-450x250h.webp)

-150x150h.webp)

The $55 Billion Sweet Tooth: How the Confectionery Candy Market Defies Economic Gravity in 2026

Table of Contents

The global Confectionery Candy Market sector serves consumers worldwide with diverse solutions.

1. Industry Overview

What industry can boast a 99.8% household penetration rate? The answer is the confectionery candy market, a resilient and ubiquitous segment within the broader Bakery Ingredients & Ready-to-Eat Snacks industry. Distinct from its savory snack counterparts, this market is defined by its powerful emotional resonance, acting as a vehicle for celebration, comfort, and tradition. Its performance is less about daily sustenance and more about occasion-driven indulgence and gifting, creating a unique demand curve that peaks dramatically around cultural and seasonal events. This emotional connection translates into staggering commercial scale: the category generated $55 billion in U.S. retail sales last year alone, demonstrating its foundational role in American consumer spending. The segment's distinctiveness lies in its ability to command premium pricing for experiential pleasure, from single-origin chocolate bars to artisanal hard candies, setting it apart from more commoditized snack aisles.

Industry Scope & Characteristics

Broad Product Portfolio

Products span cane sugar, brown sugar, rock sugar, powdered sugar, stevia, erythritol, coconut sugar, honey, maple syrup, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Industry application and market overview for Confectionery Candy Market.

2. Market Analysis

The global confectionery market is on a clear growth trajectory, projected to reach approximately $325.5 billion in 2025 and continue expanding at a steady compound annual growth rate (CAGR) of 3.9% through 2032. In North America, growth is even more robust, with an anticipated CAGR of 5.5% from 2026 to 2033. This expansion is fueled by several concrete drivers. First is powerful seasonal demand, particularly around holidays like Halloween, Christmas, and Easter, which can account for a disproportionate share of annual sales. Second is consistent innovation, with global new product launches growing by 7% between October 2020 and September 2025, as brands compete for consumer attention with novel flavors, formats, and functional benefits. Underpinning this growth is the market's remarkable penetration; with 99.8% of households purchasing confectionery at least once in 2025, it enjoys a nearly universal consumer base, providing a stable foundation for both mass-market and niche premium strategies.

