Table of Contents

The global Coffee Market Analysis sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Global coffee consumption is on a collision course with supply constraints — yet the market is projected to surge from $145.23 billion in 2025 to $227.18 billion by 2032, a CAGR of 6.6%. That growth is not just a volume story; it reflects a fundamental shift in how coffee is produced, traded, and consumed. The Beverages & Mixes industry, spanning soda, fruit juice, milk tea, and energy drinks, sees coffee as its most dynamic segment, driven by premiumization, convenience, and evolving consumer rituals. What makes coffee market analysis distinctive is the interplay of commodity volatility, geopolitical supply risks, and rapidly fragmenting consumer preferences. Unlike soft drinks with stable inputs, coffee prices swing on weather events in Brazil, inventory wars among roasters, and logistics bottlenecks from origin to cup. The National Coffee Data Trends (NCDT) report — the longest-running U.S. study on coffee consumption — is now essential reading for procurement managers and brand strategists. Its Spring 2026 edition reveals that 68% of American adults consumed coffee in the past day, a record high that underscores shifting habits even as supply tightens. Understanding these dynamics is critical for businesses that source, brand, or distribute coffee products globally.

Industry Scope & Characteristics

Broad Product Portfolio

Products span arabica coffee, robusta coffee, instant coffee, espresso beans, cold brew concentrate, coffee pods, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Industry application and market overview for Coffee Market Analysis.

2. Market Analysis

The global coffee market’s trajectory is unmistakable: from $145.23 billion in 2025 to an estimated $227.18 billion by 2032, according to the latest industry forecasts. That 6.6% compound annual growth rate is fueled by three powerful drivers. First, the expansion of café culture in Asia-Pacific and Latin America, where rising disposable incomes are converting tea drinkers into daily coffee consumers. Second, the product innovation wave in ready-to-drink (RTD) and cold brew formats, which command higher margins and attract younger demographics. Third, the institutional demand from offices, hotels, and quick-service restaurants that continues to recover post-pandemic. On the supply side, the updated outlook points to a more comfortable global balance in 2026, with production forecast to rise to 182.5 million bags — up from 175 million in 2025 — as major producers like Brazil and Vietnam rebound from weather disruptions. However, this surplus remains fragile: stock-to-use ratios are at decade lows, and any unexpected frost or drought could tighten availability overnight. The NCDT Spring 2026 data confirms that U.S. consumption alone grew 3.2% year-over-year, outpacing GDP growth. For B2B buyers, this means locking in contracts early and diversifying origin sources is no longer optional — it's survival.

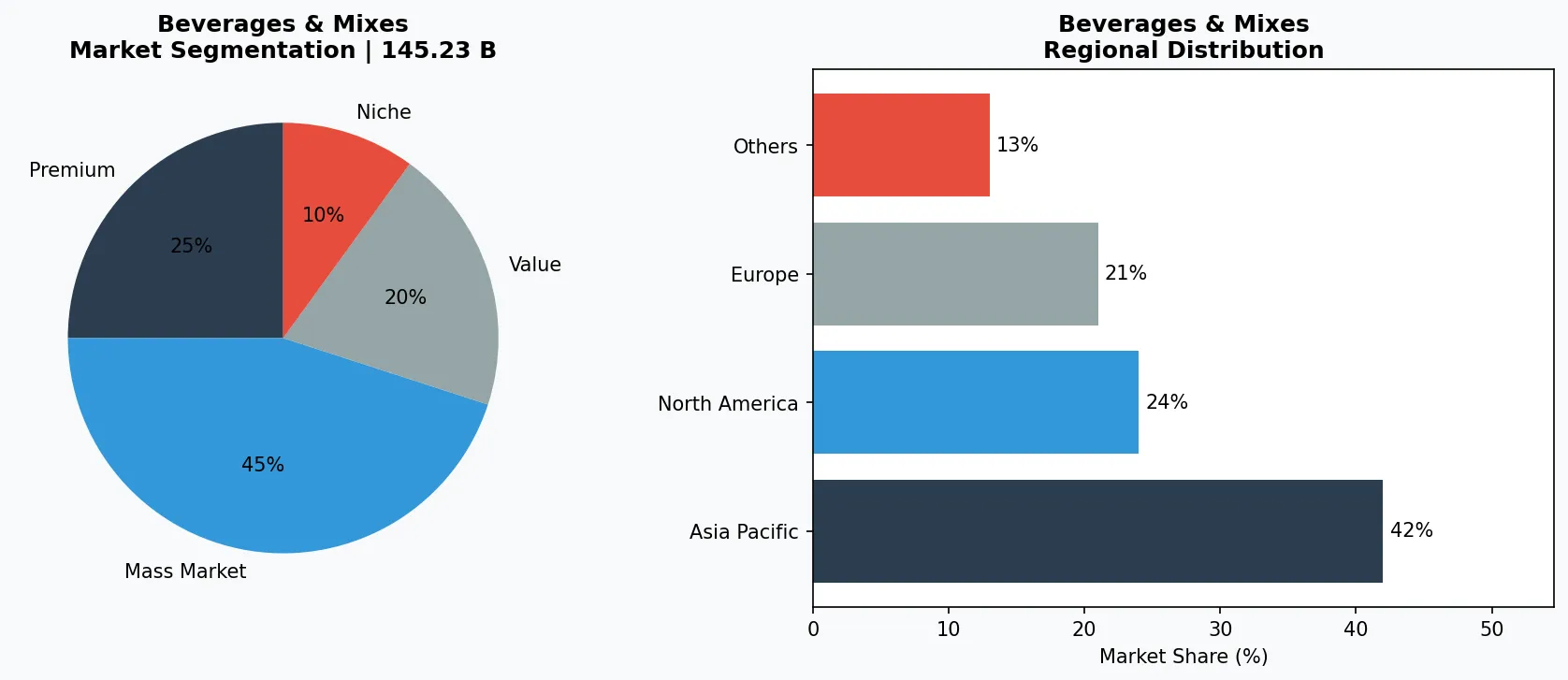

Market segmentation and regional distribution for Beverages & Mixes - Coffee Market Analysis.

