-450x250h.webp)

-150x150h.webp)

Lactose-Free Dairy Surpasses $15 Billion in 2026: A Guide to the Booming Market

Table of Contents

The global Lactose-Free Dairy Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

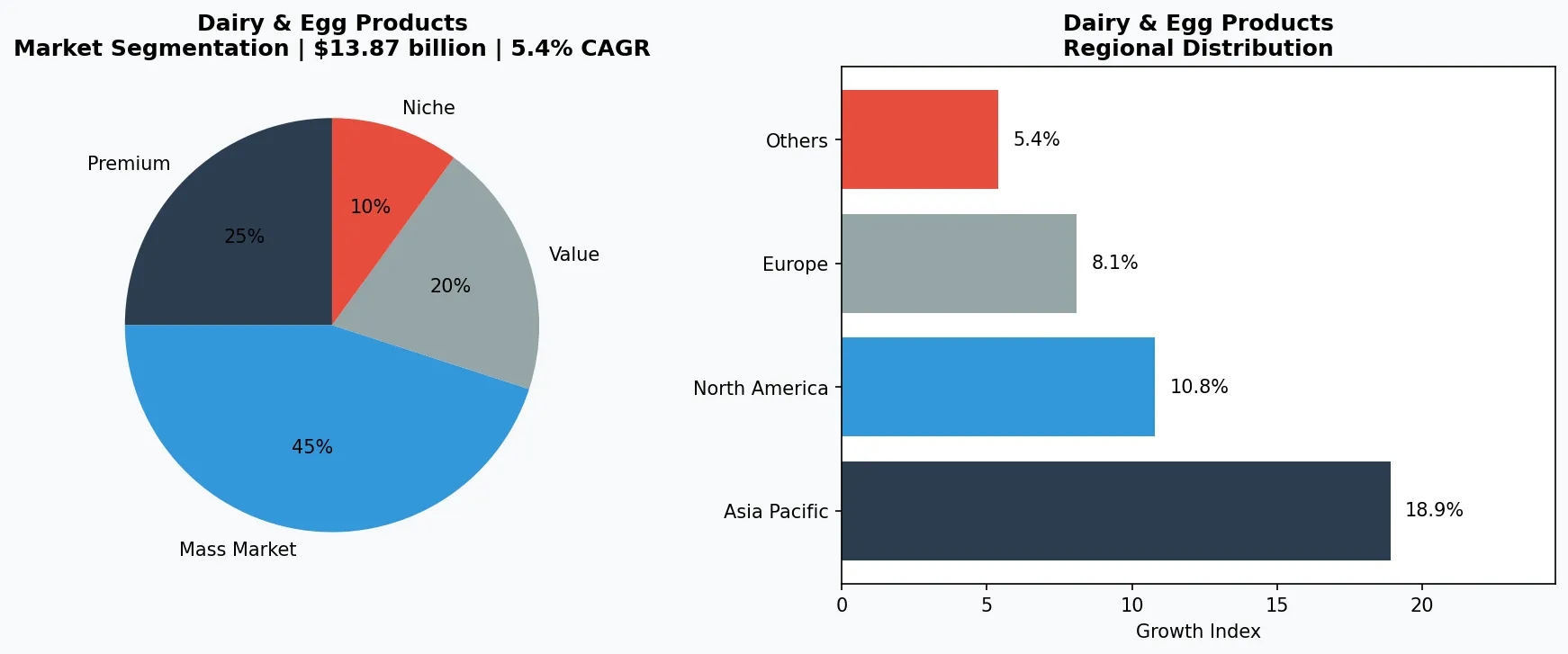

The global lactose-free dairy market is on track to hit $15.03 billion in 2026, climbing from $13.87 billion in 2025—a compound annual growth rate that signals far more than a niche shift. This isn't just about accommodating the estimated 68% of the world's population with some degree of lactose malabsorption. It's a redefinition of mainstream dairy consumption, driven by health-conscious consumers who view lactose-free as a cleaner, often higher-protein alternative to conventional milk, yogurt, and cheese. Unlike plant-based 'milks' that replace dairy altogether, lactose-free dairy retains the nutritional profile of real milk—calcium, vitamin D, and B12—while removing the sugar that triggers digestive distress. This distinction has propelled it into a standalone segment within the broader Dairy & Fresh Products market, competing directly with traditional dairy on taste and price parity. The surge is underpinned by rising awareness of digestive wellness, with over 30% of U.S. adults actively seeking lactose-free options even when not diagnosed intolerant. Major retailers now dedicate full shelves to lactose-free lines, and the segment is expanding beyond fluid milk into yogurt, cheese, butter, and even infant formula. The result is a market that is outpacing overall dairy growth by a factor of three, making it a critical area for B2B buyers and suppliers tracking the future of dairy procurement.

Industry Scope & Characteristics

Broad Product Portfolio

