Arabia's Vision 2030 initiative has accelerated construction activity that generates sustained demand for soft furnishings across residential, hospitality, and commercial segments. The UAE maintains its position as a regional re-export hub, with Dubai serving as a distribution center for soft furnishings destined for African and Central Asian markets. South Africa represents the region's most developed consumer market, with established retail infrastructure and a growing middle class that demonstrates Western-influenced consumption patterns.

7. Investment Outlook

The home textiles and soft furnishings industry presents two compelling opportunities for strategic players entering or expanding within the market. First, the convergence of smart home technology with window treatment systems represents an underdeveloped category with substantial margin potential. Motorized curtain tracks, app-controlled blinds, and light-sensing automated systems currently command premium pricing that significantly exceeds traditional alternatives, and as smart home ecosystems become standard in new residential construction, demand for integrated textile solutions will likely accelerate. Second, the expansion of rental housing markets globally—driven by changing homeownership patterns among millennials and Generation Z consumers—creates sustained demand for removable, washable, and renter-friendly soft furnishing solutions that traditional furniture categories cannot address. Manufacturers who develop products specifically designed for temporary installations and frequent relocation will capture share from competitors whose offerings assume permanent placement.

The primary risk confronting the industry involves raw material supply chain vulnerability, particularly for cotton and synthetic fiber inputs whose prices have demonstrated extreme volatility over recent years. Climate-related disruptions to cotton production in major growing regions, combined with petroleum price fluctuations affecting synthetic fiber costs, create margin pressure that cannot always be passed to price-sensitive consumers. Additionally, intensifying regulatory scrutiny of textile manufacturing practices—particularly regarding chemical treatments, wastewater discharge, and carbon emissions—will require capital investment from manufacturers that may reshape competitive dynamics by favoring larger players with compliance resources over smaller specialized producers. Companies that proactively address sustainability requirements and establish transparent supply chain documentation will be better positioned to navigate evolving regulatory landscapes while competitors face costly retroactive compliance measures.

Strategic Considerations:

- ('Technology & AI Integration:', 'Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.')

- ('Sustainability as Business Strategy:', 'Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.')

- ('Transparency & Traceability:', 'Consumers demand increasingly granular information about product origins, ingredients, and production methods.')

- ('Emerging Market Penetration:', 'Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.')

Make Informed Decisions in the Home Textiles & Soft Furnishings Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-16. All market figures are estimates and may vary from actual results.