-450x250h.webp)

-150x150h.webp)

Functional Beverages in 2026: The Gut-Hydration-Mood Revolution That's Reshaping the Beverage Aisle

Table of Contents

The global Functional Beverages Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Functional beverages are exploding in 2026. Consumers are no longer satisfied with plain soda or juice—they want drinks that do more: boost energy, improve digestion, reduce stress, and hydrate better than water. According to the latest industry trend reports, the functional beverage category is outpacing traditional soft drinks by a factor of three, with global sales projected to exceed $200 billion by the end of the decade. This guide cuts through the hype to examine what actually works, which trends are worth watching, and how buyers can identify quality suppliers on platforms like Verity Rank. A functional beverage is any non-alcoholic drink containing added ingredients—probiotics, electrolytes, adaptogens, vitamins, or plant extracts—that claims to provide a health benefit beyond basic nutrition. The segment spans everything from kombucha to electrolyte-enhanced waters, from adaptogen-infused teas to protein-packed coffee. What makes this category distinctive is its blurring of lines between food, supplement, and drink: consumers are replacing morning supplements with bottled elixirs and swapping sodas for gut-healthy alternatives. Current trends point to rising demand for globally inspired flavors like yuzu and lychee, alongside natural fruit, floral, and botanical notes. This guide is designed to help B2B buyers, brand managers, and verifiers navigate the functional beverage landscape with confidence—backed by data, not marketing fluff.

Industry Scope & Characteristics

Broad Product Portfolio

Products span energy drinks, sports drinks, vitamin water, probiotic drinks, electrolyte beverages, ginseng drinks, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Industry application and market overview for Functional Beverages Guide.

2. Market Analysis

According to the Functional Beverages Trend Report 2026, functional additions are the growth drivers shaping the category. The Top 5 beverage trends for 2026 include energy drinks targeting customers of all ages, gut health drinks, and adaptogen beverages—each segment seeing double-digit growth year-over-year. Market analysts project that the global functional beverage market will grow at a compound annual rate of 8.5% from 2024 to 2026, reaching over $220 billion in revenue. The three biggest growth drivers are clear. First, the aging global population is demanding cognitive and joint-support beverages—ginseng-infused teas and collagen waters are now standard. Second, younger demographics (Gen Z and millennials) prioritize mental clarity and mood stability, fueling the adaptogen boom. Third, the push to reduce sugar intake is causing a massive shift from carbonated soft drinks to functional alternatives—sparkling probiotic sodas and no-sugar electrolyte drinks are stealing shelf space. Energy drinks, once the domain of athletes and night-shift workers, now appeal to office professionals and parents: sugar-free variants with nootropics are the fastest-growing sub-segment. The science behind these drinks is also maturing; clinical studies on probiotic strains and adaptogenic herbs are giving legitimacy to once-fringe ingredients. For B2B buyers, this means verifying ingredient sourcing and third-party testing is no longer optional—it's a competitive necessity.

