Table of Contents

The global Cheese Category Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Every cheese block, shred, and slice on a retail shelf is now part of a strategic pivot: the global cheese industry is abandoning passive table cheese in favor of melt-driven, repeatable usage formats that dominate both foodservice and retail. According to McKinsey’s eighth annual dairy survey, rising demand continues to collide with cost and margin pressures in 2026, forcing producers to rethink their category playbooks. This cheese category guide cuts through the noise to show B2B buyers how to classify, source, and leverage the segments that actually grow.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Cheese Category Guide, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

What makes this sub-topic distinctive within the broader Dairy & Egg Products industry is its dual nature: cheese remains a staple commodity, yet it is rapidly fragmenting into functional, premium, and protein-enhanced niches. The Dairy Farmers of America identify sustainability, wellness, texture, and protein as the four pillars reshaping product development. Unlike milk or butter, cheese carries a longer shelf life and higher value per pound, making it a strategic profit center for suppliers who can align with these trends.

Online sales of cheese have surged, with premium and craft varieties leading the charge. Import and export activity has intensified as global buyers chase authentic European Appellation d’Origine Protégée (AOP) cheeses alongside innovative American cheddars. The category is no longer simply about buying blocks and aging them; it is about engineering melt performance, enhancing protein content, and telling a sustainability story that fits a foodservice menu or a retail private-label program.

For B2B decision-makers, understanding the cheese category means knowing which formats deliver repeat orders, which regions offer the best price-quality balance, and how consumer wellness trends translate into industrial formulation. This guide provides the framework to navigate a market projected to grow at a compound annual rate of 10.4% through 2033, with data drawn from leading industry analysts and real-world market findings.

Key market segments and growth drivers in the Cheese Category Guide sector.

2. Market Analysis

The natural cheese market is on a trajectory that few dairy categories can match. Industry analysis projects a compound annual growth rate of 10.4% from 2026 to 2033, driven by relentless demand from foodservice operators and expanding e-commerce channels. McKinsey’s 2026 dairy survey confirms that consumers are willing to pay more for cheese they perceive as authentic, high-protein, and sustainably produced, even as they trade down in other grocery categories.

Two mega-trends fuel this growth. First, melt-driven meals – pizza, quesadillas, burgers, mac and cheese, and hot sandwiches – generate massive repeat volume for cheese processors. Foodservice alone accounts for over 40% of global cheese consumption, and operators are reformulating menus to maximize the visual and functional appeal of melted cheese. Second, the premium and craft cheese segment has seen double-digit online sales growth, as small-batch producers bypass traditional retail to sell directly to chefs and consumers. The U.S. craft cheese market alone grew by 18% in 2024, according to trade data.

Import and export flows also reflect this dynamism. European Union cheese exports to Asia rose steadily in 2025, led by Parmigiano-Reggiano and Gouda, while U.S. mozzarella and cheddar volumes climbed in Latin American and Middle Eastern markets. However, cost pressures are not easing: raw milk prices remain volatile, and logistics costs have compressed margins for mid-tier producers. The premium end absorbs these costs better, further encouraging the shift toward higher-value formats.

For B2B buyers, the message is clear: the growth lies in form factors that enable quick service, portion control, and shelf-stable distribution. Commodity blocks will not disappear, but the margin expansion is happening in value-added shreds, slices, and specialty cuts that command a premium per pound.

Market segmentation and regional distribution analysis for Cheese Category Guide.

