Table of Contents

The global Sugar & Sweeteners Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

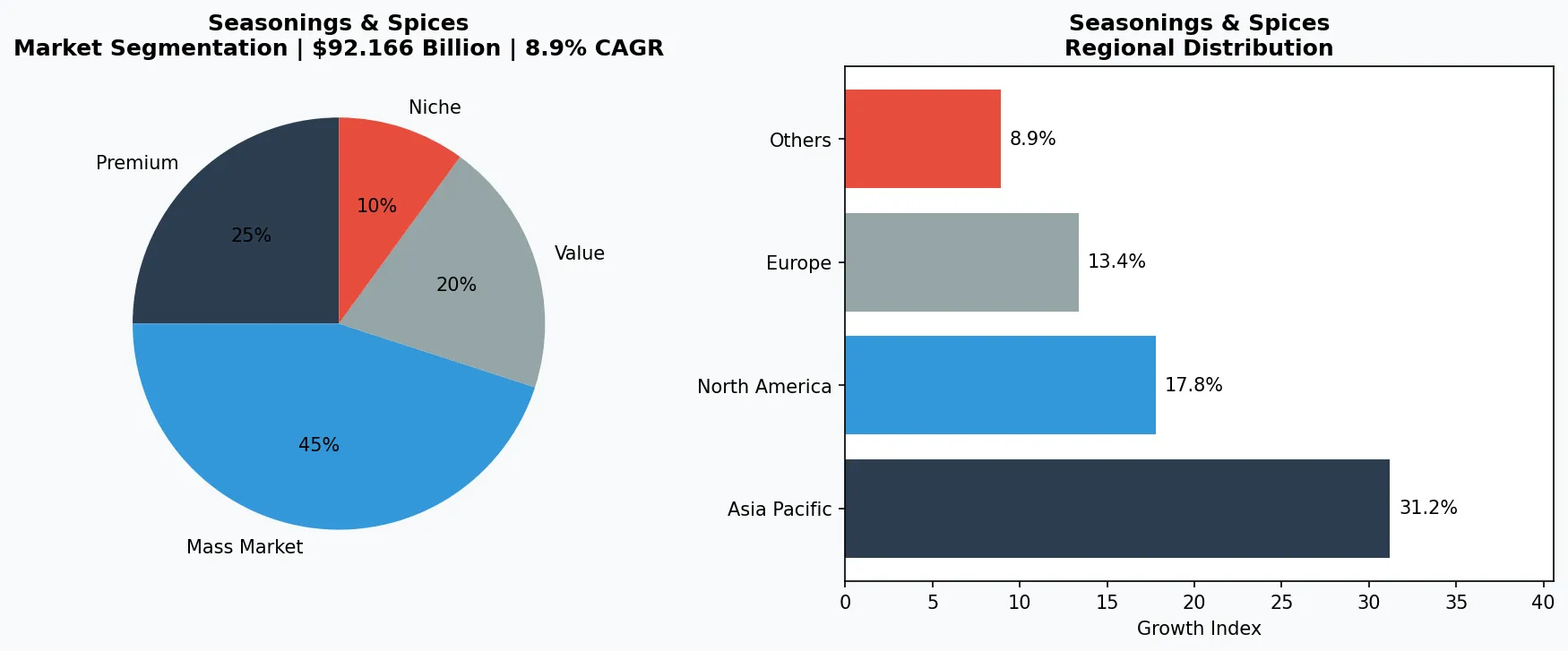

What if the most critical ingredient in your seasoning portfolio isn't a spice at all, but a sweetener? Within the vast Seasonings & Spices industry, the Sugar & Sweeteners segment operates as a distinct and colossal market force, fundamentally shaping flavor profiles from savory sauces to complex spice blends. It transcends the simple granulated white sugar of home kitchens, encompassing a sophisticated spectrum of natural and synthetic agents that deliver sweetness, texture, browning, and preservation. This segment's distinctiveness lies in its dual role: it is both a foundational commodity and a high-growth innovation hub, driven by health trends and regulatory shifts. The global sugars and sweeteners market, valued at $92.166 billion in 2021, is projected to reach a staggering $128.2 billion by the end of 2025, underscoring its massive scale and continued expansion. This growth is not uniform; it is being aggressively pulled in two directions by traditional bulk sugars and the rapidly evolving sugar substitutes sector, creating a dynamic and complex landscape for B2B decision-makers.

Industry Scope & Characteristics

Broad Product Portfolio

Products span cane sugar, brown sugar, rock sugar, powdered sugar, stevia, erythritol, coconut sugar, honey, maple syrup, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Industry application and market overview for Sugar & Sweeteners Guide.