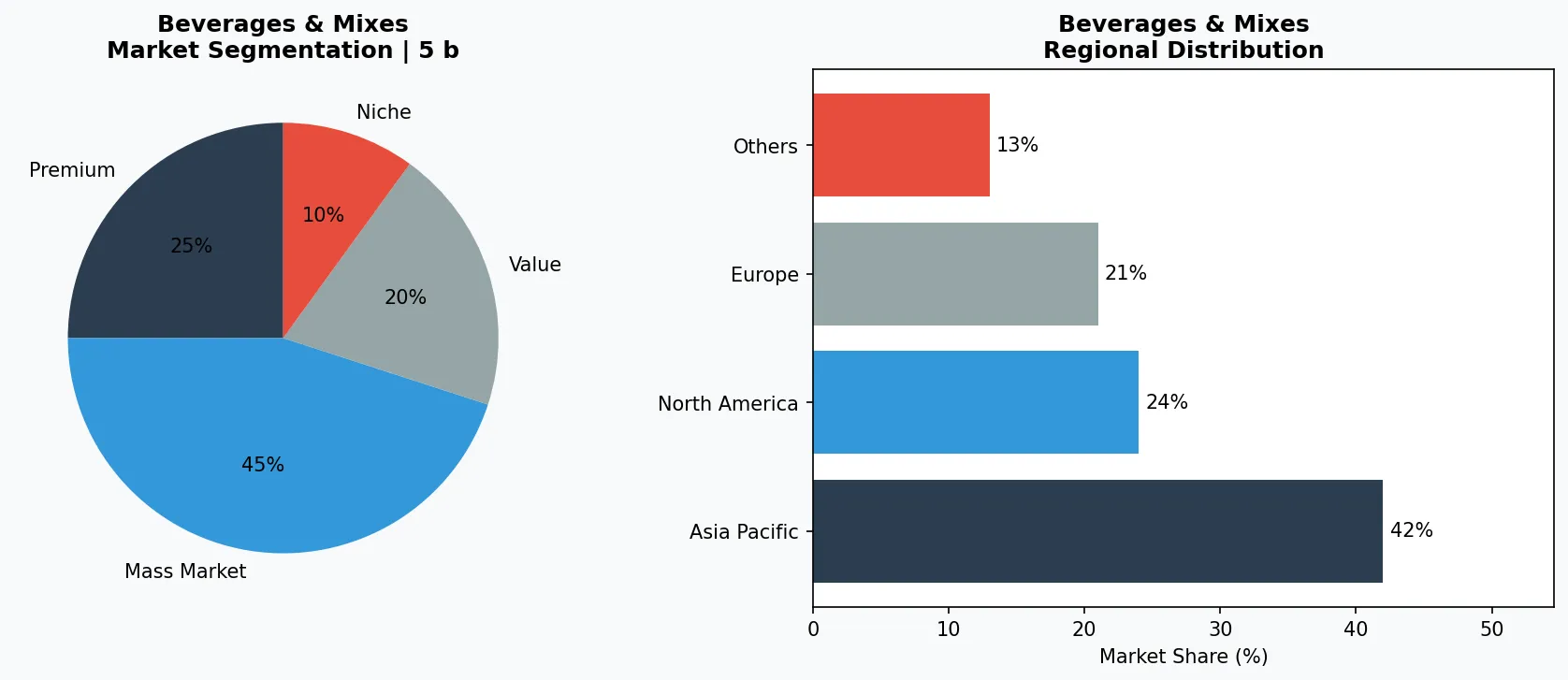

Market segmentation and regional distribution for Beverages & Mixes - Functional Beverages Guide.

3. Product Categories

Functional beverages break into three dominant product types that define the 2026 market. **Gut Health Functional Beverages** include probiotic drinks like kombucha and kefir, as well as fiber-enriched waters and prebiotic sodas. Kombucha alone is a $5 billion category, with brands like KT’s Brewing leading the fermented segment. Fiber-added drinks, such as those incorporating inulin or acacia gum, are gaining traction as consumers seek digestive regularity without pills. **Electrolyte Functional Beverages** are positioning themselves as smarter hydration than water. Enhanced waters with sodium, potassium, and magnesium—often with no added sugar—are replacing traditional sports drinks. Products like electrolyte powders and ready-to-drink coconut water with added calcium are popular among fitness enthusiasts and remote workers alike. The question 'Are hydration drinks better than water?' is being answered with clinical data showing faster rehydration rates in electrolyte beverages. **Adaptogen Functional Beverages** target stress, focus, and mood. Ingredients like ashwagandha, reishi mushroom, and rhodiola rosea are infused into sparkling waters, teas, and even coffee blends. These drinks often contain low or no caffeine, leveraging adaptogens to provide calm energy without jitters. Each product type requires distinct verification: gut health drinks need live culture stability, electrolyte drinks require accurate mineral labeling, and adaptogen drinks must prove active compound levels.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

Coca-Cola has aggressively pivoted into functional beverages, acquiring brands like BodyArmor (high-electrolyte sports drink) and Topo Chico (enhanced sparkling water). Their strategy leverages global distribution to scale functional SKUs while leveraging R&D for probiotic sodas. PepsiCo counters with Gatorade's expansion into hydration tablets and RTD electrolyte waters, plus investments in fermented teas through its partnership with KeVita. PepsiCo is also experimenting with mood-enhancing drinks under its Smartfood brand. Nestlé is betting on personalized nutrition: its Health Science division launched a line of protein-rich functional waters and cognitive beverages containing lion's mane mushroom and ginkgo biloba. Meanwhile, disruptive startups like Olipop and Poppi are redefining gut health with prebiotic sodas that taste like mainstream cola but contain 9 grams of fiber. Olipop, in particular, has grown 200% year-over-year and now competes directly with Coca-Cola's inventory. These players are Verity Rank's core client base—they need verified ingredient suppliers, certified manufacturing partners, and compliance validation to stay ahead of regulations. For B2B buyers, tracking which incumbents are acquiring which startups reveals where the market is headed.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the beverages & mixes space.

5. Market Trends

1. GLOBAL FLAVOR FUSION

GLOBAL FLAVOR FUSION — Yuzu, lychee, lemongrass, and elderflower are replacing traditional fruit and berry flavors. This matters because consumers seek exotic, Instagram-worthy experiences. Example: Japanese yuzu-infused sparkling waters from brands like Sanpellegrino's Essenza line. GUT HEALTH COMMODITIZATION | Probiotic drinks and kombucha move from niche health food stores to mass retail. Over 40% of U.S. households now purchase functional gut-health beverages, up from 22% in 2022. Example: Danone's Activia Probiotic Shot is now a top seller in convenience stores. ADAPTOGEN MAINSTREAMING | Ashwagandha and reishi appear in ready-to-drink teas and coffees. This trend is driven by mental wellness demands; one in three consumers says they drink adaptogen beverages for stress relief. Example: Recess's adaptogen-infused sparkling water has become a top seller at Whole Foods. These trends demand that B2B buyers validate ingredient potency and cross-check claims with scientific literature to avoid regulatory risk.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities stand out for 2026. First, B2B sourcing of novel functional ingredients—collagen peptides, plant-based probiotics (Bacillus subtilis), and water-soluble botanicals—can unlock private-label formulations for retailers and restaurants. Platforms like Verity Rank can help buyers vet suppliers for certifications like Non-GMO, Organic, and Kosher. Second, the rise of 'functional mixers' (cocktail-ready adaptogen spirits and prebiotic sodas) opens a new cross-category channel for beverage brands to partner with bars and hospitality groups. The primary risk is regulatory: the FDA and EFSA are intensifying scrutiny over health claims on functional beverages. Brands that fail to substantiate that their products 'support immunity' or 'reduce stress' could face fines, recalls, or worse. B2B buyers must prioritize suppliers with robust clinical trial documentation and traceable sourcing to future-proof their supply chains.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Functional Beverages Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-25. All market figures are estimates and may vary from actual results.