-450x250h.webp)

-150x150h.webp)

Mineral Fortification to Surpass $158 Billion by 2036: The Silent Revolution in Food Additives

Table of Contents

The global Mineral Food Fortification sector serves consumers worldwide with diverse solutions.

1. Industry Overview

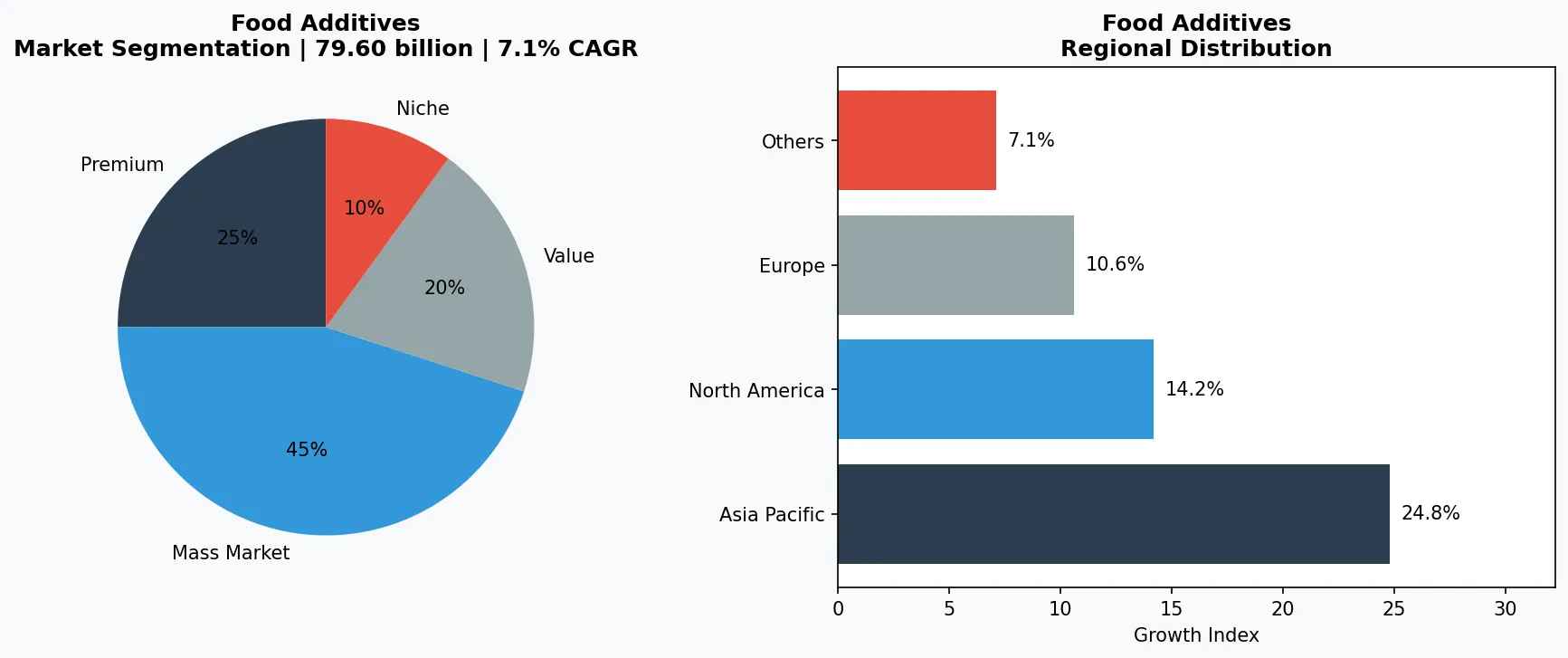

By 2026, the global mineral fortification market is projected to hit $79.60 billion—and that’s just the starting line. According to Future Market Insights, this segment is expected to nearly double to $158.06 billion by 2036, expanding at a compound annual growth rate (CAGR) of 7.1%. That pace outpaces the broader fortified foods industry, which is itself on a tear: from $176.81 billion in 2026 to $347.90 billion by 2034, growing at 8.83% CAGR. What’s driving this surge? Mineral food fortification—the targeted addition of essential minerals such as calcium, iron, zinc, and iodine to everyday foods and beverages—is no longer a niche public health measure. It has become a mainstream commercial strategy for food manufacturers worldwide. Unlike other food additives that focus on taste, color, or shelf life, mineral fortification directly addresses the global epidemic of micronutrient deficiencies, known as 'hidden hunger.' The World Health Organization estimates that over 2 billion people lack essential vitamins and minerals, creating a massive demand pull. At the same time, regulatory bodies in over 80 countries now mandate or encourage fortification of staples like flour, salt, and milk. This unique intersection of consumer health awareness, regulatory tailwinds, and industry innovation makes mineral fortification a distinctive and fast-growing segment within the broader food additives landscape. It also presents a clear opportunity for B2B buyers and suppliers who understand the supply chain dynamics—from ingredient sourcing to formulation and compliance.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Mineral Food Fortification, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Key market segments and growth drivers in the Mineral Food Fortification sector.

