-450x250h.webp)

-150x150h.webp)

Custom Apparel Market Set to Reach $12.6 Billion by 2030 as Digital Tailoring Transforms Industry

Table of Contents

The global Custom & Group Apparel industry serves consumers worldwide with diverse solutions.

1. Industry Overview

The global custom clothing market hit USD 10 billion in 2023—and it's accelerating faster than most industry observers predicted. With a compound annual growth rate of 8% projected through 2030, the sector is reshaping how businesses and consumers think about apparel procurement. This isn't your grandfather's tailor shop; it's a technologically sophisticated industry leveraging digital measurement, AI-driven design, and flexible manufacturing to deliver bespoke products at unprecedented scale. The shift from mass production to personalized garments represents one of the most significant transformations in the textile and apparel sector this decade, driven by changing workplace dynamics, rising consumer expectations for individual expression, and corporate demand for differentiated team identities.

Industry Scope & Characteristics

Broad Product Portfolio

Products span custom suits, tailored shirts, group uniforms, corporate apparel, team jerseys, school uniforms, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

North America leads the world in custom apparel spending, with the market valued at USD 20,086.08 million in 2024—representing roughly 20% of global custom clothing revenue. The region's compound annual growth rate of 8.0% from 2024 to 2031 outpaces many mature markets, fueled by corporate uniform programs, sports team apparel contracts, and a growing appetite for personalized workwear. Meanwhile, the broader global apparel market—which custom clothing feeds into as a premium segment—reached USD 1,749.67 billion in 2025 and is projected to climb to USD 1,804.08 billion in 2026. Custom and group apparel sits at the intersection of mass market scale and bespoke precision, creating opportunities for manufacturers who can deliver flexibility without sacrificing quality.

The competitive landscape has shifted dramatically as traditional tailoring operations merge with tech-enabled production platforms. Major players including Ravis, Judger, Hanpimei, Heilan Home, Tongguk, and Inman have invested heavily in digital measurement capabilities and streamlined supply chains to reduce minimum order quantities. What once required runs of hundreds of identical garments now starts at quantities as low as single units for certain product categories. This MOQ flexibility has opened custom apparel to small businesses, startups, and independent sports teams—segments previously priced out of the bespoke market.

Supply chain resilience has become a defining battleground. Post-2020 disruptions exposed vulnerabilities in offshore manufacturing, prompting both buyers and suppliers to reconsider sourcing strategies. Near-shoring trends in North America and Europe benefit regional producers capable of faster turnaround times, while Asia-based manufacturers like those in China's established textile hubs maintain cost advantages for larger volume orders. The industry now operates across a fragmented but increasingly connected global network where speed, quality, and customization coexist as competitive imperatives.

