-450x250h.webp)

-150x150h.webp)

Milk Tea Market to Hit $18.5 Billion by 2025: Retail and Bottled Segments Drive 14.1% CAGR in North America

Table of Contents

The global Milk Tea Category Deep Dive sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2025, the global milk tea market is projected to reach $18.5 billion, growing at a compound annual rate of 7.1% through 2033. That headline alone signals a booming category, but the real accelerant lies in two sub-streams: the North American bottled milk tea segment is surging at an astonishing 14.1% CAGR (2026–2033), while the retail channel alone will capture 26% of all bubble tea sales by 2026. This isn’t just a fad—milk tea has transitioned from a bubble tea shop novelty into a structural pillar of the broader beverages & mixes industry.

Industry Scope & Characteristics

Broad Product Portfolio

Products span taro milk tea, brown sugar boba, matcha latte, jasmine milk tea, roasted barley tea, coconut milk tea, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

What makes the milk tea category distinctive within the drinks landscape is its dual personality: on one side, indulgent, customizable bubble tea served fresh in specialty shops; on the other, increasingly sophisticated ready-to-drink (RTD) bottled products sold through supermarkets and convenience stores. The convergence of these two channels is reshaping supply chains, packaging formats, and consumer expectations. Unlike soda or plain iced tea, milk tea carries a higher perceived value and a stronger cultural resonance—particularly with Gen Z and millennial consumers in Asia, North America, and Europe.

The category also blurs traditional lines between beverages and dessert. With ingredients like tapioca pearls, fruit jellies, cheese foam, and boba, milk tea commands a premium price point and invites constant flavor innovation. This is a market where product differentiation is rapid, and brand loyalty is built through experiential retail as much as through taste. As a result, the milk tea category now influences adjacent segments such as dairy alternatives, sweeteners, and even bubble tea maker appliances—a niche itself growing at 7% CAGR through 2033.

For B2B buyers—whether sourcing bottled milk tea for retail chains or selecting suppliers for boba shop ingredients—understanding the category’s velocity and fragmentation is critical. The data shows a market that is scaling fast, but not uniformly. The opportunities are largest in RTD bottled formats and in retail distribution, where margins and shelf space are being renegotiated.

Industry application and market overview for Milk Tea Category Deep Dive.

2. Market Analysis

The global milk tea market is projected to grow from approximately USD 40.2 billion in 2026 to USD 64.6 billion by 2034, representing a compound annual growth rate of 7.8%. This top-line number, however, masks significant variance by region and format. The North America bottled milk tea segment is the standout performer, expected to expand at a blistering 14.1% CAGR from 2026 to 2033—nearly double the global average. This is driven by increasing distribution in mainstream grocery chains, rising Asian-American demographics, and the convenience of premium RTD options.

Three key growth drivers define this market. First, the retail channel: bubble tea sales through retail outlets are forecast to account for 26% of all bubble tea sales in 2026. This is a structural shift away from exclusively shop-based consumption. Supermarkets, convenience stores, and even dollar stores are aggressively adding shelf-stable bottled milk tea SKUs. Second, the milk tea maker appliance segment is growing at a 7% CAGR (2026–2033), signaling that consumers are replicating the bubble tea experience at home—driving demand for powder mixes, syrups, and tapioca pearls in bulk. Third, health-conscious innovation is expanding the addressable market: low-sugar, plant-based, and functional ingredient variants are pulling in new consumers who previously avoided milk tea due to its sugar load.

Geographically, Asia-Pacific still dominates total volume, but North America and Europe are the fastest-growing regions in revenue terms. The U.S. bottled milk tea market alone is seeing double-digit growth, buoyed by brands that emphasize authentic flavors and clean labels. Meanwhile, the milk tea powder and concentrate segments are growing in tandem, as foodservice operators seek consistent, cost-efficient bases for their shop menus. For suppliers, the takeaway is clear: the retail-ready bottled segment offers the highest growth trajectory, but requires investment in shelf-stable packaging and longer shelf lives.

