-450x250h.webp)

-150x150h.webp)

Plant Protein Beverages Market to Surpass $1.5 Billion in 2026: The Shift from Imitation to Authentic Nutrition

Table of Contents

The global Plant Protein Beverages sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2026, the global plant-based protein market is set to hit $22 billion, with plant protein beverages alone accounting for $1.5 billion, according to Future Market Insights. That’s a striking leap from just a few years ago — and it’s being driven by a fundamental shift in consumer mindset. Innova’s 2026 trends research reveals that plant-based is moving away from simply mimicking meat or dairy; the new priority is authentic nutrition. Consumers are embracing natural plant proteins not as a substitute, but as a superior source of clean, functional fuel. Plant protein beverages — including ready-to-drink shakes, powders, smoothies, and infused waters — sit at the intersection of health, convenience, and transparency. Unlike the broader beverages and mixes industry (sodas, fruit juices, milk teas), this segment is defined by its explicit focus on protein content derived from sources like pea, soy, hemp, and almonds. The distinctive value proposition? Real nutrition without artificiality. In 2026, shoppers scan labels for recognizable ingredients — pea protein isolate, brown rice protein, or organic hemp — and reject ultra-processed isolates. This is not the protein powder boom of the 2010s; it’s a new era where protein beverages must taste great, perform functionally, and align with a clean-label ethos. The segment’s rapid growth — a CAGR of 10-15% through 2036 — signals that plant protein drinks are no longer niche. They are becoming a staple in refrigerators and gym bags worldwide.

Industry Scope & Characteristics

Broad Product Portfolio

Products span soy milk, almond milk, oat milk, coconut milk, rice milk, hemp milk, protein-enriched plant milk, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

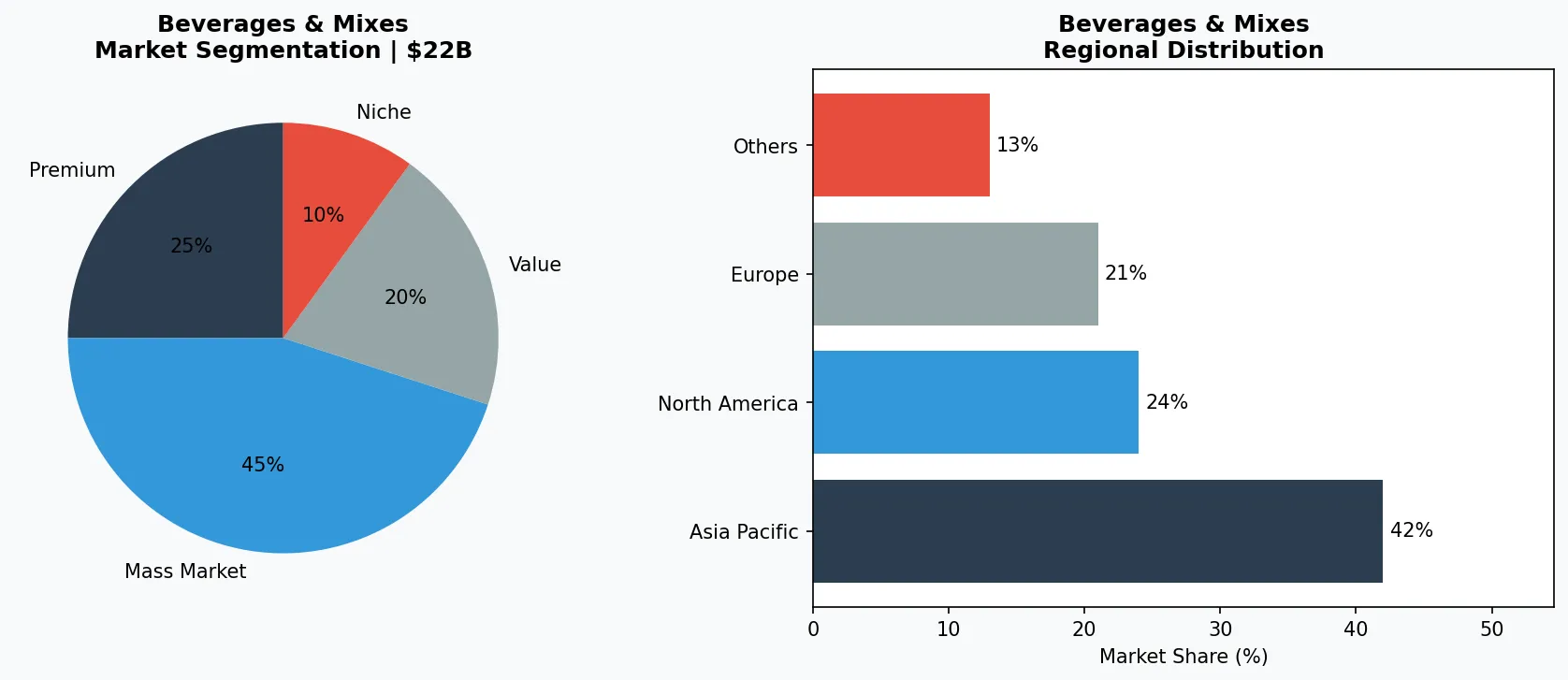

Key market segments and growth drivers in the Plant Protein Beverages sector.