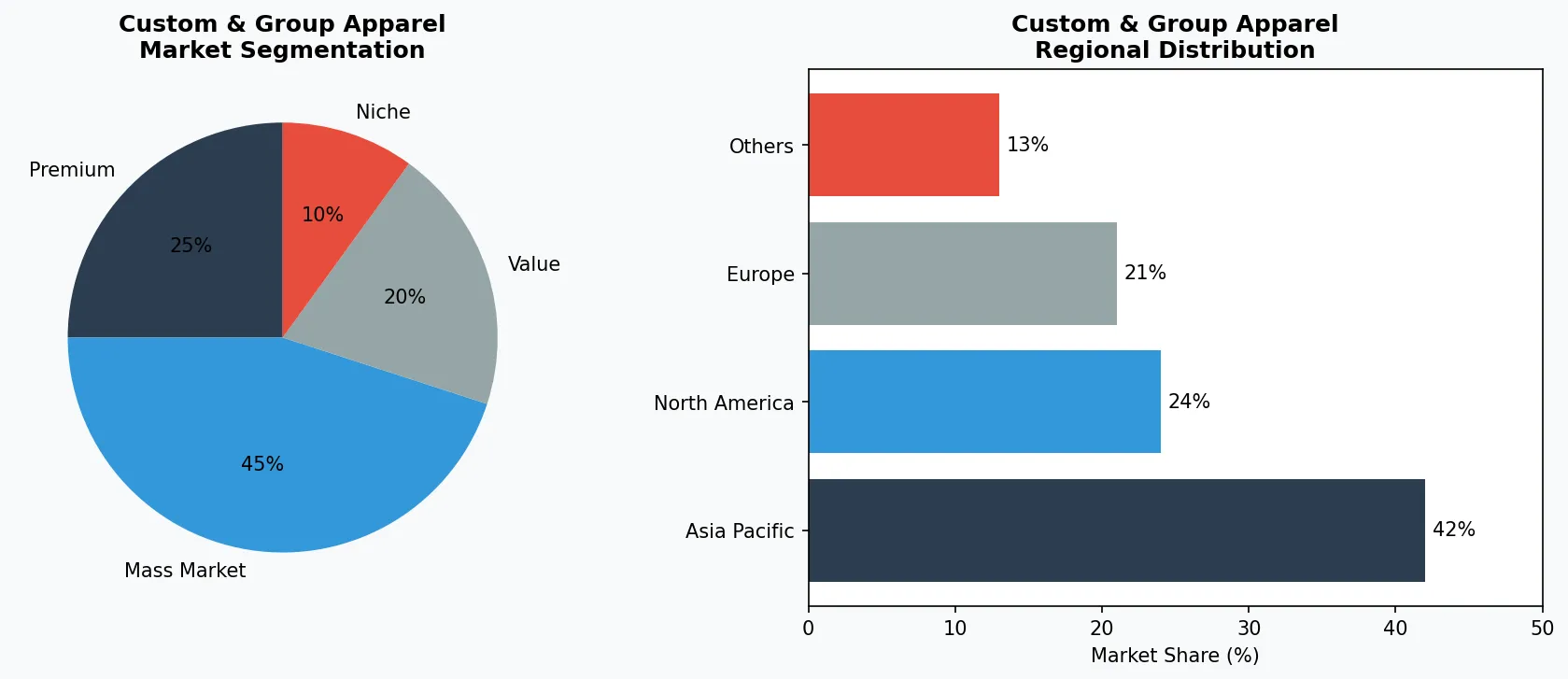

Key market segments and growth drivers in the Custom & Group Apparel sector.

2. Market Analysis

The global custom clothing market reached USD 10 billion in 2023 and is on track to grow at an 8% CAGR through 2030, according to industry analysis. By 2030, the market will approach USD 16 billion—a trajectory that reflects fundamental shifts in how organizations and individuals procure workwear, team apparel, and personalized garments. This growth outpaces the broader apparel market, which expanded from USD 1,749.67 billion in 2025 to an estimated USD 1,804.08 billion in 2026, signaling that customization commands a premium that drives faster-than-average expansion.

Three primary drivers fuel this momentum. First, corporate demand for distinctive workwear has intensified as companies use employee apparel as a branding and culture-building tool. Group uniforms now extend beyond traditional industries like hospitality and healthcare into technology firms, creative agencies, and professional services—markets that previously accepted off-the-rack solutions. Second, the explosion of team sports participation and recreational athletics has created sustained demand for custom jerseys, club wear, and performance gear at both youth and adult levels. Third, MOQ flexibility enabled by advances in digital printing and automated cutting has democratized custom apparel, making small-batch orders economically viable for the first time.

Digital integration separates high-growth players from laggards. Companies that have invested in online configuration tools, virtual fitting capabilities, and automated order processing capture higher margins and shorter sales cycles. The 2026 apparel marketing landscape shows retail media, paid search optimization, and AI-driven discovery becoming critical acquisition channels—meaning suppliers must develop digital presence alongside manufacturing excellence to remain competitive.

Geographic dynamics reveal distinct growth patterns. North America commands the highest per-capita spending on custom clothing, with its USD 20,086.08 million market reflecting strong corporate uniform programs and sports team culture. Europe shows robust growth in bespoke tailoring, particularly for executive apparel and luxury corporate wear. Asia-Pacific represents the fastest-expanding region, driven by rising middle-class consumption, corporate formalization in emerging markets, and growing interest in personalized fashion among younger demographics.

Market segmentation and regional distribution analysis for Custom & Group Apparel.

3. Product Categories

Corporate and executive apparel forms the largest product category, encompassing custom suits, tailored dress shirts, blazers, and business casual separates designed for professional environments. This segment targetslaw firms, financial institutions, and consulting companies seeking cohesive team presentations. Manufacturers like Ravis and Judger dominate this space, offering fabric selection tools, monogramming capabilities, and volume discount structures that appeal to enterprise buyers managing hundreds or thousands of employee uniforms.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Team uniforms and group wear represent a high-volume category spanning sports teams, school athletics, corporate recreational leagues, and community organizations. Custom jerseys, track suits, warm-up kits, and fan apparel fall into this classification. The category benefits from recurring purchase cycles—sports teams reorder annually or seasonally—and strong brand identity requirements that necessitate customization. Heilan Home has established significant capacity in this segment, leveraging economies of scale to serve national and regional sports organizations alongside corporate clients.