3. Product Categories

The coffee market segments into four distinct product types, each with its own growth curve and consumer base. Whole Bean & Ground Coffee remains the largest category by value, driven by the at-home espresso movement and single-origin demand. Premium roasters now offer traceable beans with QR codes, appealing to the transparency-conscious buyer. Instant Coffee, long considered a commodity, is receiving a premium makeover with freeze-dried specialty blends and single-serve sticks, especially popular in Asia. Nestlé’s Nescafé brand has introduced high-altitude single-origin instant lines, targeting the office and travel segment. Ready-to-Drink (RTD) Coffee is the fastest-growing category, expanding at over 9% annually as convenience wins over quality purists. Cold brew, in particular, has transcended seasonal trends and is now a year-round staple, with major bottlers launching nitrogen-infused variants. Finally, Specialty & Single-Origin coffee now accounts for nearly 40% of U.S. retail coffee sales, according to NCDT data. These beans command a 30-50% price premium over conventional, rewarding farmers who invest in certification. For beverage formulators and private-label buyers, sourcing certified sustainable coffee is becoming a baseline requirement, not a differentiator.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The competitive landscape is dominated by three clusters: global roasters, specialty chains, and emerging origin-based brands. Nestlé, through its Nescafé and Nespresso divisions, holds the largest market share in instant and portioned coffee, leveraging its R&D muscle to push into RTD and home-brewing systems. The company’s 2025 investment in a carbon-neutral supply chain across Colombia and Ethiopia signals a long-term bet on sustainability as a brand asset. JDE Peet’s, owner of Jacobs, Douwe Egberts, and Peet’s Coffee, focuses on building vertical integration from farm to cup. Its recent acquisition of a pan-African sourcing platform gives it direct control over over 50,000 metric tons of green coffee annually, insulating it from spot-market volatility. Starbucks remains the iconic retailer and branded consumer packaged goods player, with its at-home coffee sales through grocery channels now rivaling its café revenue. The chain’s push into cold brew concentrate and creamers shows how it is leveraging its brand equity to capture the at-home premium segment. Finally, smaller origin-focused players like Counter Culture Coffee and Intelligentsia have carved out a B2B niche, supplying high-end restaurants and corporate offices with traceable, direct-trade beans. For procurement managers on Verity Rank, evaluating these players’ supply chain robustness and certification credentials is critical when selecting verified suppliers.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the beverages & mixes space.

5. Market Trends

1. 1. SUSTAINABILITY & ETHICAL

1. SUSTAINABILITY & ETHICAL SOURCING

2. SUSTAINABILITY & ETHICAL SOURCING — What it is: A shift

SUSTAINABILITY & ETHICAL SOURCING — What it is: A shift toward deforestation-free supply chains, carbon-neutral roasting, and fair-trade premiums. Why it matters: New EU regulations require importers to prove their coffee hasn’t contributed to forest loss by 2026. Example: Nestlé has committed to 100% responsibly sourced coffee by 2026, mapping over 100,000 farms. COLD BREW & RTD SURGE | What it is: Ready-to-drink cold brew sales growing at 9%+ annually, outpacing hot coffee. Why it matters: Cold brew allows higher margins per ounce and appeals to younger, on-the-go consumers. Example: Starbucks’ line of bottled cold brew concentrates saw a 22% sales increase in 2025. DIGITALIZATION OF THE SUPPLY CHAIN | What it is: Blockchain traceability and AI-driven demand forecasting tools for coffee traders and roasters. Why it matters: Real-time tracking reduces risk of adulteration and helps buyers verify origin claims. Example: The specialty roaster Counter Culture Coffee now offers a public blockchain ledger for every lot it sources. PREMIUMIZATION AT HOME | What it is: Consumers investing in high-end brewers, specialty beans, and dairy alternatives. Why it matters: This trend drives volume growth in whole-bean and single-serve segments. Example: Sales of espresso machines in the U.S. rose 18% in 2025, per NCDT data.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities stand out for 2026-2027. First, the specialty coffee market in India and Southeast Asia is underpenetrated, with per capita consumption below 0.5 kg annually. Early entry by private-label roasters or distributors into these markets, especially via e-commerce, could capture first-mover advantage. Second, the premiumization of at-home brewing equipment creates demand for ultra-fresh, single-origin beans delivered on subscription models — a high-margin, repeat-purchase channel that B2B suppliers can support via white-label packaging. The primary risk remains climate volatility in the Arabica heartland of Brazil and Colombia. A severe drought or frost in 2027 could push prices above $3 per pound, compressing margins for roasters that lack long-term contracts. Buyers should prioritize suppliers with diversified sourcing portfolios and multi-year forward agreements to hedge against price shocks. Verity Rank’s supplier verification tools can help identify these resilient partners.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Coffee Market Analysis Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-24. All market figures are estimates and may vary from actual results.