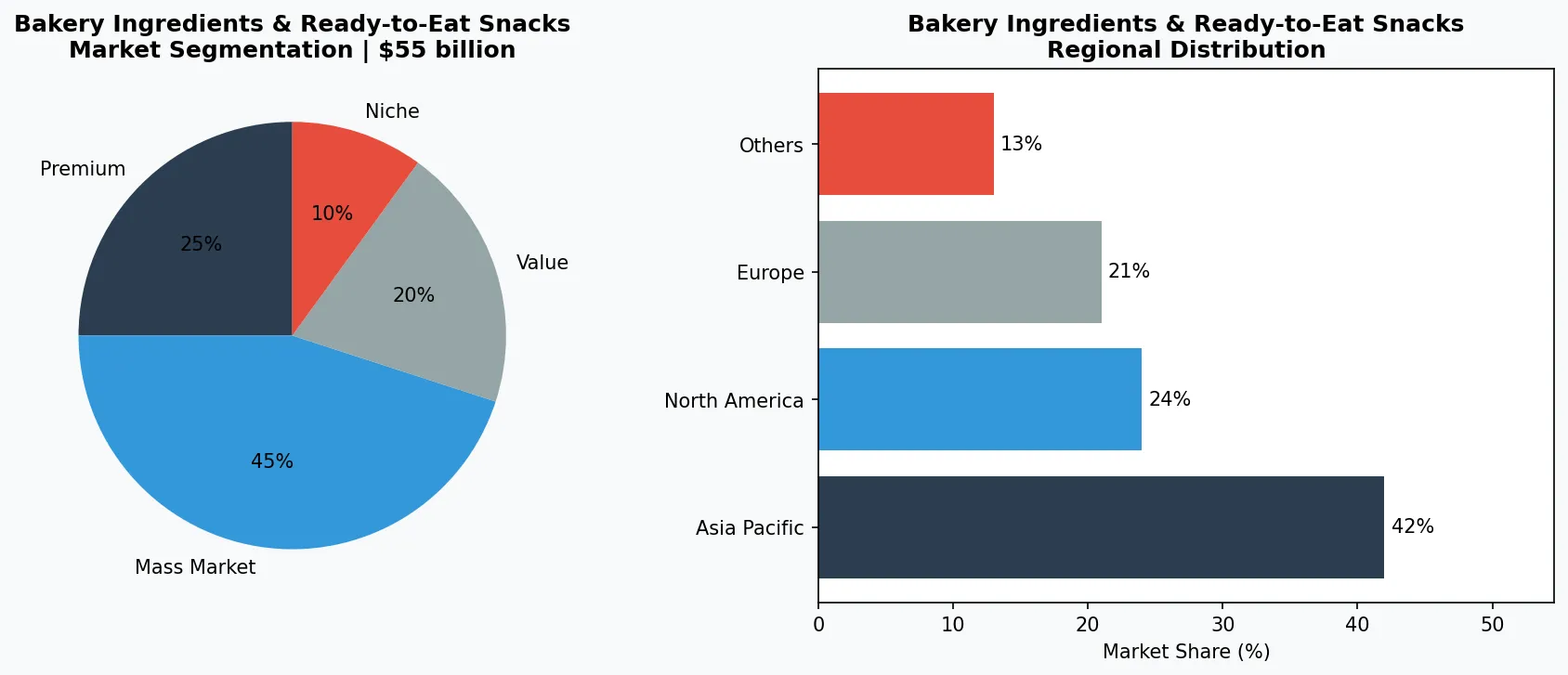

Market segmentation and regional distribution for Bakery Ingredients & Ready-to-Eat Snacks - Confectionery Candy Market.

3. Product Categories

The confectionery candy market is broadly organized into several key product types. Chocolate confectionery, led by America's favorite milk chocolate, dominates in value and includes countlines, boxed chocolates, and seasonal novelties from giants like Hershey and Mars. Sugar confectionery encompasses a vast array of non-chocolate sweets, from classic hard candies and chewy caramels to modern gummies and sour belts, with brands like Haribo and Jelly Belly leading in innovation. Gum and mints represent a segment focused on oral freshness and functional benefits, though it has faced challenges in recent years. Finally, the power seasonal and novelty segment includes products explicitly designed for holidays (e.g., Halloween candy bags, Christmas candy canes) and licensed character-themed sweets, which drive significant impulse purchases and limited-time excitement.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The Hershey Company remains the undisputed leader in the North American market, leveraging its deep brand heritage in chocolate and an aggressive acquisition strategy (like Dot's Homestyle Pretzels and SkinnyPop) to expand its snack portfolio beyond pure confectionery. Its strategy hinges on dominating seasonal aisles and securing prime retail real estate. Mars Wrigley, a close competitor, operates with a dual strength in both chocolate (M&M's, Snickers) and gum (Orbit, Extra), though it is actively pivoting its gum portfolio towards functional benefits and premiumization to counter segment softness. Mondelez International takes a global, premium-centric approach, focusing on high-margin chocolate brands like Cadbury and Milka while investing heavily in sustainability marketing to appeal to ethically conscious consumers. Ferrero Group has grown through strategic acquisitions (Nestlé's U.S. candy business, Kellogg's cookies) to solidify its position as a third major chocolate force, emphasizing quality ingredients and family-owned heritage.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the bakery ingredients & ready-to-eat snacks space.

5. Market Trends

1. Sugar Reduction & Recipe Transformation

Sugar Reduction & Recipe Transformation — Brands are reformulating to reduce sugar via natural sweeteners and fiber blends to meet health demands and regulatory pressures, exemplified by Mondelez's 'Well-being' portfolio which includes reduced-sugar options.

2. Plant-Based & Ethical Sourcing

Plant-Based & Ethical Sourcing — The rise of vegan, dairy-free chocolates and a sharp focus on certified sustainable cocoa addresses growing consumer ethics, with brands like Tony's Chocolonely building their entire identity on transparent, slave-free supply chains.

3. AI & Hyper-Personalization

AI & Hyper-Personalization — Artificial intelligence is being used for demand forecasting, optimizing seasonal production, and even creating personalized flavor profiles, allowing companies to minimize waste and maximize consumer engagement through data.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities stand out. First, the premiumization wave offers significant margin growth for brands that can successfully market high-cocoa, single-origin, or experientially packaged products. Second, the integration of functional ingredients—like adaptogens for stress relief or probiotics for gut health—presents a path to reposition candy from 'empty calories' to permissible, beneficial indulgence, tapping into the broader wellness trend. The most concrete risk is intensifying regulatory scrutiny and potential taxation on sugar content, which could compress margins, force costly reformulations, and dampen impulse purchase volume. Navigating this will require a balanced portfolio that innovates ahead of legislation.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Confectionery Candy Market Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-23. All market figures are estimates and may vary from actual results.