School uniforms and institutional apparel constitute a stable, demand-predictable category favored by educational institutions, religious organizations, and healthcare systems. These products prioritize durability, cost efficiency, and consistent sizing over fashion differentiation. Manufacturers competing here must balance embroidered logos and school-specific color requirements against tight budgets and high-volume orders. Tongguk has cultivated expertise in this category, offering competitive pricing on cotton-blend uniforms with reinforced construction for extended wear cycles.

Specialized and promotional apparel rounds out the product portfolio, including event-specific merchandise, trade show giveaways, and performance athletic wear with technical fabrics. This category often involves one-off or limited-run orders where speed-to-delivery matters more than unit cost. Inman has positioned itself to capture this fragmented market through rapid-turnaround printing and embroidery services that fulfill short-lead-time corporate and community event needs.

4. Leading Players

Ravis has emerged as a technology-forward leader in the custom apparel space, investing heavily in digital measurement platforms and AI-assisted design tools that streamline the customer configuration experience. The company's strategy centers on capturing the small-to-medium enterprise market for corporate uniforms—businesses that need professional appearance standards without the procurement complexity of traditional uniform suppliers. Ravis's online ordering portal allows buyers to specify custom dimensions, upload logos, and review virtual fit previews before production, reducing return rates and improving customer satisfaction metrics that drive repeat business.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the custom & group apparel space.

Judger competes at the large-volume end of the corporate uniform market, serving major corporations and government agencies with orders numbering in the thousands. The company's competitive advantage lies in manufacturing efficiency and supply chain integration—relationships with fabric mills and component suppliers enable cost structures that smaller players cannot match. Judger's recent investments in automated cutting and robotic embroidery systems have reduced labor costs while improving consistency across high-volume runs, positioning the company to win contracts where price competitiveness determines award decisions.

Hanpimei occupies the premium bespoke segment, targeting executive clients and luxury hospitality brands willing to pay higher margins for superior craftsmanship. The company's approach emphasizes hand-finishing techniques, premium fabric sourcing, and personalized service that technology cannot fully replicate. Hanpimei's production facilities combine traditional tailoring methods with modern quality control systems, delivering custom suits and formal wear that meet the exacting standards of international business travelers and high-net-worth clientele. This positioning shields Hanpimei from price competition while building brand equity among corporate procurement decision-makers.

Heilan Home represents the scale player, leveraging vertical integration from fabric production through finished garment assembly to dominate large corporate uniform and institutional apparel contracts. The company's geographic footprint across China's manufacturing heartlands provides access to diverse textile capabilities and workforce expertise that supports rapid scaling for major orders. Recent strategic moves have focused on expanding international distribution and establishing regional service centers closer to North American and European corporate clients, reducing lead times that historically disadvantaged Asian suppliers against regional competitors.

5. Market Trends

1. PERSONALIZED TAILORING AI

PERSONALIZED TAILORING AI — AI-powered body scanning and fit prediction systems now enable retailers and suppliers to capture precise measurements through smartphone cameras or specialized kiosks, eliminating the need for in-person fittings while improving accuracy. This technology matters because fit-related returns account for 20-30% of online apparel purchases in traditional markets; custom apparel suppliers who eliminate this friction gain significant competitive advantage. Companies like Ravis have integrated AI measurement tools into their ordering platforms, reducing order-to-delivery cycles while improving first-time fit rates.

2. MOQ FLEXIBILITY REVOLUTION

MOQ FLEXIBILITY REVOLUTION — Minimum order quantity barriers that once excluded small organizations from custom apparel have collapsed thanks to digital printing and single-unit embroidery capabilities. What previously required runs of 50-100 units now starts at quantities as low as single items for certain product categories. This trend matters because it expands the addressable market from large enterprises to the 30 million small businesses in North America alone—organizations seeking differentiation through customized workwear without committing to bulk orders. Manufacturers like Inman have built entire business models around serving these previously underserved micro-enterprise customers.