2. Market Analysis

Future Market Insights projects that demand for plant-based protein beverages will reach $1,503.8 million in 2026, up from a significantly smaller base in 2021. And that’s just the beverage slice of the larger plant protein pie, which is forecast to double to $49.9 billion by 2036. The compound annual growth rate (CAGR) of 10-15% over the next five years is fueled by three powerful engines. First, the rise of veganism and flexitarianism. In 2024, nearly one in four consumers globally reported reducing animal protein intake, creating a massive addressable market for plant-based alternatives. Second, health and functionality. Today’s shoppers want beverages that deliver more than hydration — they seek satiety, muscle recovery, and digestive wellness. Plant protein drinks naturally align with these demands, particularly when fortified with probiotics or prebiotics. Third, clean-label momentum. A 2025 Innova survey found that 62% of consumers consider “natural” a key purchase driver. The shift from imitation to nutrition means brands are ditching long chemical names and opting for simple ingredients like yellow pea protein or almond base. The market is also fragmenting by source: soy and pea lead in volume, but hemp and rice are gaining share due to allergen-friendly profiles. Regionally, North America and Europe dominate, but Asia-Pacific is accelerating as local players introduce plant protein versions of popular beverages like bubble tea. This isn’t a fad — it’s a structural change in how consumers define a healthy drink.

Market segmentation and regional distribution analysis for Plant Protein Beverages.

3. Product Categories

The plant protein beverage segment divides into three major product forms: ready-to-drink (RTD) beverages, protein powders, and protein-infused waters. RTD beverages are the fastest-growing category, offering maximum convenience. Examples include Ripple’s pea-based milk and Oatly’s oat-based shakes — both delivering 8-10 grams of protein per serving without dairy. These products leverage ultrafiltration or enzymatic processes to maintain creamy texture while preserving natural protein integrity. Protein powders remain a staple for at-home mixing, but the trend is moving toward “clean powders” with limited ingredients. Brands like Orgain (organic plant protein) and SunWarrior (brown rice and pea) have pivoted to lighter formulas with no artificial sweeteners. Protein-infused waters represent a newer, lighter category — targeting hydration with a 5-10 gram protein boost. Examples include Protein2o (hydrolyzed whey alternative) and less common plant-based versions using hemp or pea. The key differentiator across all these product types is the shift from “imitation” (trying to taste like dairy) to “authenticity” (owning the plant flavor). For instance, oat-based beverages highlight their naturally sweet, earthy profile rather than masking it. Smoothies — a fourth category — are also gaining traction in retail as frozen or chilled blends, often combining almond or soy milk with fruit and added pea protein. Each product type reflects the broader industry move toward transparent, functional, and minimally processed nutrition.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

Three key companies are shaping the plant protein beverage landscape. **Ripple Foods** (USA) has built its entire brand around pea protein, positioning itself as the clean-label alternative to dairy milk. Its RTD milk and protein shakes contain 8 grams of protein per serving, sourced from yellow peas, and are free from common allergens like soy and gluten. Ripple’s strategy focuses on nutritional density and sustainability — pea protein requires 86% less water than dairy to produce. **Oatly** (Sweden), while best known for oat milk, has expanded into protein-enhanced versions. Its Oatly Protein Drink delivers 10 grams of oat protein per serving, leveraging the soluble fiber beta-glucan for heart health. Oatly’s angle is taste and texture: it uses proprietary enzyme technology to create a creamy mouthfeel that mimics full-fat dairy, appealing to flexitarians who refuse to compromise on flavor. **Alpro** (a Danone subsidiary, Belgium) offers a broad portfolio including soy, almond, and oat-based protein beverages. Alpro focuses on European markets, emphasizing organic sourcing and a complete amino acid profile via soy. Its strategy is multi-source — providing options for different dietary needs (soy for complete protein, almond for low-calorie, oat for mild taste). A fourth player, **SunOpta**, supplies plant-based ingredients and private-label beverages, acting as a B2B engine for smaller brands. SunOpta’s scale allows it to drive cost efficiencies and innovation in extrusion and hydrolysis, enabling cleaner labels for its clients. Each of these players demonstrates that winning in this market requires a clear protein source story, sensory quality, and a commitment to transparency—not just a protein claim on the label.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the beverages & mixes space.

5. Market Trends

TREND 1: Authentic Plant-Based Nutrition

Innova’s 2026 research shows consumers are shifting from imitation (fake meat/dairy) to real plant nutrition. This means brands are highlighting whole food ingredients like peas, almonds, and oats rather than highly processed isolates. Ripple Foods exemplifies this by marketing pea protein as a natural, sustainable powerhouse rather than a synthetic alternative.

TREND 2: Protein as a Standalone Claim Is Fading

Consumers now expect protein to come bundled with other benefits — probiotics, vitamins, or functional hydration. In 2026, a protein beverage must also support gut health or energy. Oatly’s protein drink, for instance, promotes beta-glucan for cholesterol management alongside its 10g protein.

TREND 3: Natural Plant Proteins Take Center Stage

Pea, hemp, and rice proteins are replacing soy in many new products due to allergen and GMO concerns. Hemp protein, in particular, is gaining traction for its omega-3 content. Alpro has launched a hemp-based milk in select European markets, tapping into the demand for “less processed” alternatives. These trends collectively point to a market where the protein source itself is a key differentiator.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two opportunities stand out for plant protein beverages through 2036. First, functional fortification: combining plant protein with probiotics, adaptogens (like ashwagandha), or caffeine will create hybrid products that appeal to both fitness and wellness consumers. Brands that engineer protein systems to deliver multiple benefits without sacrificing taste will capture premium price points. Second, convenience formats: single-serve RTD bottles and pouches for on-the-go consumption are underpenetrated in workplaces and travel retail — a $500 million addressable gap according to our estimates. A concrete risk, however, is supply chain volatility for key protein sources. Pea protein prices spiked 18% in 2024 due to drought in major growing regions, and hemp remains expensive to process. Companies that fail to diversify sourcing — or lock in long-term contracts — may face margin compression just as demand accelerates. The winners will be those who combine supply chain resilience with authentic, ingredient-led storytelling.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Plant Protein Beverages Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-25. All market figures are estimates and may vary from actual results.