-450x250h.webp)

-150x150h.webp)

Food Thickeners Market to Reach $26.71 Billion by 2031: Types, Trends, and Strategic Shifts

Table of Contents

The global Food Thickeners Types sector serves consumers worldwide with diverse solutions.

1. Industry Overview

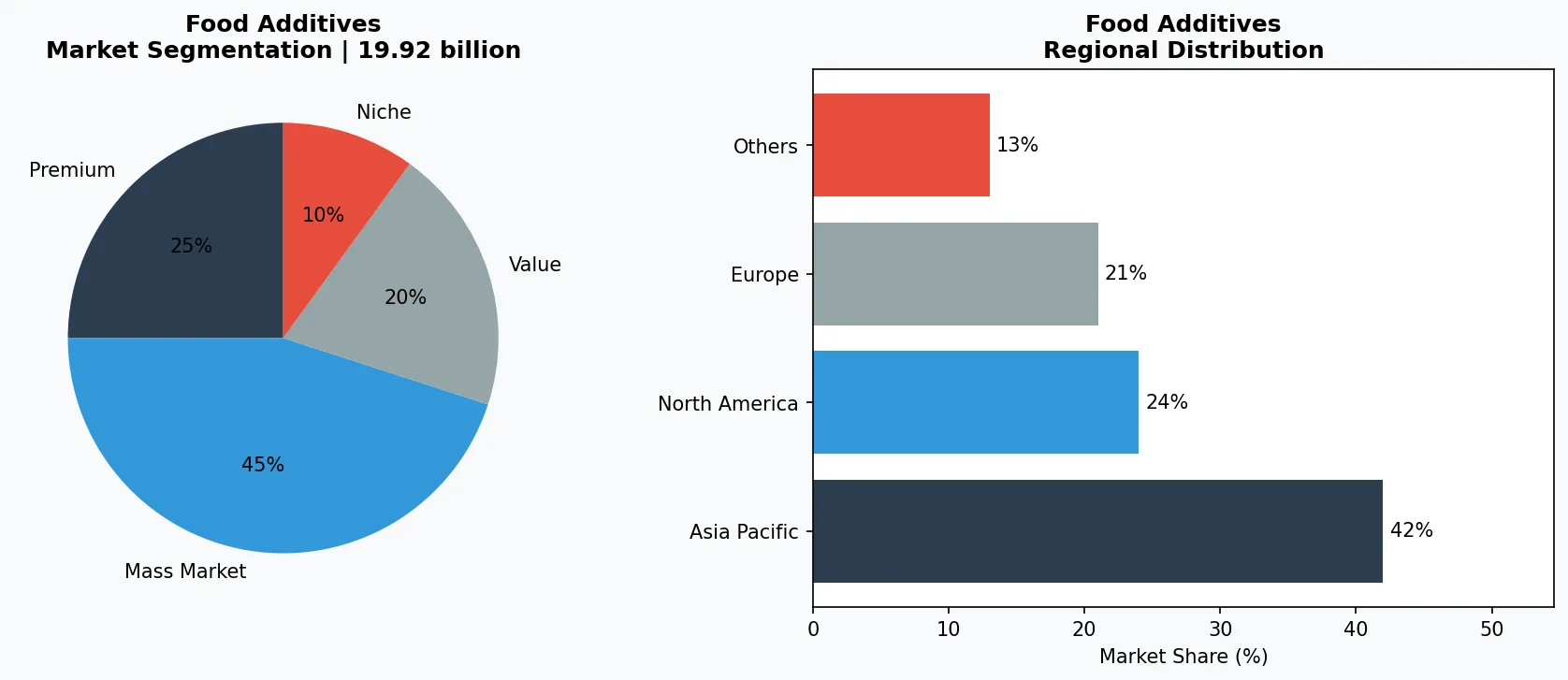

The global food thickeners market was valued at $19.92 billion in 2026 and is projected to surge to $26.71 billion by 2031, growing at a compound annual rate of 6.05%. That pace is accelerating—another forecast puts the thickening agent segment at a 7.8% CAGR through 2033. For any B2B buyer sourcing food additives, understanding which thickeners types dominate this expansion is no longer optional; it is a strategic imperative. Food thickeners are substances that increase viscosity without altering a product’s other properties. They are the unsung workhorses behind the smooth mouthfeel of sauces, the stable suspension in dressings, and the creamy texture of dairy alternatives. Their role is distinctive within the broader food additives industry because they directly affect both sensory experience and shelf stability—two critical factors in consumer acceptance and supply chain efficiency. Unlike preservatives or flavor enhancers, thickeners must balance functionality with label appeal. The shift toward plant-based and clean-label diets has forced manufacturers to replace synthetic options like modified starches with recognizable ingredients such as guar gum or pectin. This tension between performance and naturality defines the current market. As the data show, the demand for high-quality, natural thickeners is rising sharply, driven by consumers who read ingredient lists and reject chemical-sounding names. For suppliers, the winners will be those who can deliver viscosity without complexity.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Food Thickeners Types, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Key market segments and growth drivers in the Food Thickeners Types sector.

2. Market Analysis

The food thickener market is split into two competing growth narratives. The broader market, which includes starches, gums, pectins, and proteins, was worth $19.92 billion in 2026 and is expected to climb to $26.71 billion by 2031—a CAGR of 6.05%. However, the more narrowly defined thickening agent for food subsegment is growing even faster at 7.8% CAGR through 2033, according to separate research. This discrepancy suggests that while mature categories like corn starch hold volume, higher-value clean-label gums and exudates are driving value growth. Three factors are fueling this acceleration. First, the explosion of plant-based meat and dairy alternatives requires