-450x250h.webp)

-150x150h.webp)

Zero Sugar Boom: Low Sugar Beverage Trends Reshaping the $72.8 Billion Market by 2026

Table of Contents

The global Low Sugar Beverage Trends sector serves consumers worldwide with diverse solutions.

1. Industry Overview

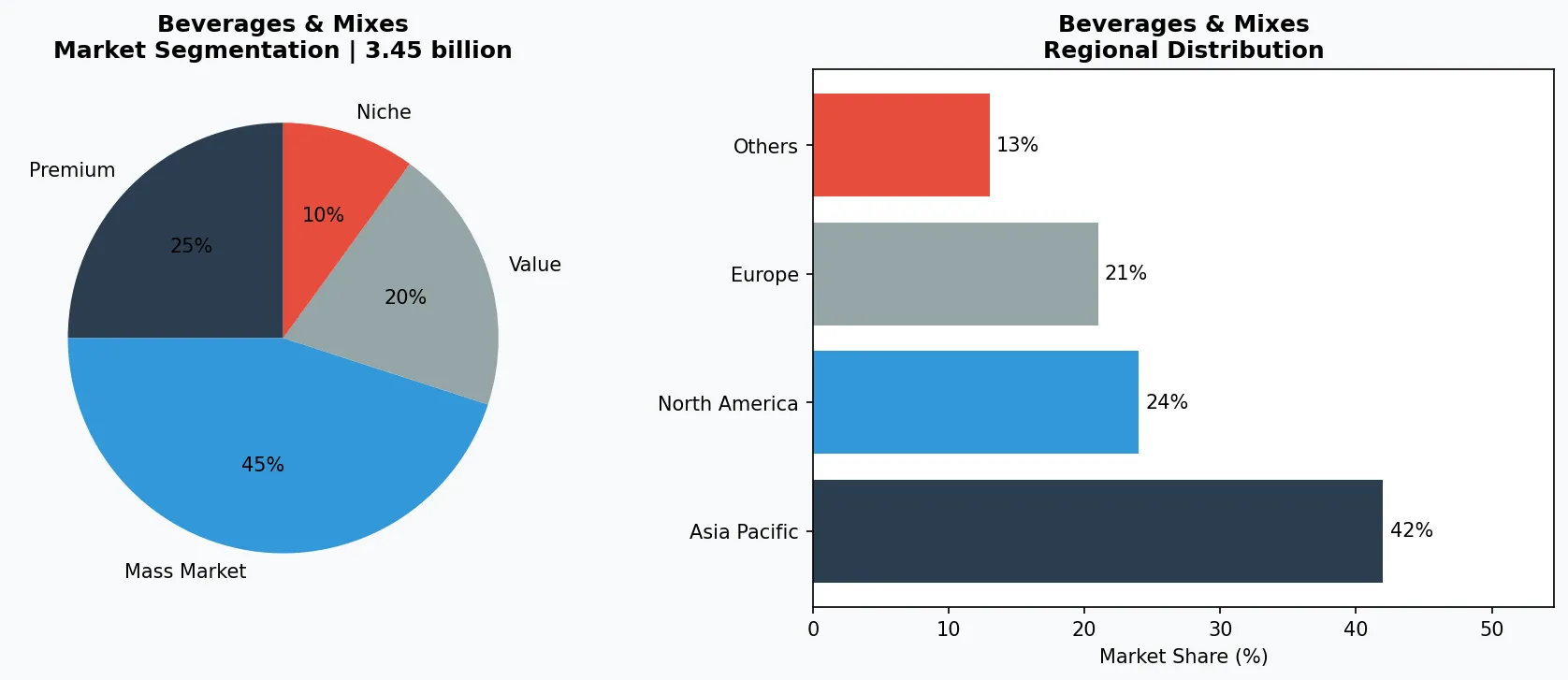

By 2026, global consumers will spend $72.8 billion on zero-sugar beverages — a figure that projects to $119.6 billion by 2033. That is not a niche; it is a mainstream upheaval. The low sugar beverage trend has moved from fringe wellness circles to the core product strategy of every major drink manufacturer. What makes this sub-topic distinctive within the broader Beverages & Mixes industry is its speed: the low sugar drink segment alone is forecast to grow from $3.45 billion in 2025 to $6.48 billion by 2032, a compound annual growth rate of 11.3%. This is nearly double the overall beverage market's pace.

