-450x250h.webp)

-150x150h.webp)

Food Antioxidants Market to Hit $1.12 Billion by 2033: Clean Label Trends and Synthetic Stability Drive Growth

Table of Contents

The global Antioxidants in Food Industry sector serves consumers worldwide with diverse solutions.

1. Industry Overview

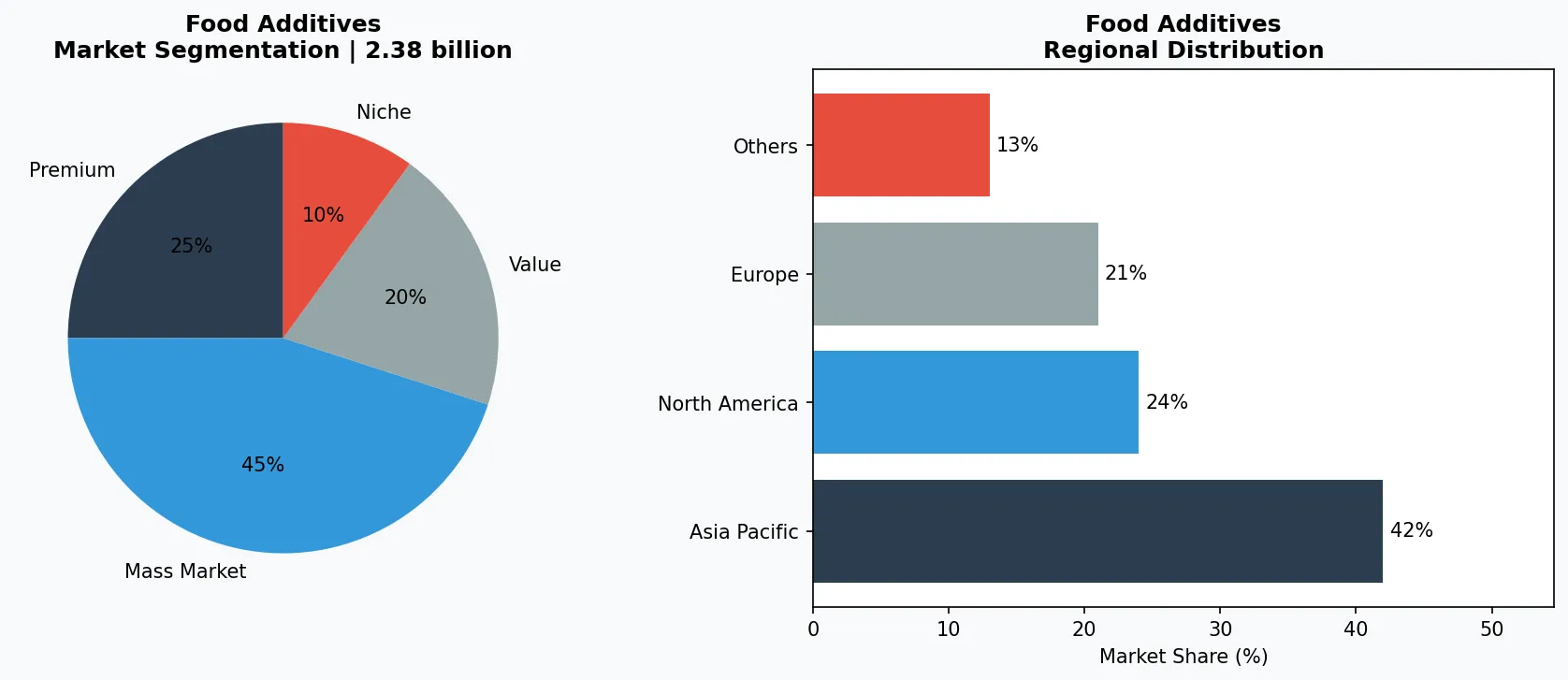

By 2025, the global food antioxidants market will already command $2.38 billion in value. Yet the trajectory that matters most is the 13.9% compound annual growth rate projected for North America from 2026 to 2033—nearly double the global CAGR of 6.5%. That divergence signals a fundamental restructuring of how the industry approaches shelf-life extension and ingredient safety. Food antioxidants are chemical or natural compounds that inhibit oxidation, preventing rancidity, color degradation, and nutrient loss in fats, oils, meats, bakery goods, and pet food. They occupy a distinctive niche within the broader food additives segment because they act as both preservatives and quality enhancers, directly impacting consumer perception of freshness. The market’s urgency stems from rising demand for minimally processed foods, where antioxidants must compensate for reduced synthetic preservatives. Over 60% of processed foods now rely on some form of antioxidant, with the meat and poultry segment alone accounting for nearly 30% of total consumption. As regulatory pressure tightens and clean-label movements accelerate, the battle between synthetic stability and natural sourcing defines the industry’s next decade.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Antioxidants in Food Industry, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Key market segments and growth drivers in the Antioxidants in Food Industry sector.

