-450x250h.webp)

-150x150h.webp)

Butter's $63 Billion Rebound: Why 2026 Is the Year of Cultured and Grass-Fed Varieties

Table of Contents

The global Butter Types & Usage sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Butter is no longer the simple yellow block your grandmother used. In 2025, the global butter market hit $43.83 billion, but the real story is the dramatic shift in what 'butter' means to buyers. Cultured and European-style varieties have captured 25% more retail shelf space over the past two years, signaling a premiumization wave that is reshaping the dairy aisle. This isn't a fleeting trend—it's a structural change driven by consumers who now demand provenance, flavor complexity, and functional benefits from a product once seen as a commodity. For B2B buyers in the Dairy & Egg Products sector, understanding the nuances of butter types is no longer optional; it is a competitive necessity. Whether you are sourcing for a bakery chain, a foodservice operator, or a private-label brand, the choice between salted, unsalted, sweet cream, cultured, or clarified butter directly impacts cost, shelf life, and end-product quality. The rise of grass-fed and A2 butter further complicates the landscape, as does the parallel growth of plant-based alternatives that mimic butter's functionality. This article dissects the key butter types, market forces, and strategic moves that every industry professional should track in 2026.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Butter Types & Usage, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

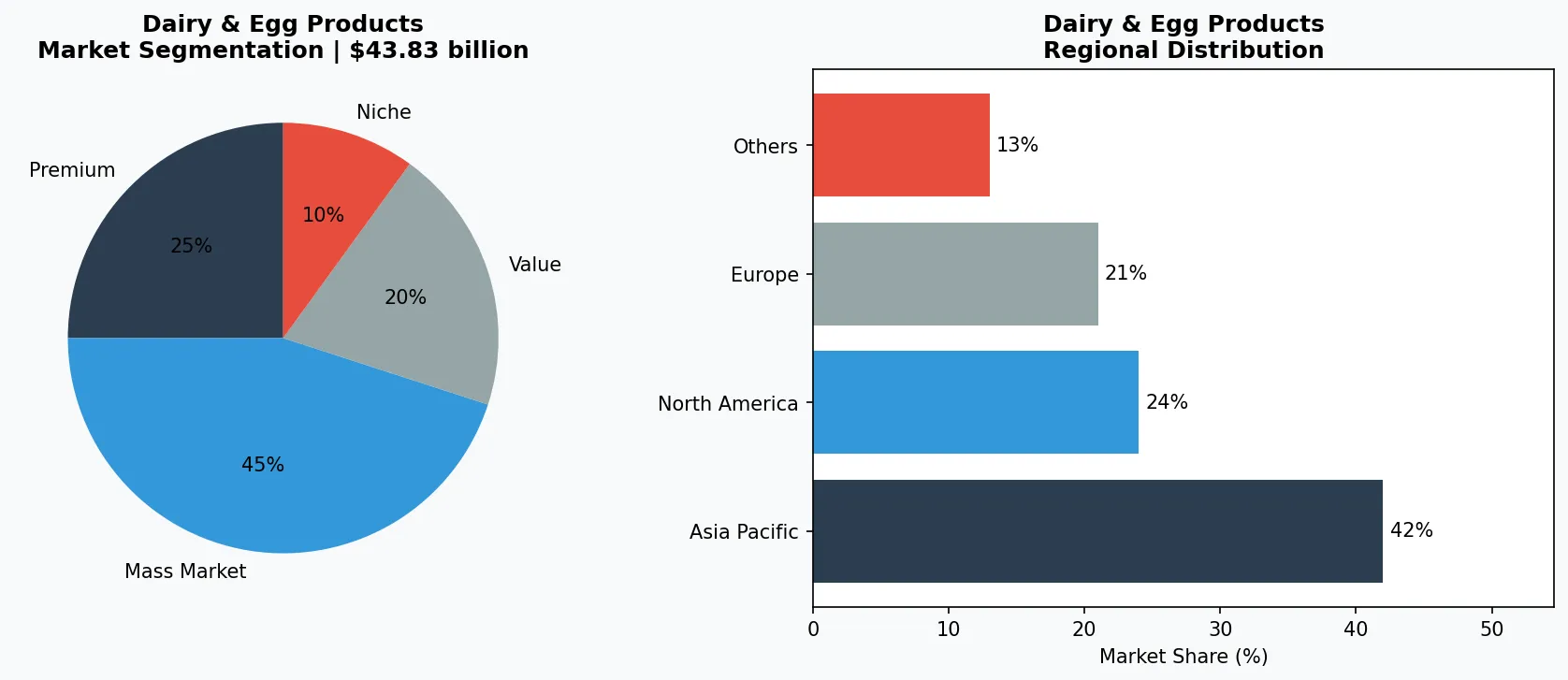

Key market segments and growth drivers in the Butter Types & Usage sector.