Industry Scope & Characteristics

Broad Product Portfolio

Products span cane sugar, brown sugar, rock sugar, powdered sugar, stevia, erythritol, coconut sugar, honey, maple syrup, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Driven by regulatory pressures, rising diabetes rates, and a global recalibration of what 'healthy' means, low sugar beverages now span every category: soda, juice, milk tea, coffee, energy drinks, and even protein powders. The shift is not a temporary fad but a structural change in formulation and consumer expectation. Brands that ignore this trajectory risk irrelevance.

Critically, the trend is bifurcated. On one end, 'zero sugar' products—artificially sweetened with stevia, monk fruit, or sucralose—dominate shelf space. On the other, 'low sugar' products (often under 5 grams per serving) leverage natural fruit concentrates and fermentation to reduce sugar without synthetic aftertaste. Both segments are growing, but the zero-sugar category commands a valuation ten times larger than low sugar alone.

The year 2026 marks a tipping point: top beverage trend reports now rank low- to no-sugar as a top five trend, not a sub-trend. This is the moment when health-driven innovation becomes the default, not the differentiator.

Key market segments and growth drivers in the Low Sugar Beverage Trends sector.

2. Market Analysis

The global zero-sugar beverages market is valued at $72.8 billion in 2026 and is on track to reach $119.6 billion by 2033, growing at a 6% CAGR, according to industry forecasts. Meanwhile, the narrower low sugar drink segment—products with reduced but not eliminated sugar—is expanding even faster: from $3.45 billion in 2025 to $6.48 billion by 2032, a CAGR of 11.3%. These numbers reveal a dual-speed market where 'no sugar' still dominates in volume, but 'less sugar' is gaining share at a higher growth rate.

Three forces are accelerating this growth. First, government sugar taxes and front-of-pack labeling mandates in over 50 countries are forcing reformulation. For example, the UK's Soft Drinks Industry Levy, enacted in 2018, has already cut sugar sold through soft drinks by 29%. Second, the global functional beverage boom—estimated at $200 billion by 2027—has low sugar as a baseline requirement; no consumer buys a 'functional' drink that is loaded with high-fructose corn syrup. Third, the rise of continuous glucose monitors among non-diabetics has turned sugar awareness into a daily data point for millions, directly influencing purchasing decisions.

Low sugar soda deserves a spotlight: it is projected to grow at an 11.2% CAGR through 2033. The carbonated soft drink category, long the poster child for sugar excess, is now the epicenter of reformulation. Major brands have launched 'zero' variants that now outsell their full-sugar predecessors in many markets.

Regional disparities persist. North America leads in absolute value, but Asia-Pacific—particularly China and India—is the fastest-growing region for low sugar beverages, driven by rising disposable incomes and swelling rates of type 2 diabetes. In China, sugar-free tea and milk tea products have become bestsellers on platforms like Tmall and Douyin.

Market segmentation and regional distribution analysis for Low Sugar Beverage Trends.

3. Product Categories

**Zero-Sugar Sodas & Carbonated Drinks** — The most visible category. Products like Coca-Cola Zero Sugar and Pepsi Max have become permanent line extensions, not limited editions. The category is expanding into flavored sparkling water with zero sweeteners (e.g., LaCroix, Spindrift) and 'healthy' colas made with prebiotic fiber and stevia. These products now account for over 40% of total soda sales in some European markets.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

**Low-Sugar Fruit Juices & Juice Blends** — Traditional orange and apple juices, typically high in natural sugar (20-30g per cup), are being re-engineered. New launches combine vegetable juice (e.g., carrot, beet) with fruit to cut sugar by 30-50% while maintaining sweetness perception. Examples include Ocean Spray's reduced-sugar cranberry blends and Innocent's 'veggie' smoothies.

**Low/No-Sugar Functional Drinks** — Energy drinks, protein shakes, and ready-to-drink coffee now come in sugar-free versions. Monster Energy Zero Ultra, for instance, contains zero sugar and 10 calories. Similarly, protein powders and cereal drinks (e.g., Orgain, OWYN) use monk fruit or stevia to keep sugar low. Even honey-based drinks are innovating: brands now blend raw honey with green tea and lemon to reduce overall sugar content per serving.

**Reduced-Sugar Dairy & Plant-Based Milk Tea** — Bubble tea chains like Chatime and Gong Cha offer reduced-sugar (30%, 50%, or 70% sweetness) options. Packaged milk teas from brands such as Oatly have launched 'no added sugar' varieties using oat milk's natural sweetness.