2. Market Analysis

The food antioxidants market is growing rapidly, with multiple data points converging on a clear trajectory. According to recent industry analyses, the market was valued at $2.14 billion in 2025 and is expected to reach $2.39 billion in 2026—a compound annual growth rate of 11.7% year-over-year. Longer-term projections show the market crossing $1.12 billion by 2033, up from $721.3 million in 2026, implying a sustained CAGR of 6.5%. However, regional disparities are pronounced. North America, driven by stringent FDA regulations and consumer demand for clean labels, is forecast to grow at a staggering 13.9% CAGR from 2026 through 2033. Europe follows with a steadier 5.8% CAGR, while Asia Pacific—led by China and India—is accelerating at 7.2% as processed food penetration deepens. Three growth factors dominate: first, the expansion of the meat and poultry industry, which uses antioxidants to prevent lipid oxidation and maintain color; second, the rise of functional and fortified foods requiring shelf-stable formulations; and third, the substitution of synthetic antioxidants like BHA and BHT with natural alternatives such as rosemary extract and tocopherols. The dry form segment holds a 65% share due to its ease of handling and longer shelf life, but liquid antioxidants are gaining ground in emulsion-based applications like salad dressings and sauces.

Market segmentation and regional distribution analysis for Antioxidants in Food Industry.

3. Product Categories

The market segments primarily by type, form, and application. By type, synthetic antioxidants—including butylated hydroxyanisole (BHA), butylated hydroxytoluene (BHT), propyl gallate, and tert-butylhydroquinone (TBHQ)—still dominate with roughly 55% market share. Their cost-efficiency and superior thermal stability make them indispensable in high-temperature frying oils and baked goods. However, the natural antioxidant category is the fastest-growing, expanding at nearly 9% CAGR. Key examples include tocopherols (vitamin E) from vegetable oils, ascorbic acid (vitamin C), rosemary extract rich in carnosic acid, and green tea polyphenols. By form, the dry segment (powders and granules) leads at 60% of revenue because of simpler logistics and compatibility with dry mixes, seasonings, and meat rubs. Liquid antioxidants are preferred for liquid fat systems, marinades, and emulsions. By application, meat and poultry represent the largest end-use, consuming about 35% of all food antioxidants, followed by bakery and confectionery at 25%, fats and oils at 20%, and fish and seafood at 10%. The pet food segment, though smaller at 5%, is growing at over 8% annually as premiumization and humanization of pet diets demand higher-quality preservation.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The competitive landscape is concentrated among multinational chemical and ingredient companies. BASF, with its extensive portfolio of synthetic antioxidants like Irganox and natural alternatives under the Verdad brand, leverages vertical integration in raw material sourcing and R&D in encapsulation technologies to maintain a 15% market share. The company has invested heavily in plant-based tocopherol production to capture clean-label demand. Archer Daniels Midland (ADM) competes through its broad natural extracts division, supplying rosemary, green tea, and mixed tocopherols. ADM’s strategy hinges on partnerships with food processors to co-develop antioxidant blends tailored to specific oxidative stress profiles, particularly in meat and bakery sectors. Kemin Industries differentiates itself with proprietary formulations like FORTIUM and FenuFresh, which combine natural antioxidants with organic acids and essential oils for synergistic protection. Kemin’s focus on poultry and pet food has yielded double-digit growth in those segments. DuPont Nutrition & Biosciences (now part of International Flavors & Fragrances) emphasizes clean-label solutions through its Danisco range, including Grindsted antioxidants derived from rosemary and ascorbyl palmitate. DuPont’s technical service teams work directly with manufacturers to replace synthetic antioxidants without compromising shelf life, a capability that has won contracts with major snack and meat brands.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the food additives space.

5. Market Trends

1. CLEAN LABEL TRANSFORMATION

CLEAN LABEL TRANSFORMATION — Consumers increasingly demand recognizable ingredients, driving food manufacturers to replace synthetic antioxidants like BHA and BHT with natural alternatives. This shift has accelerated since 2022, with over 40% of new product launches in North America claiming 'no artificial preservatives.' Companies like Kemin have responded with enhanced rosemary extract formulations that match synthetic efficacy. | AI-DRIVEN FORMULATION OPTIMIZATION | Artificial intelligence is being deployed to predict oxidation kinetics and optimize antioxidant blends in real time. BASF has integrated machine learning models into its customer portal, allowing R&D teams to simulate shelf-life outcomes under different temperature and packaging conditions. This reduces trial costs by up to 30% and shortens product development cycles. | PLANT-BASED & PET FOOD EXPANSION | The surge in plant-based meat alternatives creates new oxidation challenges—higher unsaturated fat content makes these products more prone to rancidity. Simultaneously, the premium pet food segment is adopting food-grade antioxidants historically reserved for human consumption. ADM has launched a dedicated line of natural antioxidants for plant-based burgers and kibble, targeting a combined market opportunity exceeding $800 million by 2028. | REGULATORY HARMONIZATION IN ASIA | China and India are tightening permissible levels of synthetic antioxidants, pushing local processors toward natural solutions. The Asia Pacific market is now the fastest-growing region for natural antioxidants at 9.5% CAGR, with companies establishing sourcing networks for local herbs and spices.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities stand out. First, the pet food segment, currently underpenetrated but growing at over 8% annually, offers a high-margin avenue for natural antioxidant suppliers willing to navigate pet-specific safety regulations. Second, the integration of antioxidants into active packaging—through coatings or sachets—could create a new revenue stream worth an estimated $300 million by 2030, with early movers like Kemin already piloting smart labels. The primary risk is regulatory fragmentation: diverging standards for synthetic antioxidants between the EU (where BHA is restricted), the US (where it remains generally recognized as safe), and Asia (where limits are tightening) complicate global product formulations. Companies that invest in flexible, region-specific antioxidant portfolios and transparent labeling will capture disproportionate share as the market accelerates toward $1.12 billion by 2033.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Antioxidants in Food Industry Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-29. All market figures are estimates and may vary from actual results.