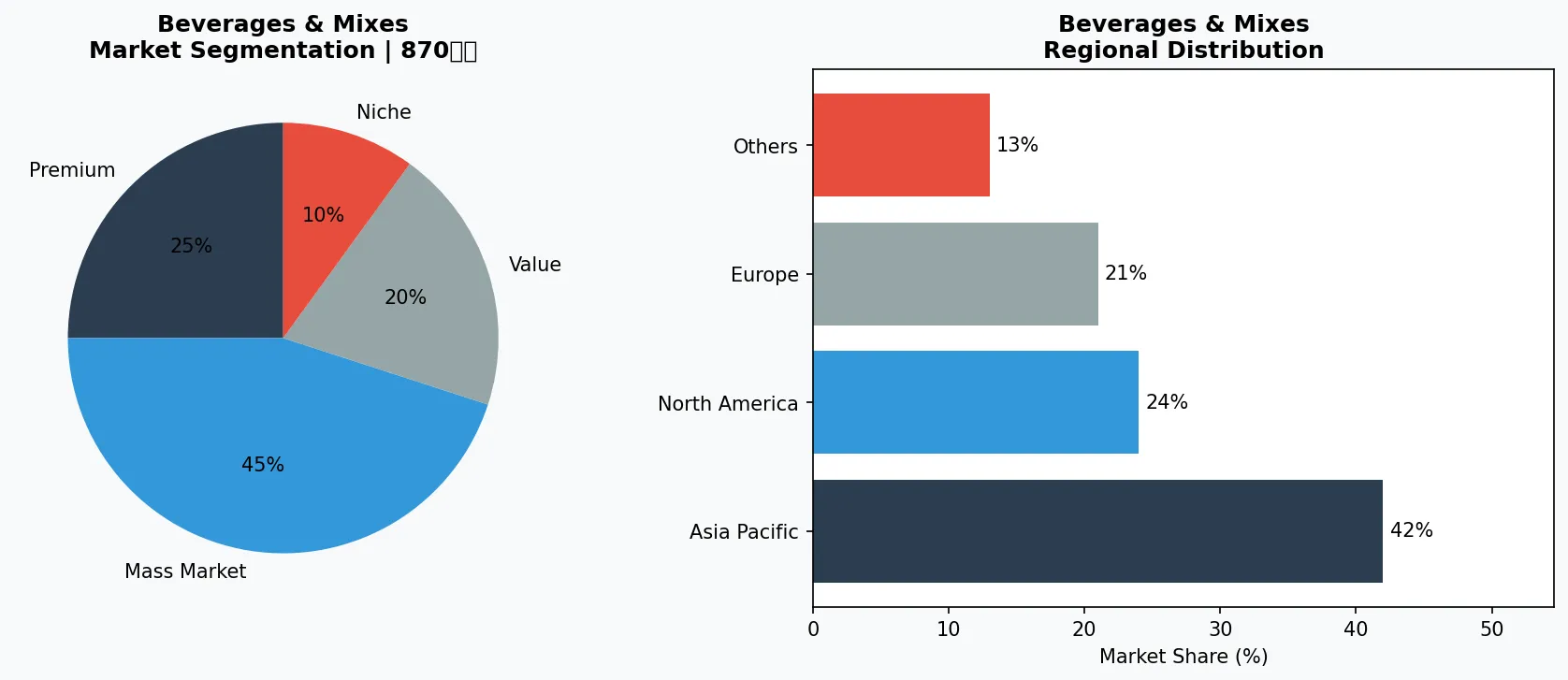

Market segmentation and regional distribution for Beverages & Mixes - Milk Tea Category Deep Dive.

3. Product Categories

The milk tea category can be broken into three core product sub-types, each with distinct supply chains and consumer use cases.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

**Bottled / Ready-to-Drink (RTD) Milk Tea** – This is the fastest-growing sub-segment, especially in North America. These products are shelf-stable or refrigerated, often packaged in PET bottles or cans. Examples include popular Asian RTD brands that use UHT processing to maintain flavor without preservatives. Retailers value the long shelf life and consistent quality, while consumers appreciate grab-and-go convenience. The North America RTD sub-segment is the primary driver of the 14.1% CAGR figure.