4. Leading Players

**The Coca-Cola Company** — No company has bet bigger on low sugar. With over 200 reformulated products since 2020, Coca-Cola has positioned its 'Coca-Cola Zero Sugar' as a flagship brand, not a diet afterthought. In 2024, the company reported that Zero Sugar variants now account for 38% of total sparkling soft drink volume in key markets. Its R&D investments focus on next-generation natural sweeteners that mimic sucrose mouthfeel.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the beverages & mixes space.

**PepsiCo** — PepsiCo's approach is dual: aggressively expanding 'Pepsi Zero Sugar' while also acquiring and incubating low-sugar snacks and beverages (e.g., Bare Snacks, SodaStream). The company's 'Pep + Lipton' tea line and 'Gatorade Zero' leverage the same zero-sugar platform across hydration and energy occasions. In 2025, PepsiCo announced a target to reduce added sugar in its beverage portfolio by 15% by 2030.

**Nestlé** — In beverages, Nestlé focuses on low-sugar milk powders, coffee creamers, and ready-to-drink coffee. Its 'Nescafé Gold' line includes 'zero sugar' instant coffee sticks, and its 'Milo' brand has launched reduced-sugar versions in Asia. Nestlé also uses a proprietary sugar-reduction technology (enzymatic conversion) that cuts sugar by up to 30% in dairy drinks without adding artificial sweeteners.

**Unilever** — Through its 'Lipton' and 'Pure Leaf' tea brands, Unilever offers unsweetened and reduced-sugar iced teas. The company has committed to removing added sugar from all kids' beverages by 2026, and its 'Magnum' ice cream range now includes a zero-sugar-added line. Unilever's strategy ties low-sugar to broader sustainability messaging, appealing to health-conscious millennials.

5. Market Trends

1. NATURAL SWEETENER WARS

NATURAL SWEETENER WARS — The shift from artificial sweeteners (aspartame, sucralose) to plant-based sweeteners (stevia, monk fruit, allulose) is accelerating. Why it matters: consumer distrust of artificial ingredients is pushing formulators toward 'clean label' sweeteners. Coca-Cola has partnered with Amyris to develop a fermented stevia molecule that tastes closer to sugar, aiming for a 2027 launch.

2. PREBIOTIC & GUT-HEALTH SODAS

PREBIOTIC & GUT-HEALTH SODAS — Low sugar sodas infused with prebiotic fiber, apple cider vinegar, and probiotics are the fastest-growing subcategory. Brands like Poppi and Olipop have surged, with Olipop reporting 100% YoY growth. Why it matters: consumers want the soda experience without the sugar spike, and gut health adds a functional halo. Major soda companies are acquiring or developing competing products.

3. PERSONALIZED SUGAR TARGETING

PERSONALIZED SUGAR TARGETING — Apps and smart devices (e.g., Levels, Nutrisense) that monitor continuous glucose response are influencing purchase decisions. Why it matters: consumers now 'prescribe' themselves low sugar beverages based on real-time biometric data. In response, beverage brands are launching 'glucose-friendly' certifications. Nestlé's 'Glucerna' line, originally for diabetics, is being repackaged for the broader biohacking audience.

4. REGULATION-DRIVEN REFORMULATION

REGULATION-DRIVEN REFORMULATION — More than 60 countries now have sugar taxes or warning labels. Why it matters: this is not a trend that will reverse. In 2026, Brazil and Mexico are implementing stricter front-of-pack labeling laws, forcing all major beverage companies to accelerate reformulation. The cost of compliance is high, but the cost of non-compliance (loss of shelf space, fines, brand damage) is higher.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two opportunities stand out. First, the white space in low-sugar dairy and plant-based milk alternatives remains largely untapped: only 12% of flavored milk products in North America carry a low-sugar claim, compared to 45% in carbonated soft drinks. Second, the rise of e-commerce and direct-to-consumer subscription models allows smaller low-sugar brands to bypass retail gatekeepers and build loyal customer bases quickly, as seen with brands like 'Halo Top' for ice cream and 'Perfect Keto' for beverages.

The main risk is a backlash against non-nutritive sweeteners. New studies linking certain sugar alcohols and artificial sweeteners to gut microbiome disruption could shift consumer sentiment away from 'zero sugar' entirely. Any negative media cycle could push consumers toward unsweetened water and tea formats, collapsing the zero-sugar premium category. Brands must invest in transparency and clinical validation of their sweetening systems to stay ahead of this uncertainty.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Low Sugar Beverage Trends Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-25. All market figures are estimates and may vary from actual results.