3. SUSTAINABLE CUSTOM PRODUCTION

SUSTAINABLE CUSTOM PRODUCTION — Environmentally conscious manufacturing practices are becoming prerequisites for winning corporate contracts, with major buyers increasingly requiring recycled materials, water-efficient dyeing processes, and transparent supply chains. This trend matters because sustainability compliance now influences procurement decisions alongside price and quality. Leading players including Heilan Home have invested in eco-certified production lines that use organic cotton, recycled polyester, and closed-loop water systems, positioning themselves to capture demand from corporations with ambitious ESG commitments.

4. QUICK TURNAROUND MANUFACTURING

QUICK TURNAROUND MANUFACTURING — Compressed production timelines—from traditional 4-6 week lead times down to 7-10 days for standard custom orders—have become a competitive differentiator as organizations demand agility. This matters because late uniform deliveries create operational disruptions for businesses that schedule training sessions, product launches, or team-building events around apparel availability. Manufacturers responding to this demand have redesigned workflows, invested in rapid prototyping equipment, and established regional finishing facilities that complete customization closer to end customers.

6. Regional Markets

North America remains the world's largest and most sophisticated custom apparel market, with 2024 valuations reaching USD 20,086.08 million. The region's dominance reflects mature corporate uniform programs across diverse industries, strong sports team culture driving youth and adult apparel demand, and high per-capita spending on personalized fashion. The United States specifically shows concentrated demand in metropolitan business corridors—New York financial services, Los Angeles entertainment industry, and Chicago professional services—where employer-branded workwear has become standard practice. Canadian demand centers on resource extraction and manufacturing sectors requiring specialized industrial apparel alongside traditional corporate uniforms.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

Europe presents a bifurcated landscape where Western markets prioritize premium bespoke tailoring while Eastern European nations embrace custom apparel as an emerging consumption category. Germany, the United Kingdom, and France drive demand for executive workwear and corporate formal attire, with particular strength in luxury hospitality and financial services sectors. The region's emphasis on craftsmanship and quality construction means custom apparel commands higher price points than comparable North American offerings, supporting healthy margins for manufacturers capable of meeting European quality standards. Sustainability regulations in the EU—including expanded producer responsibility requirements—also influence sourcing decisions, favoring suppliers with demonstrable environmental credentials.

Asia-Pacific represents the fastest-expanding regional market, driven by corporate formalization across China, India, and Southeast Asian economies. China's established textile manufacturing infrastructure positions the country as both a major producer and growing consumer of custom apparel, with domestic demand rising among the expanding middle class seeking personalized fashion. India shows particular strength in school uniform and institutional apparel markets, while Southeast Asian nations offer growth potential as manufacturing shifts from China to lower-cost alternatives. Competition in this region intensifies as local manufacturers develop capabilities that previously required Western technology, compressing margins while expanding market access for buyers at every price point.

7. Investment Outlook

Two concrete opportunities define the sector's trajectory through 2027. First, AI-driven fit prediction and virtual try-on technologies will mature sufficiently for mainstream deployment, enabling suppliers to offer near-instant custom garment production with measurement accuracy matching professional tailors. Companies that integrate these capabilities into seamless buying experiences will capture market share from both traditional custom apparel providers and mass-market retailers attempting customization. Second, corporate ESG requirements will create sustained demand for sustainably sourced custom apparel, allowing suppliers with certified eco-friendly production to command premium pricing while competitors scramble to retrofit facilities. The regulatory environment increasingly favors producers who invested early in sustainable manufacturing infrastructure.

One concrete risk demands attention: raw material cost volatility threatens margin stability across the custom apparel sector. Cotton prices fluctuate based on weather patterns and agricultural policy, while synthetic fabric costs track petroleum market movements. For custom apparel suppliers operating on thin margins in competitive bidding environments, inability to pass through input cost increases creates profitability pressure that could accelerate consolidation. Companies lacking diversified supplier relationships or hedging strategies face particular vulnerability to supply shocks—a risk amplified by ongoing geopolitical tensions affecting global textile trade flows. Strategic positioning requires balancing cost competitiveness against supply chain resilience, a tension that will define competitive outcomes through the decade's second half.

Strategic Considerations:

- ('Technology & AI Integration:', 'Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.')

- ('Sustainability as Business Strategy:', 'Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.')

- ('Transparency & Traceability:', 'Consumers demand increasingly granular information about product origins, ingredients, and production methods.')

- ('Emerging Market Penetration:', 'Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.')

Make Informed Decisions in the Custom & Group Apparel Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-14. All market figures are estimates and may vary from actual results.