-450x250h.webp)

-150x150h.webp)

Tea Beverages Hit $64 Billion by 2034: The New Rules for Operators

Table of Contents

The global Tea Beverage Category Report sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2034, the global tea beverage market is projected to exceed $64 billion—a 60% jump from its 2026 valuation of $40.2 billion. That explosive trajectory is forcing operators to rethink everything from ingredient sourcing to menu positioning within the broader Beverages & Liquid Supplements segment.

Industry Scope & Characteristics

Broad Product Portfolio

Products span green tea, oolong tea, jasmine tea, black tea, milk tea, pu-erh tea, barley tea, diet tea beverages, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

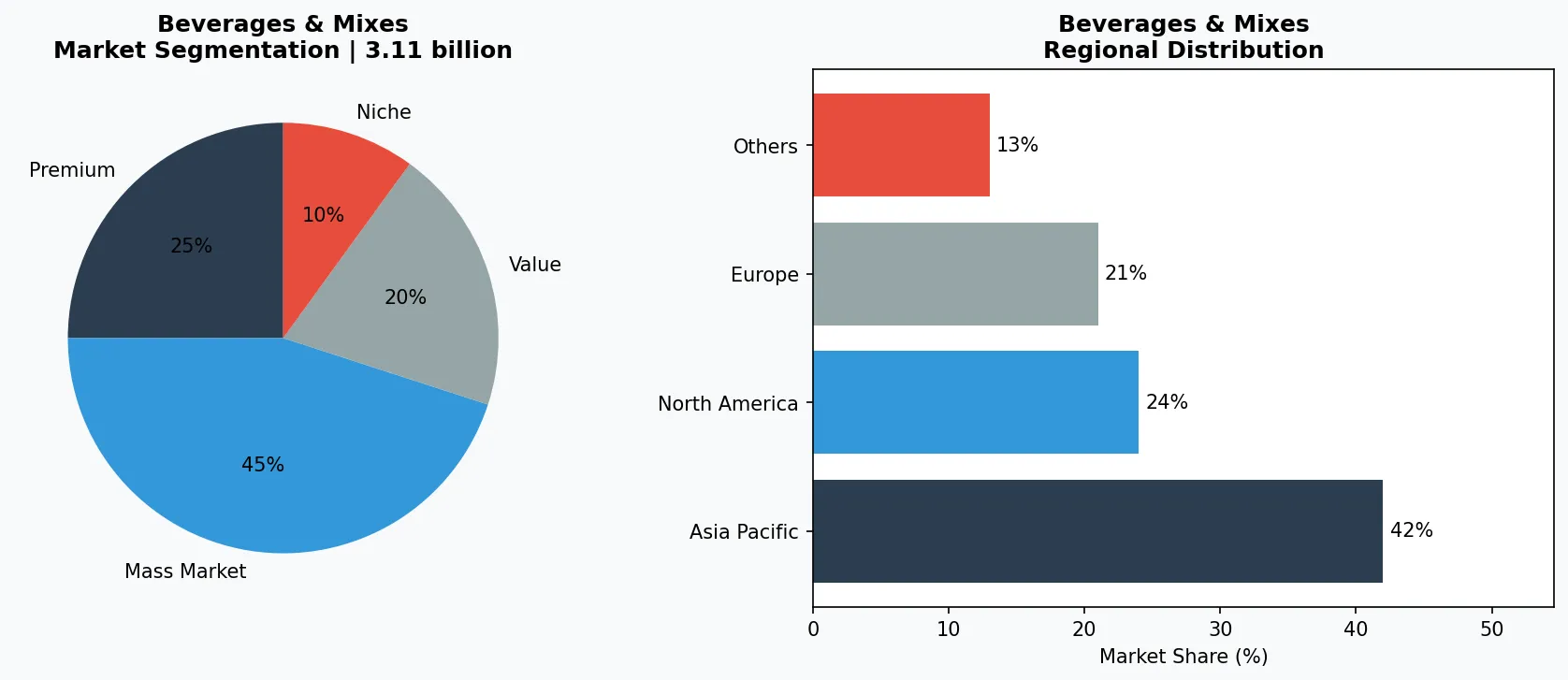

The tea category is no longer a sleepy aisle of bagged black tea. It now intersects with wellness, energy, and even coffee culture. Protein coffee, loaded teas, and premium lattes are blurring the lines between traditional hot drinks and functional beverages. At the same time, the U.S. tea market alone sits at $3.11 billion in 2025, with steady growth to $3.78 billion by 2032. This is a category that demands attention.

What makes the tea beverage category distinctive is its dual identity: it is both a comfort staple and a canvas for innovation. Operators who can navigate organic certification, matcha diversification, and caffeine-free alternatives will capture the next wave of consumer dollars. The question is no longer whether tea will grow, but who will own the growth.

