-450x250h.webp)

-150x150h.webp)

Whey Protein Market Surges to $9.1B in 2025: Forward Contracts Lock Up 2026 Supply

Table of Contents

The global Whey Protein Products sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The global whey protein products market is projected to grow from $9.1 billion in 2025 to $12.9 billion by the end of 2030, at a compound annual growth rate of 7.2%. That is no small whey. This surge is not just about gym-goers chugging shakes; it reflects a structural shift in how consumers and food manufacturers perceive protein. Whey, once a byproduct of cheese making, has become a premium ingredient for sports nutrition, functional foods, and meal replacements. What makes whey protein distinct within the broader Dairy & Egg Products industry is its dual role as a commodity ingredient and a high-margin branded product. Unlike milk or butter, whey is processed into isolates, concentrates, and hydrolysates that command significant price premiums. The market's acceleration is underpinned by rising health awareness, a global push toward high-protein diets, and increasing adoption among older adults looking to maintain muscle mass. Yet the supply side tells a more nuanced story: major manufacturers have sold forward contracts well into 2026, leaving little to no spot-market inventory for new or growing customers. This tightness signals that the market is not just growing—it is restructuring. For B2B buyers and suppliers, understanding this dynamic is critical for securing stable sourcing relationships. The whey protein segment is no longer a niche add-on; it is a cornerstone of modern nutrition strategy.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Whey Protein Products, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

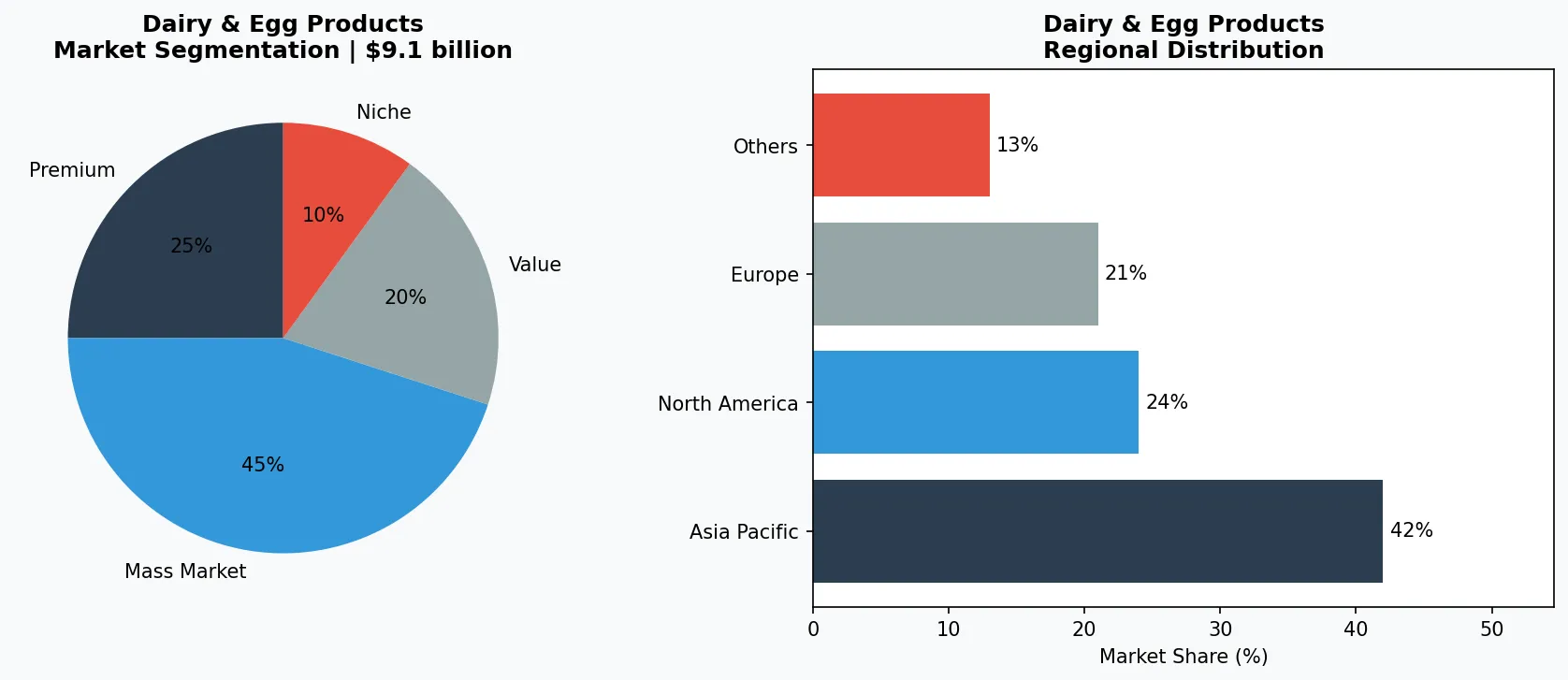

Key market segments and growth drivers in the Whey Protein Products sector.