thickeners to replicate the texture of animal-based products—xanthan gum and carrageenan are now staples in oat milk and burger patties. Second, urbanization and convenience food consumption in Asia-Pacific are pushing demand for instant soups and ready-to-eat meals that rely on rapid hydration thickeners. Third, regulatory pressure on synthetic additives in the European Union and North America is forcing reformulation toward natural hydrocolloids. Geographically, Asia-Pacific leads in volume, but North America commands the highest per-ton revenue due to premium organic and non-GMO thickeners. The market is fragmented, with top players holding only 30–35% share, leaving room for specialized suppliers offering traceable, single-origin products. For Verity Rank users, targeting the right subsegment—such as xanthan gum for clean-label sauces or citrus pectin for fruit preparations—can mean the difference between margin growth and commodity pricing.

Market segmentation and regional distribution analysis for Food Thickeners Types.

3. Product Categories

Food thickeners fall into four primary categories: starches, gums, pectins, and proteins. **Starches** dominate volume globally, led by corn starch, tapioca starch, and modified food starch. Modified starches, while functional, face headwinds due to clean-label trends; unmodified waxy maize starch is gaining traction as a direct replacement. **Gums** include the hydrocolloids xanthan gum, guar gum, locust bean gum, and carrageenan. Xanthan gum is the most versatile—stable across pH and temperature—making it indispensable in gluten-free baking and salad dressings. Carrageenan, derived from red seaweed, is prized in dairy and plant-based milks for its creamy mouthfeel, though it faces scrutiny in some organic circles. **Pectins**, especially high-methoxyl (HM) and low-methoxyl (LM) varieties, are essential for jams, jellies, and fruit fillings. Citrus pectin offers a clean label and is increasingly used in yogurt and confectionery to reduce sugar while maintaining gel strength. **Proteins** such as gelatin and whey protein isolate act as thickeners in specific applications—gelatin in gummies and marshmallows, whey in protein shakes. However, the shift toward vegan alternatives is driving innovation in pea protein and soy protein thickeners. Each category has distinct thermal and pH stability profiles, and formulators often blend two or more to achieve specific textures. The key for buyers is matching the thickener’s functional properties to the processing conditions—high-shear mixing, acid environments, or frozen storage—while keeping the ingredient statement short and natural.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