2. Market Analysis

The numbers tell a compelling story. The food fortification ingredients market, according to industry reports, is projected to grow annually by 5.3% from 2026 to 2033, with mineral fortification being the largest sub-segment. Breaking down the $79.60 billion projection for 2026: calcium fortification leads, accounting for roughly 35% of revenue, driven by its dominance in dairy alternatives, cereals, and bakery products. Iron and zinc follow, together representing nearly 30% of the market, fueled by wheat flour and rice fortification programs in Asia and Africa. Iodine, while smaller in volume, commands premium pricing due to its critical role in salt iodization programs in over 120 countries. Three growth drivers stand out. First, rising consumer demand for functional foods—products that offer health benefits beyond basic nutrition. In 2025 alone, the global functional food market exceeded $275 billion, with mineral-enriched products capturing an increasing share. Second, aggressive government mandates. For example, India’s Food Safety and Standards Authority expanded mandatory fortification of wheat flour and rice in 2024, directly impacting domestic and import ingredient demand. Third, the clean label movement is pushing manufacturers toward bioavailable mineral forms—such as calcium citrate malate and ferrous bisglycinate—which command higher margins. Regionally, Asia-Pacific is the fastest-growing market, projected to register a CAGR of 8.2% through 2036, owing to large-scale malnutrition programs and a rapidly expanding middle class. North America remains dominant in value terms, with the U.S. fortified breakfast cereal and plant-based milk sectors alone representing over $12 billion in annual sales.

Market segmentation and regional distribution analysis for Mineral Food Fortification.