Products span cane sugar, brown sugar, rock sugar, powdered sugar, stevia, erythritol, coconut sugar, honey, maple syrup, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Key market segments and growth drivers in the Lactose-Free Dairy Guide sector.

2. Market Analysis

The lactose-free dairy market size has grown strongly in recent years, advancing from $13.87 billion in 2025 to a projected $15.03 billion in 2026 at a compound annual growth rate of roughly 8.4%—though the broader lactose-free food market, which includes non-dairy items, is estimated at $22.83 billion in 2026 and expected to expand at a 10.5% CAGR to reach $45.92 billion by 2033. Within dairy specifically, North America led the global market in 2025, with the U.S. segment alone forecast to grow at a 5.4% CAGR from 2026 to 2033. Three primary drivers are fueling this expansion. First, the rising prevalence of lactose intolerance diagnoses, particularly among Asian and Hispanic populations in North America, has normalized the need for lactose-free products. Second, the clean-label movement has pushed consumers to scrutinize ingredient lists; lactose-free dairy is perceived as minimally processed compared to many plant-based alternatives. Third, innovation in lactase enzyme technology has dramatically improved taste and shelf life, eliminating the sweet, caramelized flavor that once plagued lactose-free milk. Companies are now producing lactose-free versions of premium products like Greek yogurt and aged cheeses—categories that historically resisted adaptation due to texture challenges. The U.S. market's 5.4% CAGR, while lower than the global figure, reflects a mature base that is still expanding through e-commerce and foodservice channels, where lactose-free options are increasingly mandatory on menus.

Market segmentation and regional distribution analysis for Lactose-Free Dairy Guide.

