-450x250h.webp)

-150x150h.webp)

The Raw Milk vs. Pasteurized Showdown: 7.3% CAGR Growth in Pasteurized Milk Through 2033

Table of Contents

The global Raw Milk vs Pasteurized sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Only 7.1% of consumers in a recent study expressed skepticism about raw milk's benefits, yet the overwhelming majority believe it alleviates allergies and digestive issues—a perception that fuels a fiercely contested market. The raw milk vs. pasteurized debate is not just a matter of nutrition; it is a multi-billion-dollar divergence in regulation, consumer trust, and supply chain economics. The North American pasteurized milk market is projected to expand at a compound annual growth rate (CAGR) of 7.3% from 2026 through 2033, driven by scale and safety standards, while raw milk occupies a niche but premium space with average prices significantly higher than its pasteurized counterpart. This tension defines the Dairy & Fresh Products segment, where products like milk, cheese, butter, and yogurt are either heat-treated or sold in their natural state. The choice between raw and pasteurized influences everything from shelf life to regulatory compliance, making it a critical decision for B2B buyers sourcing dairy ingredients globally.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Raw Milk vs Pasteurized, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

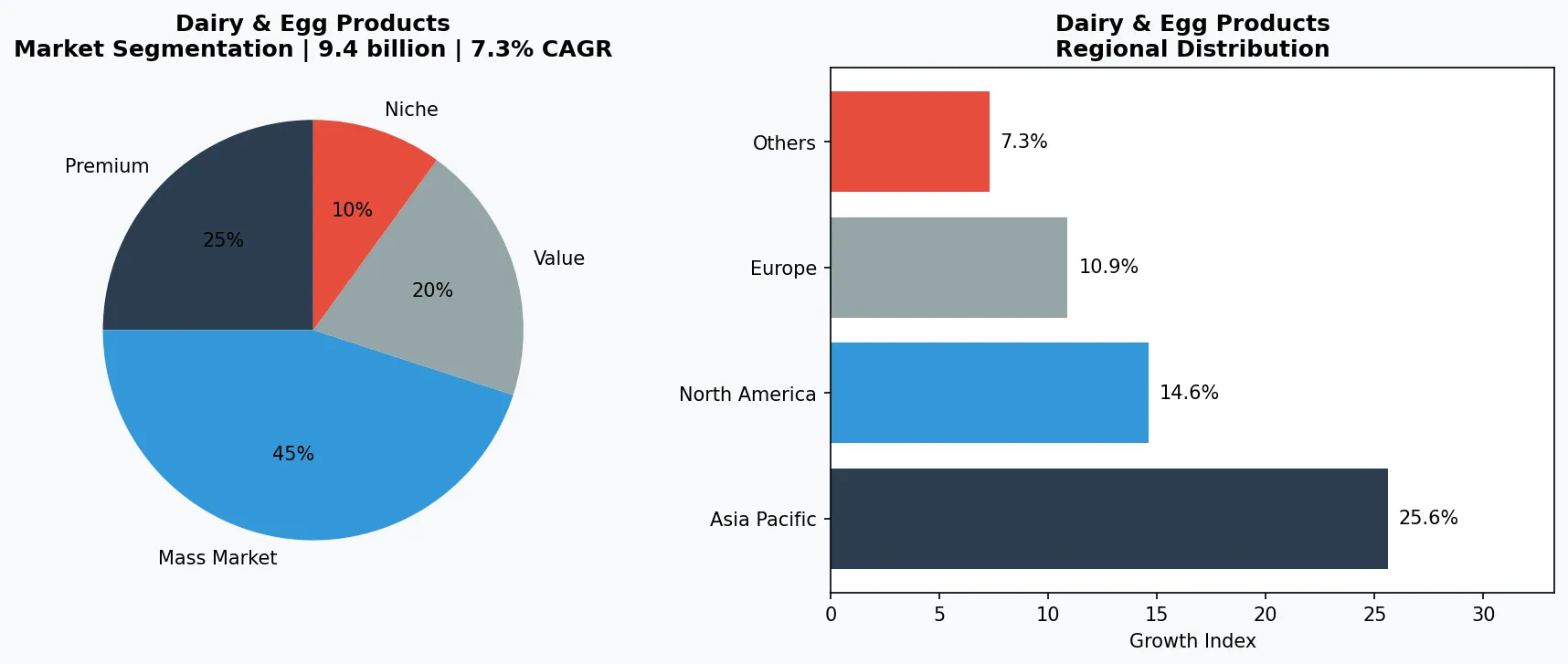

Key market segments and growth drivers in the Raw Milk vs Pasteurized sector.