3. Product Categories

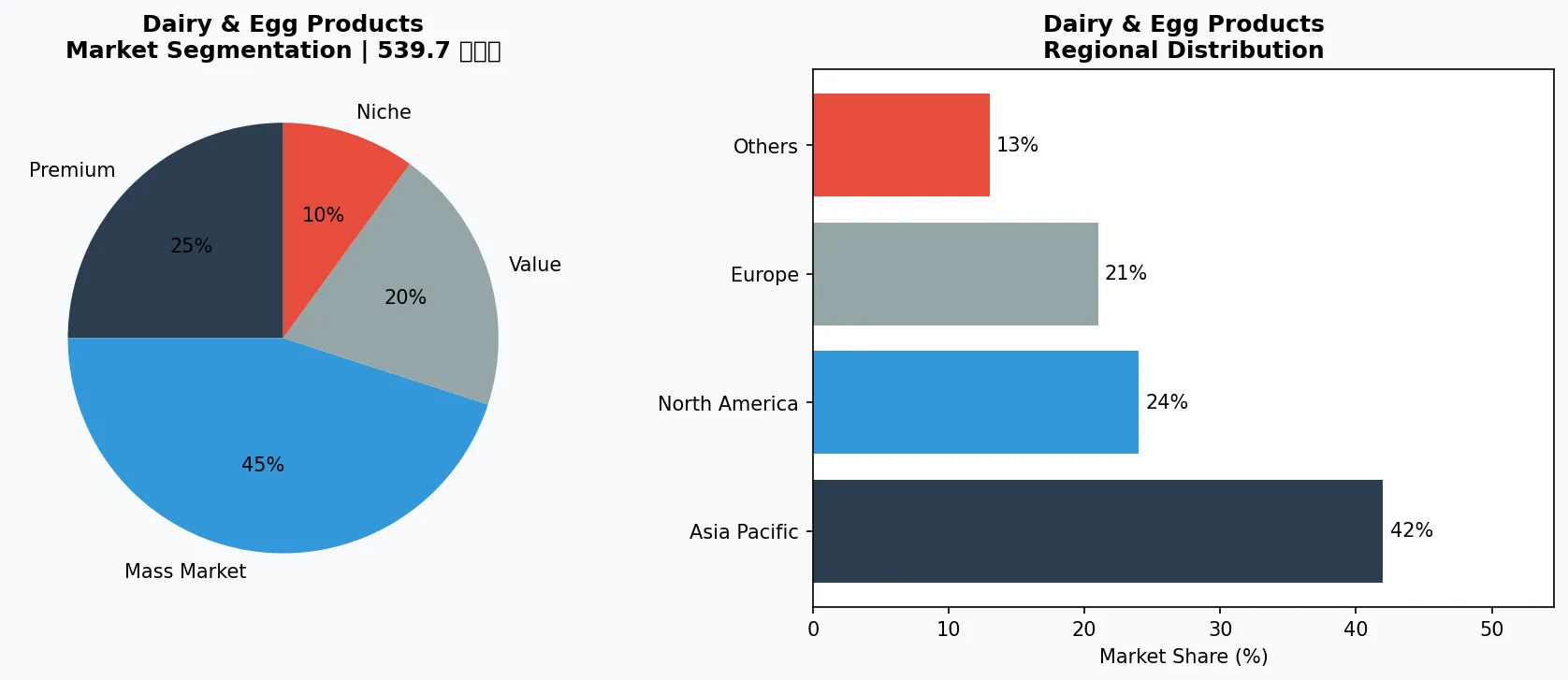

The cheese category can be organized into four distinct product types, each with its own sourcing logic and margin profile.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

**Fresh Cheese** – Mozzarella, ricotta, feta, and cream cheese. Fresh cheeses are the workhorses of melt-driven meals. Mozzarella, in particular, is the backbone of the pizza industry, which alone consumes over 35% of global cheese output. These products require fast logistics and strict cold chain compliance, making supplier reliability the top procurement criterion. Tastewise data shows that mentions of 'fresh mozzarella' in menus have risen 22% year-over-year as chefs seek authentic, high-moisture options.

**Aged Cheese** – Cheddar, Gouda, Parmesan, and Gruyère. Aged cheeses offer higher unit value and longer shelf life, making them ideal for export and retail private-label programs. Cheddar alone represents nearly 30% of U.S. cheese production. The trend here is toward shorter aging cycles (6–12 months) that still deliver flavor depth but reduce inventory carrying costs. Dairy Farmers of America has invested in accelerated aging technologies to meet demand for robust taste without tying up capital for years.

**Soft-Ripened & Blue Cheese** – Brie, Camembert, Roquefort, and Gorgonzola. These are premium products that command high margins but require specialized mold cultures and careful ripening facilities. Online sales of soft-ripened cheese surged 30% in 2025, driven by at-home charcuterie trends. B2B buyers should look for suppliers with certified mold-aging rooms and blockchain traceability to prove origin claims.

**Processed Cheese & Cheese Spreads** – Slices, shreds, sauces, and dips. Processed cheese offers precise melt characteristics and extended shelf stability, crucial for foodservice chains that need consistent performance. The largest processors are reformulating to reduce sodium and add protein, responding to wellness trends without sacrificing meltability. This sub-category is the most commoditized, but also the most scalable for volume buyers.

4. Leading Players

Three key players shape the cheese category: Dairy Farmers of America (DFA), McKinsey & Company, and the data intelligence firm Tastewise. Each influences the market in a distinct way.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the dairy & egg products space.