3. Product Categories

The lactose-free dairy segment spans four dominant product categories, each with distinct production processes and consumer appeals. **Milk** remains the largest category, accounting for over 60% of segment revenue. Ultra-filtered milk uses physical filtration to remove lactose while concentrating protein, while enzyme-treated milk adds lactase to break down lactose after packaging. Major retailers now offer both options under private labels, with prices within 10–20% of conventional milk. **Yogurt** has emerged as the fastest-growing sub-category, driven by Greek and Icelandic styles. These strained yogurts naturally contain less lactose due to fermentation, but dedicated lactose-free lines add lactase to ensure zero tolerance—critical for consumers with severe sensitivities. Products like drinkable yogurt and probiotic-rich variants cater to the digestive health angle. **Cheese** presents a more complex landscape. Hard, aged cheeses such as cheddar, Parmesan, and Swiss naturally contain negligible lactose levels, yet many brands now offer explicit 'lactose-free' labels to capture the segment. Fresh cheeses like mozzarella and ricotta require enzyme treatment, resulting in a product that melts and stretches similarly to traditional versions. **Butter and cream** are often naturally low in lactose due to high fat content, but clarified butter (ghee) is a staple in lactose-free diets. However, value-added spreads and whipped creams now feature lactase processing to guarantee zero lactose, appealing to the premium home-baking market. Additionally, lactose-free infant formula and whey protein isolates have become specialized niches, driven by medical necessity and sports nutrition demand.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The competitive landscape is dominated by established dairy conglomerates and specialized nutritional brands. **Lactaid**, owned by McNeil Nutritionals (a Johnson & Johnson subsidiary), remains the most recognized brand in the U.S. for lactose-free milk and ice cream. Its strategy focuses on broad retail distribution and educational marketing about lactose intolerance, leveraging its first-mover advantage since the 1970s. Lactaid's recent expansion into cottage cheese and sour cream underscores its intent to own the lactose-free dairy aisle. **Danone**, through its brands like Horizon Organic and Dannon, has aggressively entered the space with lactose-free yogurt and drinkable products. Danone's strategy leverages its probiotic expertise, marketing lactose-free yogurt as a dual benefit for digestive health. The company's global supply chain allows it to produce lactose-free versions of its popular Activia and Oikos lines, offering SKUs that target both intolerance and general wellness. **Arla Foods**, the Danish cooperative, has carved out a strong position in Europe and is expanding in North America with its Arla Lactose-Free milk line. Arla's key differentiator is its 'free-from' commitment combined with sustainability credentials, using biogas from its farms. The cooperative partners with foodservice giants to supply lactose-free milk for coffee chains, a high-volume channel. **Saputo**, a Canadian dairy processor, has introduced lactose-free cheese and butter under the Dairyland and Stella brands, focusing on price competitiveness and private-label manufacturing. Its strategy emphasizes operational efficiency, capturing cost-conscious B2B buyers who need bulk lactose-free ingredients for further processing.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the dairy & egg products space.

5. Market Trends

1. HEALTH-CONSCIOUS CONSUMER SHIFT

HEALTH-CONSCIOUS CONSUMER SHIFT — Consumers are increasingly choosing lactose-free dairy not because of medical necessity but because they perceive it as a healthier, cleaner option. This trend is driving a 5.4% CAGR in the U.S. market, with brands like Lactaid and Danone reformulating existing products to carry a 'lactose-free' label even when they naturally have low lactose. The strategy works because it removes a perceived barrier, tapping into the broader 'free-from' movement.

2. TECHNOLOGICAL INNOVATION IN LACTOSE REMOVAL

TECHNOLOGICAL INNOVATION IN LACTOSE REMOVAL — Advances in enzymatic hydrolysis and ultra-filtration are allowing producers to create lactose-free dairy that tastes and behaves identically to conventional products. Arla Foods has invested heavily in proprietary lactase enzymes that eliminate the 'sweet aftertaste' once common in lactose-free milk. This technology enables the production of lactose-free hard cheeses that age and develop flavor normally, opening the category to gourmet applications.

3. E-COMMERCE AND DIRECT-TO-CONSUMER GROWTH

E-COMMERCE AND DIRECT-TO-CONSUMER GROWTH — Online sales of lactose-free dairy products are growing at over 15% annually, outpacing brick-and-mortar. Danone has launched subscription models for lactose-free yogurt and milk via its website, while third-party platforms like Thrive Market and Amazon Fresh have dedicated lactose-free sections. This channel allows brands to target niche consumers (e.g., athletes seeking lactose-free protein shakes) with detailed product information.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities define the next phase for lactose-free dairy. First, product diversification into underpenetrated categories like lactose-free butter, cream cheese, and aged specialty cheeses offers significant margin upside, as these segments currently have less than 20% lactose-free penetration compared to milk's 40% in key markets. Second, expansion into Asia-Pacific—where lactose intolerance rates exceed 90% in some populations—represents a greenfield opportunity, though infrastructure and cold-chain logistics remain hurdles. The primary risk is supply chain volatility for lactase enzymes, which are derived from microbial fermentation and currently concentrated among a few global suppliers. Any disruption could limit production capacity and raise costs, potentially slowing the segment's price convergence with conventional dairy. B2B buyers should lock in long-term contracts with enzyme suppliers and collaborate with multiple dairy processors to mitigate this risk.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Lactose-Free Dairy Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-27. All market figures are estimates and may vary from actual results.