2. Market Analysis

The market data reveals a story of robust, bifurcated growth. The total global sugars and sweeteners market is on a clear upward trajectory, set to hit $128.2 billion by 2025. However, the most explosive action is concentrated in the alternatives space. The sugar substitutes market alone is projected to surge from $24.8 billion in 2025 to new heights, with another authoritative projection valuing it at USD 26.88 billion in 2026 and forecasting an 8.9% CAGR to reach USD 37.86 billion by 2030. Similarly, the broader Sweetening Agent market is anticipated to grow at a CAGR of 9.1% from 2026 to 2033. This growth is propelled by three key drivers. First, relentless consumer demand for reduced-sugar and 'healthier' products across all food categories, from beverages to condiments like ketchup and oyster sauce. Second, government policies and sugar taxes, such as those influencing the USDA's 2024/25 and 2025/26 projections for the U.S. and Mexico, are forcing large-scale recipe reformulation. Third, continuous ingredient innovation has improved the taste and functionality of substitutes, making them viable for a wider range of industrial applications beyond diet sodas.

Market segmentation and regional distribution for Seasonings & Spices - Sugar & Sweeteners Guide.

3. Product Categories

The product landscape is usefully divided into three core categories. First, **Traditional Caloric Sweeteners** remain the volume giants, including cane/beet sugar (sucrose), high-fructose corn syrup (HFCS), and globally prevalent options like palm sugar and jaggery. These are staples in bulk seasoning production for soy sauce, hoisin, and bouillon for their cost-effective sweetness and functional properties like browning and preservation. Second, **Natural High-Intensity Sweeteners** have gained significant traction, led by stevia (Reb M and Reb D isolates for cleaner taste) and monk fruit extract. These plant-derived, zero-calorie options cater to the 'clean label' movement and are increasingly blended to mask off-notes. Third, **Synthetic and Sugar Alcohol Sweeteners** include established players like sucralose, aspartame, and acesulfame potassium, alongside sugar alcohols like erythritol and allulose, which offer low glycemic impact and bulking properties similar to sugar. Each category serves distinct B2B needs, from cost and functionality to marketing claims.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The competitive field is dominated by diversified agri-food giants and specialized ingredient innovators. **Ingredion** exemplifies a strategic pivot, leveraging its core starch business to develop a comprehensive portfolio of stevia-based sweeteners and texturants, helping clients reduce sugar without compromising mouthfeel. **Tate & Lyle**, a historical sugar titan, has radically transformed into a leading solutions provider for sugar reduction and fiber fortification, with its allulose product gaining significant FDA regulatory traction. **Cargill** operates across the entire spectrum, from global sugar trading and sourcing to its proprietary EverSweet stevia (developed via fermentation with DSM) and Zerose erythritol, offering customers a one-stop-shop for sweetening solutions. **PureCircle (now part of Ingredion)** was a pioneer in driving the commercial scalability and taste improvement of high-purity stevia extracts, fundamentally altering the economics and acceptance of the natural sweetener.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the seasonings & spices space.

5. Market Trends & Innovations

1. Sustainability & Eco-Friendly Innovation

Sustainability has become a core competitive priority. Companies like Cargill and Tate & Lyle are investing in eco-friendly materials, carbon-neutral production, and circular economy initiatives to meet growing consumer demand for responsible products.

2. Digital Transformation & E-Commerce Growth

The shift to digital sales channels continues to accelerate. Südzucker and Associated British Foods are leveraging data analytics, AI-driven personalization, and omnichannel strategies to enhance customer engagement and streamline distribution.

3. Premiumization & Product Innovation

Rising consumer expectations are driving premiumization across the market. Cosan has introduced high-end product lines, while Wilmar International focuses on innovative features and superior quality to capture value-conscious yet quality-seeking customers.

4. Health, Wellness & Functional Benefits

Health-oriented consumer preferences are reshaping product development. Tereos and Nordzucker are pioneering functional products with demonstrable benefits, commanding premium pricing and driving category expansion.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities are paramount for 2026 and beyond. First, the integration of sweetener systems into savory and umami-forward applications presents a white space. Developing blends that enhance the savory depth of soy sauce, oyster sauce, or chili crisps without overt sweetness can create distinct product advantages. Second, the regulatory greenlight for novel ingredients like allulose in more regions opens a window for first-movers to establish formulations and claims around 'sugar-like' functionality with minimal calories.

The concrete risk remains price volatility and supply chain fragility in the bulk sugar market, heavily influenced by weather, policy (as seen in USDA's shifting projections), and geopolitical factors. A sudden price spike in traditional sugar could simultaneously strain margins for dependent products and accelerate the switch to alternatives, but not before causing significant short-term disruption for unprepared manufacturers.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Sugar & Sweeteners Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-21. All market figures are estimates and may vary from actual results.