Cargill has positioned itself as the leader in clean-label starches, investing heavily in non-GMO and organic tapioca starch lines. The company’s strategy focuses on vertical integration—controlling supply from cassava farms in Thailand to processing facilities—giving it both cost and traceability advantages. Cargill’s SimPure line of unmodified starches directly addresses the clean-label trend, allowing food manufacturers to replace modified starches without sacrificing performance. DuPont (now part of International Flavors & Fragrances, IFF) leverages its expansive hydrocolloid portfolio, including Danisco brand guar gum and pectin. IFF’s approach is ingredient system solutions: rather than selling single thickeners, it offers pre-blended stabilizer systems for yogurt, ice cream, and plant-based beverages. This reduces formulation risk for mid-size food companies and locks in recurring revenue for IFF. Ingredion competes primarily on innovation in native starches and pulse-based thickeners. Its Novation and Homethic lines provide clean-label viscosity from corn, tapioca, and potato, but the more distinct move is into pea and chickpea flours as dual-purpose thickeners and protein sources. Ingredion’s PureCircle stevia tie-in also positions it for sugar-reduced, thickened beverages. Kerry Group focuses on dairy and meat applications with its range of carrageenan and dairy protein thickeners. Kerry’s strength lies in application-specific technical support—it maintains pilot plants in major regions to help customers optimize thickening in hot-fill, retort, and frozen processes. These four players collectively hold approximately 35% market share, meaning the remaining 65% is up for grabs by nimble, regional suppliers with unique botanical sources or certified organic products.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the food additives space.

5. Market Trends

1. PLANT-BASED AND CLEAN-LABEL THICKENERS

PLANT-BASED AND CLEAN-LABEL THICKENERS — Consumers are demanding ingredients they recognize. This trend has pushed modified starches and synthetic gums off the label in favor of chickpea flour, taro powder, and citrus fiber. Cargill’s SimPure lineup exemplifies this shift—unmodified starches that provide the same viscosity with a single-ingredient declaration. HYDROCOLLOIDS IN PROCESSED FOODS | Hydrocolloids like xanthan gum and guar gum are becoming default ingredients in gluten-free, low-fat, and high-fiber products. The global hydrocolloid market is growing at 5.5% annually, driven by convenience foods. Ingredion’s introduction of a cold-water-swelling xanthan gum allows manufacturers to thicken RTD beverages without heat, saving energy and preserving flavor. NATURAL THICKENERS FROM UNDERUSED SOURCES | Okra mucilage, chia seed gel, and konjac glucomannan are gaining attention as functional thickeners with added health benefits. DuPont’s R&D in fermentation-derived gellan gum offers a sustainable alternative to agar, while small startups are commercializing pumpkin seed and flaxseed thickeners for the premium allergen-free segment. The key for B2B buyers is to vet these novel thickeners for scalability and batch consistency before committing to a switch.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two opportunities stand out. First, the clean-label conversion wave is far from saturated—only about 20% of processed foods in North America have fully transitioned to recognizable thickeners. Suppliers who can certify non-GMO, organic, and traceable starches or gums will capture premium pricing. Second, the functional beverage market (protein shakes, meal replacements, cold-brew coffees) demands thickeners that remain stable at low pH and high shear; this creates a niche for specialized hydrocolloid blends. The primary risk is regulatory fragmentation. The EU’s tightening of permitted emulsifiers and thickeners (e.g., restricting titanium dioxide) may soon apply to hydrocolloids, forcing costly reformulations. Buyers should prioritize suppliers with robust regulatory affairs teams and a diversified portfolio across multiple thickener categories to hedge against bans or sudden demand shifts.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Food Thickeners Types Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-30. All market figures are estimates and may vary from actual results.