**Bubble Tea Shop Ingredients** – This encompasses tapioca pearls (boba), flavored syrups, fruit powders, non-dairy creamers, and tea bases sold to bubble tea chains and independent shops. These are often bulk-packaged for commercial use. The market here is driven by new flavor launches and the demand for “cleaner” ingredients, such as tapioca pearls without artificial colors. Shop-grade products require reliable cold chain logistics for fresh toppings.

**Milk Tea Powders and Mixes** – Targeted at both foodservice operators and home consumers, these dehydrated blends typically include tea powder, creamer, and sweetener. The home-use segment is surging alongside the milk tea maker appliance market (7% CAGR). Brands are launching single-serve sachets and stand-up pouches for easy preparation. This sub-category is particularly attractive for B2B buyers looking to enter the market quickly without investing in liquid packaging lines.

4. Leading Players

The milk tea category lacks a single dominant global player, creating fragmentation that favors specialized suppliers and nimble brands.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the beverages & mixes space.

**Bottled milk tea manufacturers** have emerged as key players in the RTD space. Incumbent beverage conglomerates are acquiring or partnering with Asian milk tea brands to enter the segment. Their strategy focuses on scaling production via UHT lines, securing supermarket shelf space, and launching limited-edition seasonal flavors. These players benefit from existing distribution networks but face competition from smaller, authenticity-first brands that resonate with younger consumers.

**Bubble tea chains** are the traditional heart of the category, but they are increasingly pivoting to retail. Major chains are launching bottled versions of their signature drinks for sale in convenience stores, effectively becoming both retailers and CPG brands. Their strategy leverages brand loyalty and proprietary recipes. They also invest heavily in supply chain control for tapioca pearls and tea leaves to ensure consistency across hundreds of locations globally.

**Milk tea maker appliance companies** represent a distinct but growing player group. These firms manufacture countertop machines that automate the preparation of bubble tea at home. Their market is growing at a 7% CAGR, driven by the post-pandemic stay-at-home trend. Their strategy includes bundling machines with starter kits of powder mixes and reusable straws, creating recurring revenue streams for consumables. They often partner with online influencers for direct-to-consumer sales.

5. Market Trends

1. RETAIL CHANNEL DOMINANCE

RETAIL CHANNEL DOMINANCE — The retail segment is forecast to capture 26% of bubble tea sales by 2026, up from an estimated 18% in 2023. This shift matters because it opens the category to larger, more consistent revenue streams outside seasonal café traffic. Major retailers are expanding their Asian beverage sections, and bottled milk tea is often placed alongside kombucha and energy drinks. This trend pressures suppliers to deliver longer shelf lives and eye-catching packaging that works on shelves.

2. HEALTH INNOVATION

HEALTH INNOVATION — Low-sugar and plant-based milk tea variants are growing twice as fast as standard offerings. Brands are reformulating with oat milk, coconut cream, and natural sweeteners like monk fruit. This matters because it addresses the primary barrier to repeat purchase for health-conscious demographics—sugar content. Companies are launching “less sweet” versions and transparent nutritional labeling to capture this segment.

3. HOME BREWING CONVENIENCE

HOME BREWING CONVENIENCE — The milk tea maker appliance market is expanding at a 7% CAGR (2026–2033), indicating that consumers want café-quality drinks at home. This trend matters because it amplifies demand for milk tea powder mixes, syrups, and pre-cooked tapioca pearls sold through e-commerce. Suppliers who can offer B2B bulk packs to appliance manufacturers will gain a foothold in this emerging channel.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities stand out. First, expanding RTD bottled milk tea into untapped retail channels like drugstores and gyms—these outlets have low penetration for the category but high foot traffic from the target demographic. Second, creating functional milk tea blends (e.g., added collagen, probiotics, or caffeine alternatives) to differentiate from incumbent sugary versions. Both opportunities require supplier partnerships for clean-label formulations and shelf-stable packaging.

One concrete risk: tapioca pearl supply volatility. The majority of tapioca starch comes from Southeast Asia, where climate and logistics disruptions are increasing. A sustained shortage would impact both bubble tea shops and home-use product availability. B2B buyers should diversify sourcing and consider alternative toppings like popping boba or jelly cubes to mitigate dependency.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Milk Tea Category Deep Dive Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-25. All market figures are estimates and may vary from actual results.