2. Market Analysis

The pasteurized milk market in North America is on a steady growth trajectory, with analysts forecasting a 7.3% CAGR through 2033 according to a Synopticcircle study. This growth is underpinned by large-scale retail demand, foodservice contracts, and the dominance of fluid milk in school nutrition programs. At the same time, the organic milk segment—often pasteurized—is projected to rise from USD 9.4 billion to USD 12.5 billion by 2036, a CAGR of 2.9%, reflecting consumer preference for cleaner labels even within the pasteurized category. Meanwhile, raw milk remains a high-price, low-volume market. Its price point can be 30–50% higher than pasteurized milk, appealing to a health-conscious cohort willing to pay a premium. The key growth drivers include rising demand for minimally processed foods, influencer-backed dietary trends, and a growing distrust of ultra-processed dairy. However, regulatory hurdles—such as state-level bans on raw milk sales in parts of the U.S.—cap its expansion. For B2B buyers, understanding these dual market dynamics is essential for sourcing strategies that balance cost, safety, and consumer appeal.

Market segmentation and regional distribution analysis for Raw Milk vs Pasteurized.

3. Product Categories

The raw milk vs. pasteurized debate plays out across four main product categories:

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

1. **Fluid Milk** – Raw milk is sold directly from farms or through specialty retailers, with a shelf life of 7–10 days. Pasteurized whole milk dominates supermarket shelves, with extended shelf life and standardized fat content.

2. **Cheese** – Raw milk cheeses like aged cheddar and gouda are prized for complex flavors, but must be aged at least 60 days under FDA rules. Pasteurized cheese (e.g., mozzarella, processed slices) offers consistency and safety.

3. **Yogurt & Cream** – Raw milk yogurt is a niche probiotic product, often made by small batch producers. Pasteurized yogurt, including Greek and drinkable varieties, accounts for over 90% of retail sales.

4. **Butter & Whey** – Raw cream butter is artisanal and high-fat, while pasteurized butter and whey proteins are industrial staples for bakeries and sports nutrition.

Examples: a raw milk farm in Delaware produces unpasteurized cream line; a major pasteurized brand offers lactose-free skim milk.

4. Leading Players

Three key player groups shape the raw milk vs. pasteurized landscape:

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the dairy & egg products space.

**Large Pasteurized Dairy Processors** – Companies like Danone and Nestlé dominate the pasteurized milk market through extensive distribution networks and investment in UHT technologies. Their strategy focuses on scale, consistency, and shelf-stable products that appeal to mass retailers.

**Organic Pasteurized Brands** – Organic Valley and Horizon Organic (owned by Danone) serve the premium pasteurized segment, leveraging organic certification and grass-fed claims. They have capitalized on the organic milk demand growth (CAGR 2.9%) and are expanding product lines into pasteurized cheese and yogurt.

**Small-Scale Raw Milk Producers** – Amish and Mennonite farmers in states like Delaware and Pennsylvania operate direct-to-consumer raw milk operations. Their strategy is built on community trust, on-farm sales, and activism for legal raw milk access. They often produce raw milk cheese under the 60-day aging rule.

5. Market Trends

1. ORGANIC BOOM

ORGANIC BOOM — Organic pasteurized milk is the fastest-growing mainstream sub-segment, projected to reach USD 12.5 billion by 2036. Consumers associate organic with purity, even when pasteurized. Brands like Organic Valley are doubling down on pasture-raised claims.

2. REGULATORY TIGHTENING

REGULATORY TIGHTENING — U.S. FDA and state authorities are increasing raw milk inspections and labeling requirements. In 2025, Delaware introduced stricter farm-to-table traceability rules, impacting small-scale raw milk sellers. Compliance costs are rising.

3. FUNCTIONAL DAIRY

FUNCTIONAL DAIRY — Both raw and pasteurized milk are being marketed with functional benefits. Raw milk advocates claim enzyme preservation; pasteurized brands add vitamins and probiotics. Synopticcircle’s analysis notes that functional dairy innovations are a key driver of the 7.3% CAGR.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two opportunities stand out: First, the raw milk market can expand by partnering with pasteurized cheese makers for aged raw milk products—bypassing fluid milk bans. Second, organic pasteurized milk producers can capture market share by investing in transparent cold-chain logistics that mimic raw milk freshness. The primary risk is inconsistent regulation across states and countries, which creates supply chain friction and legal liability for cross-border dairy sourcing. B2B buyers should prioritize suppliers with robust traceability and compliance protocols to navigate this divided market through 2026 and beyond.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Raw Milk vs Pasteurized Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-27. All market figures are estimates and may vary from actual results.