3. Product Categories

Mineral fortification spans four primary product categories, each with distinct application profiles and market dynamics. **Calcium**: The largest segment, used extensively in dairy alternatives (almond milk, oat milk), breakfast cereals, and bakery products. Popular forms include calcium carbonate and calcium phosphate. A key trend is the shift toward microencapsulated calcium to avoid texture issues in clear beverages. **Iron**: Critical for combating anemia, iron fortification is most common in wheat flour, maize meal, and infant cereals. Electrolytic iron and ferrous fumarate are widely used, but new ingredient technologies like sodium iron EDTA (NaFeEDTA) offer higher bioavailability without color changes—a major advantage in rice and pasta. **Zinc**: Increasingly added to snack foods, nutrition bars, and infant formula. Zinc oxide and zinc sulfate dominate, but chelated forms like zinc glycinate are gaining traction for superior absorption. **Iodine**: Mostly deployed in table salt and animal feed. Potassium iodate is the standard form, but organic iodine sources (e.g., kelp extract) are emerging in the premium segment. Beyond these four, trace minerals like selenium and chromium are carving out niche applications in sports nutrition and diabetic-friendly foods. The innovation frontier is in multi-mineral premixes that allow food manufacturers to fortify with a single blend, reducing inventory complexity. Leading premix suppliers now offer customized blends that adhere to both CODEX Alimentarius and regional regulations, enabling global scalability.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The mineral fortification ecosystem comprises three tiers of players, each with distinct strategic approaches. First, **global ingredient manufacturers**—companies that produce the base mineral salts and chelates. These firms invest heavily in purification, particle size control, and bioavailability studies. One leader in this space focuses on organic mineral chelates, securing exclusive supply agreements with major infant formula producers. Another dominates the calcium carbonate market with proprietary wet-milling technology that achieves sub-micron particle sizes, ideal for clear beverages. Second, **premix and custom-blend specialists** that combine multiple minerals with vitamins and excipients. These companies act as intermediaries, delivering ready-to-use fortification blends to food processors. Their competitive edge lies in R&D: developing stable formulations that withstand high heat, pH extremes, and shelf life requirements. One notable firm has patented a microencapsulation technology that masks the metallic aftertaste of iron and zinc, a common consumer complaint. Third, **contract manufacturers and toll processors** that offer end-to-end fortification services for smaller food brands. They provide sourcing, blending, packaging, and regulatory compliance—critical for startups entering the functional food space. Supply chain transparency is a growing differentiator: several major players now offer blockchain-based traceability for mineral sourcing, especially for iron and zinc from conflict-free zones. The competitive landscape is consolidating, with three top firms controlling over 45% of the global mineral premix market, but niche regional suppliers in India and China are gaining share by offering cost-effective calcium and zinc products tailored to local taste preferences.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the food additives space.

5. Market Trends

1. CLEAN LABEL MINERAL FORMS

CLEAN LABEL MINERAL FORMS — What it is: Shift from synthetic mineral salts to 'clean label' alternatives such as algal calcium, seaweed-derived iodine, and plant-based iron from legumes. Why it matters: Consumers are scrutinizing ingredient lists, rejecting additives with chemical-sounding names. Fortified foods using organic mineral sources can command 15-25% price premiums. Industry response: Global ingredient manufacturers are investing in fermentation-based mineral production. One major supplier launched a chelated iron derived from chickpea protein in 2025.

2. MICROENCAPSULATION AND DELIVERY SYSTEMS

MICROENCAPSULATION AND DELIVERY SYSTEMS — What it is: Encasing mineral particles in lipid or polysaccharide coatings to improve stability, mask taste, and control release in the digestive tract. Why it matters: Prevents mineral interactions with other ingredients (e.g., iron causing rancidity in cereals) and allows fortification of clear liquids. One leading premix company commercialized a double-encapsulated zinc system for sports drinks in 2024, achieving 98% retention after six months.

3. PERSONALIZED FORTIFICATION

PERSONALIZED FORTIFICATION — What it is: Tailored blend programs using AI-driven analysis to match mineral profiles to specific demographic needs (e.g., high-iron blends for women of childbearing age, zinc-rich for elderly). Why it matters: Food brands can differentiate with 'targeted wellness' positioning. A contract manufacturer now offers a drop-ship model where consumers receive customized fortified baking mixes based on self-reported health data.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities stand out for B2B stakeholders. First, the growing demand for fortified plant-based dairy alternatives—milk, yogurt, and cheese analogs—presents a $5 billion addressable market by 2028. Manufacturers that can supply calcium and vitamin D3 in stable, vegan-compatible forms will capture early-mover advantages. Second, the push for large-scale biofortification of staple crops in Sub-Saharan Africa and Southeast Asia offers long-term procurement contracts for iron and zinc premixes, with multilateral organizations like the World Food Programme tendering multimillion-dollar agreements. However, a significant risk looms: over-fortification and regulatory backlash. As more food categories become fortified (snacks, bottled water, even alcoholic beverages), cumulative intake of certain minerals—especially iron—can exceed safe upper limits, particularly for children and individuals with genetic disorders like hemochromatosis. Regulators in the EU and Canada are already reviewing maximum addition limits. Companies that invest in rigorous safety testing and clear labeling will be best positioned to navigate this tightening landscape.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Mineral Food Fortification Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-30. All market figures are estimates and may vary from actual results.