2. Market Analysis

The global butter market was valued at $43.83 billion in 2025 and is projected to reach $45.18 billion in 2026, growing to $63.49 billion by 2034 at a compound annual growth rate (CAGR) of 4.34%, according to industry analyses. This steady expansion is underpinned by three major drivers. First, the clean-label movement is fueling demand for butter made from simple, natural ingredients, reversing decades of margarine dominance. Consumers are scrutinizing ingredient lists and willing to pay a premium for butter that lists only cream and salt. Second, health perceptions around dairy fats have shifted; recent nutritional studies have rehabilitated saturated fats from butter, especially from grass-fed cows rich in conjugated linoleic acid (CLA). This has boosted sales of grass-fed and cultured butter, which command price premiums of 30–50% over standard varieties. Third, premiumization is not just a consumer story—it is a supply-chain reality. Retailers in North America and Europe have expanded dedicated 'premium butter' sections, with cultured and European-style butter varieties gaining 25% more shelf space in 2024 alone. This space is being filled by imported as well as domestic artisan producers, creating new sourcing opportunities for distributors and food manufacturers. The Asia-Pacific region, particularly China and India, is emerging as a high-growth market for butter used in bakery and confectionery, further propelling global demand.

Market segmentation and regional distribution analysis for Butter Types & Usage.

3. Product Categories

Butter types can be grouped into four primary categories, each serving distinct use cases. **Salted and Unsalted Butter** remain workhorses. Unsalted (or sweet cream) butter is the baker's standard because it allows precise control over sodium content. Salted butter, typically containing 1–2% salt, is preferred for table use and spreads. For professional kitchens, European-style butter—with a fat content of 82–86% versus the standard 80%—offers richer flavor and less water, making it ideal for laminated doughs like croissants and puff pastry. Brands such as Plugrà and Kerrygold have popularized this style globally. **Cultured Butter** is made by fermenting cream with lactic acid bacteria before churning, yielding a tangy, complex flavor profile. It is increasingly used in high-end pastry and as a finishing butter. **Grass-Fed Butter** comes from cows that graze pasture, resulting in a deeper yellow color and higher levels of beta-carotene and CLA. It is marketed as a health-conscious and environmentally friendlier option. **Clarified Butter (Ghee)** , which has had milk solids removed, boasts a high smoke point (around 485°F) and is shelf-stable without refrigeration, making it a staple in Indian cuisine and for high-heat cooking. Each type requires different sourcing specifications, storage conditions, and price points, which B2B buyers must evaluate when selecting suppliers.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The butter market is shaped by a mix of global dairy cooperatives, regional processors, and niche artisan producers. **Large-scale dairy cooperatives** such as those in the European Union (e.g., Ireland, France, Netherlands) dominate the production of European-style and cultured butter, leveraging centuries-old techniques and economies of scale. These players export heavily to North America and Asia, capitalizing on the premiumization trend. **North American dairy processors** have responded by launching their own cultured and grass-fed lines, often under private-label arrangements for major retailers. **Artisan creameries**, while small in volume, are driving innovation in flavor profiles—smoked, herb-infused, single-herd butters—that attract premium pricing and media attention. For B2B buyers, the strategic challenge is balancing cost and quality: while global cooperatives offer stable supply and compliance with food safety standards, smaller producers can provide unique product differentiation and tighter traceability. **Private-label manufacturers** have also entered the premium butter space, using supplier partnerships to offer store-brand cultured butter at a 20–30% discount to national brands, capturing value-conscious yet trend-driven shoppers. The competitive landscape in 2026 will favor suppliers that can demonstrate both scale and specialty, particularly those with certifications such as grass-fed, organic, or Non-GMO Project Verified.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the dairy & egg products space.

5. Market Trends

1. TREND_1

TREND_1 — Plant-Based Butter Alternatives | What it is: Non-dairy spreads made from oils (coconut, shea, avocado) and starches designed to mimic butter's flavor and functionality. Why it matters: Clean-label, vegan, and lactose-free trends are driving retail growth of plant-based butter at 8–10% annually, encroaching on traditional butter shelf space. Example: Several European dairy companies have launched hybrid or plant-based lines to protect market share, while dedicated plant-based brands expand distribution into foodservice. TREND_2 | Cultured & Grass-Fed Premiumization | What it is: Consumers trading up to butter varieties with a flavor story and health halo. Why it matters: Cultured butter now accounts for over 15% of specialty butter sales in the US and Europe, with grass-fed growing even faster. Example: Retailers like Whole Foods and Waitrose have doubled their grass-fed butter SKUs since 2023, and major dairy cooperatives now offer dedicated grass-fed supply chains. TREND_3 | Regenerative Agriculture Sourcing | What it is: Butter marketed as coming from farms using soil-health practices like rotational grazing and cover cropping. Why it matters: Brands use carbon-neutral certifications and regenerative labels to command premiums of 40%+ and meet corporate sustainability goals. Example: Several European butter brands now carry Regenerative Organic Certified (ROC) seals, and US dairy processors are piloting traceability programs that link butter packs to specific regenerative farms.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two opportunities stand out for B2B buyers in the butter space. First, sourcing direct from grass-fed and regenerative farms can secure both a premium price point and a powerful sustainability narrative for downstream customers—particularly in the foodservice and bakery sectors where margins allow for upselling. Second, investing in cultured butter production or co-packing arrangements can differentiate a supplier's portfolio as retail shelves continue to expand for this segment. One concrete risk: the volatility of global cream and milk fat prices, which have swung 20–30% year-over-year due to feed costs, weather events, and dairy herd reductions. Buyers should lock in forward contracts or diversify across geographies (e.g., combining European and New Zealand supply) to mitigate price spikes. In 2026, the butter winners will be those who treat butter not as a commodity, but as a differentiated ingredient with a story—and the data to back it up.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Butter Types & Usage Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-26. All market figures are estimates and may vary from actual results.