2. Market Analysis

The whey protein products market reached a valuation of $6.15 billion in 2025 and is anticipated to expand at a CAGR of 13.63% during the forecast period. While different methodologies yield slightly different base figures—one research firm pegs 2025 at $9.1 billion—the consensus is clear: double-digit growth is locked in. Three key drivers fuel this expansion. First, the sports nutrition boom shows no signs of slowing. Demand for whey isolate and hydrolyzed whey has grown by over 15% year-over-year in key markets like North America and Asia-Pacific. Second, the trend toward high-protein diets has moved beyond athletes. Mainstream consumers now seek protein-fortified yogurt, ready-to-drink shakes, and protein bars. This opens a massive addressable market in everyday food and beverage categories. Third, the clean-label movement has forced manufacturers to strip out artificial sweeteners, fillers, and GMOs. Clean-label whey protein products now command a 20–30% price premium over conventional equivalents, driving value growth even when volume growth moderates. The Asia-Pacific region is expected to be the fastest-growing market, fueled by rising disposable incomes in China and India and a growing fitness culture. However, supply constraints pose a real challenge. With forward contracts covering production through late 2026, spot buyers face inflated prices and limited availability. For B2B procurement teams, this means early negotiation and multi-year agreements are becoming table stakes.

Market segmentation and regional distribution analysis for Whey Protein Products.

3. Product Categories

Whey protein products fall into three primary categories, each serving distinct end-use applications. Whey Protein Concentrate (WPC) is the most widely used form, typically containing 70–80% protein. It retains more of the fat and lactose found in milk, giving it a creamy mouthfeel ideal for smoothies, baked goods, and snack bars. Major dairy processors produce WPC in varying protein levels to meet diverse customer needs. Whey Protein Isolate (WPI) undergoes further processing to remove nearly all fat and lactose, yielding a protein content of 90% or higher. WPI is the go-to choice for serious athletes and medical nutrition products where purity and rapid absorption are critical. It is commonly found in premium sports shakes and clear protein waters. Whey Protein Hydrolysate (WPH) is partially broken down (hydrolyzed) for faster digestion. Used in clinical nutrition and high-end recovery supplements, WPH is more expensive but offers a sensory advantage—it mixes easily without clumping. Within each category, product innovation is accelerating. For example, some manufacturers now offer grass-fed whey isolates that leverage clean-label claims, while others produce microfiltered concentrates that retain more bioactive compounds. For B2B buyers, the choice of format directly impacts cost, application, and consumer appeal.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The whey protein market is dominated by a handful of global dairy giants and specialized ingredient suppliers. Major manufacturers have sold forward contracts well into 2026, a move that signals both confidence in sustained demand and a strategic effort to lock in pricing. One leading global dairy cooperative, based in the United States, has invested heavily in membrane filtration technology to increase yields of high-purity isolates. Its strategy centers on supplying large-scale sports nutrition brands with traceable, non-GMO whey ingredients. A second major player, headquartered in Europe, has differentiated itself through organic and grass-fed whey protein lines. By targeting premium B2B customers in the clean-label segment, it captures higher margins and builds long-term loyalty among protein bar and meal replacement manufacturers. A third key competitor focuses exclusively on hydrolyzed whey for clinical and pediatric nutrition. Its products are used in hospital feeding programs and specialized infant formulas—a niche that insulates it from commodity price cycles. All three players face a common challenge: raw milk supply volatility. With dairy farmers facing feed costs and environmental regulations, securing consistent whey feedstock requires multi-year contracts with milk producers. The forward-contract strategy is a direct response; it de-risks production and ensures that buyers willing to commit early can secure supply. For new entrants or smaller brands, the window to obtain spot-market whey protein has narrowed considerably.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the dairy & egg products space.

5. Market Trends

1. CLEAN LABEL AND ORGANIC SHIFT

CLEAN LABEL AND ORGANIC SHIFT — Consumers are increasingly seeking whey protein that contains no artificial flavors, colors, or preservatives. This trend has accelerated since 2024, with clean-label whey products growing at twice the rate of conventional ones. Major global dairy processors have responded by launching organic whey isolates and concentrates that are Non-GMO Project Verified. The trend matters because it elevates the entire category: clean-label certification commands a 25–30% price premium, boosting revenue even if volume growth slows.

2. SUPPLY CONTRACTION AND FORWARD BOOKING

SUPPLY CONTRACTION AND FORWARD BOOKING — With production capacity nearly fully committed through 2026, spot-market availability is at an all-time low. This is not a short-term hiccup but a structural shift. Manufacturers are prioritizing long-term relationships with large buyers, effectively squeezing smaller brands and new entrants. For B2B buyers, this trend means procurement must start 12–18 months in advance, and price negotiation leverage has shifted firmly to suppliers.

3. FUNCTIONAL AND BEYOND-SPORTS APPLICATIONS

FUNCTIONAL AND BEYOND-SPORTS APPLICATIONS — Whey protein is no longer just for post-workout shakes. It is now used in high-protein water, coffee creamers, and even savory snacks. The functional food sector is expected to absorb over 40% of new whey protein supply by 2028. Companies like those in infant formula and medical nutrition are reformulating products to include whey hydrolysates for easier digestion. This diversification reduces market risk for producers and opens new channels for B2B suppliers.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities stand out for B2B buyers and manufacturers. First, investing in contracts for grass-fed or organic whey isolates now can lock in premium pricing power as clean-label demand continues. Second, regional processors in Asia-Pacific that partner with local dairy co-ops can bypass the tight Western supply chain and tap into the fastest-growing consumption region. However, one concrete risk looms: if protein demand softens due to an economic downturn—or if alternative proteins (plant-based or precision fermentation) gain meaningful share—the forward-contract commitments could leave buyers over-allocated and paying above market prices. Prudent hedging and flexible volume commitments will be essential for navigating 2026 and beyond.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Whey Protein Products Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-27. All market figures are estimates and may vary from actual results.