**Dairy Farmers of America** – As the largest dairy cooperative in the United States, DFA controls a significant share of milk supply and cheese production. The cooperative has publicly committed to aligning its product portfolio with the four trends it identified: sustainability, wellness, texture, and protein. DFA is investing in reduced-fat and high-protein cheese lines, as well as methane-reduction farming practices that appeal to ESG-focused buyers. For B2B partners, DFA offers scale and traceability, but its cooperative structure can mean less flexibility in custom formulations compared to private processors.

**McKinsey & Company** – While not a cheese producer, McKinsey’s annual dairy survey has become a de facto benchmark for the industry. The 2026 survey highlights that 68% of dairy executives expect cost pressures to persist, pushing them to invest in automation and premium product lines. Buyers use McKinsey’s data to negotiate contract terms and forecast price swings. The consultancy’s insights on consumer willingness to pay for sustainability claims directly influence how cheese suppliers market their products to retailers.

**Tastewise** – This AI-powered food trend platform tracks billions of food and beverage data points, including menu mentions, social media conversations, and recipe usage. Tastewise reports that melt-driven cheese applications (pizza, grilled cheese, cheese dips) are growing 3x faster than non-melt applications. B2B buyers can leverage Tastewise’s analytics to identify which cheese formats are gaining traction in specific regions or restaurant segments, reducing the risk of sourcing the wrong product. The platform’s data also helps suppliers justify premium pricing by linking flavor trends to consumer demand.

These three players – a cooperative, a consultancy, and a tech platform – collectively shape the category’s direction. B2B decision-makers should monitor all three for signals on pricing, demand shifts, and innovation opportunities.

5. Market Trends

1. MELT-DRIVEN MEALS

MELT-DRIVEN MEALS — The single strongest demand driver is cheese used in melting applications – pizza, burgers, sandwiches, and pasta dishes. According to Tastewise, melt-focused menu items account for 60% of all cheese mentions in foodservice. This trend matters because it creates repeatable, high-volume orders for processors, and it rewards suppliers who can engineer consistent stretch, browning, and oil-release properties. Example: Domino's Pizza, a major buyer, sources specific mozzarella blends for its ovens.

2. SUSTAINABILITY & WELLNESS

SUSTAINABILITY & WELLNESS — Dairy Farmers of America flags sustainability and wellness as non-negotiable for 2026 buyers. Consumers want cheese from cows raised on pasture, with lower carbon footprints and cleaner labels. At the same time, wellness is driving demand for reduced-sodium, reduced-fat, and high-protein cheese. DFA is rolling out a line of grass-fed cheddar with a verified carbon-neutral certification, targeting retailer private labels.

3. PREMIUM & CRAFT SURGE

PREMIUM & CRAFT SURGE — Online sales of craft cheese grew over 25% in 2025, and import data from the EU shows a 15% increase in AOP cheese exports to the U.S. Small-batch producers are using DTC channels to reach chefs and home cooks willing to pay $20+ per pound. This trend matters because it opens new margin opportunities for B2B distributors that can handle small-lot, high-touch logistics. Example: Murray's Cheese, a New York-based retailer, now offers curated wholesale boxes for restaurants.

4. PROTEIN ENRICHMENT

PROTEIN ENRICHMENT — The protein trend, driven by fitness and health-conscious consumers, is pushing cheese processors to add whey protein or other isolates to create higher-protein cottage cheese, string cheese, and cheese-based snacks. This is a growth area beyond traditional cheese formats, with companies like Good Culture experimenting with 14g-protein cottage cheese cups.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities stand out for B2B buyers in the cheese category. First, invest in high-protein and functional cheese products aimed at the wellness segment. With 68% of dairy executives expecting cost pressures, premium functional lines offer higher per-unit margins and can be marketed at a 30-40% price premium over standard cheese. Second, build direct online channels for craft and imported cheeses. The e-commerce surge shows no signs of abating, and buyers who can aggregate small producers into curated wholesale catalogs will capture the loyalty of chefs and specialty retailers.

The primary risk remains the cost-margin squeeze identified by McKinsey’s 2026 survey. Raw milk prices are volatile, and labor costs in processing plants are rising faster than automation can offset. If commodity cheese prices spike, buyers may face inventory write-downs or be forced to reformulate. Mitigation strategies include locking in long-term contracts with cooperatives like DFA, and diversifying sourcing between domestic and imported supply to buffer against regional shocks.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Cheese Category Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-26. All market figures are estimates and may vary from actual results.