Verity Rank’s analysis, grounded in competitor research data and market projections, provides a clear lens into the forces reshaping this $40 billion-plus industry. From sourcing strategies to trend deployment, the insights below are designed to help B2B buyers verify suppliers and brands that can deliver on 2026 demands.

Industry application and market overview for Tea Beverage Category Report.

2. Market Analysis

The global tea beverage market is forecast to expand from approximately $40.2 billion in 2026 to $64.6 billion by 2034, according to industry projections. That represents a compound annual growth rate (CAGR) of 7.8%—well above the average for the broader Beverages & Mixes sector. Digging deeper, the new-type tea beverage segment (encompassing ready-to-drink premium teas, artisan blends, and functional infusions) is expected to grow at a slightly lower but still impressive 6.2% CAGR between 2026 and 2033.

Within the United States, the tea market is valued at $3.11 billion in 2025 and is projected to reach $3.78 billion by 2032, reflecting a stable, mature market that still offers pockets of high growth in premium niches. The two biggest growth drivers are the shift toward functional beverages and the mainstreaming of organic tea. Functional teas—those infused with protein, caffeine alternatives, or adaptogens—are capturing health-conscious consumers who previously gravitated toward energy drinks or coffee. Meanwhile, organic tea has exited the niche corner and now commands shelf space in mainstream retail and foodservice.

A third, often overlooked driver is the rapid expansion of new Chinese-style tea drinks. This sub-segment, characterized by fresh-brewed tea bases, milk foams, and customizable toppings, is driving significant volume in Asia and beginning to influence Western menus. The combination of premiumization, health halo, and cultural novelty is pushing category growth well above inflation. For B2B buyers, these numbers mean that sourcing contracts for organic matcha, caffeine-free rooibos, and protein-infused tea bases should be locked in now to meet 2026 demand.

Market segmentation and regional distribution for Beverages & Mixes - Tea Beverage Category Report.

3. Product Categories

The tea beverage category in 2026 is best understood through three distinct product sub-categories: Organic & Wellness Teas, Specialty Matcha Products, and Functional Loaded Teas.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

**Organic & Wellness Teas.** Organic is no longer a niche; it is a baseline expectation for many premium buyers. These teas include single-origin green, black, and herbal blends that carry third-party certifications. Caffeine-free options—such as rooibos, chamomile, and peppermint—are gaining traction as versatile alternatives for evening consumption or consumers sensitive to stimulants. Operators like those sourcing through Shamrock Foodservice Warehouse are increasingly demanding organic certification to meet both retail and foodservice specifications.

**Specialty Matcha Products.** Matcha is diversifying beyond the traditional ceremonial grade. We now see matcha used in lattes, smoothies, baked goods, and even savory applications. The trend is driving demand for both culinary-grade and premium stone-ground matcha. New Chinese-style tea drinks frequently feature matcha as a base or topping, and the U.S. market is following suit with matcha cold brews and matcha protein blends.

**Functional Loaded Teas.** Protein coffee made headlines, but loaded teas are the category’s next frontier. These are tea-based beverages fortified with protein powders, vitamins, or adaptogens. The data shows operators buzzing through 2026 by incorporating protein coffee into their tea menus—essentially creating cross-category hybrids. Loaded teas also include caffeine-free varieties with added electrolytes or collagen, targeting fitness and wellness audiences. For suppliers, this means offering multi-functional ingredient blends rather than single-note tea leaves.

4. Leading Players

**Shamrock Foodservice Warehouse** exemplifies the B2B distribution backbone of the tea beverage category. As a dedicated supplier of teas and coffees to foodservice operators, Shamrock positions itself as a one-stop shop for the latest trends—offering everything from decaf coffee to premium lattes and loaded tea bases. Their catalog reflects the convergence of coffee and tea trends, and they actively market product lines that align with the 2026 demands for unique flavors and functional ingredients.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the beverages & mixes space.

**alveus.eu** provides strategic market intelligence for the tea industry. While not a product manufacturer, alveus.eu’s trend reports—detailing organic teas, matcha diversification, and caffeine-free innovations—are used by buyers and suppliers to anticipate demand. Their 2026 forecast highlights that operators who ignore the organic and wellness shift risk falling behind. For B2B decision-makers, alveus.eu’s analysis serves as a trusted reference when vetting new supplier partnerships.

**Operators in the new Chinese-style tea drinks market** are reshaping the category’s product architecture. Although not a single named entity, this segment—fueled by chains and independent shops across Asia and now expanding globally—drives innovation in tea bases, toppings, and brewing methods. Their rapid growth, reflected in the market’s 6.2% CAGR, pressures traditional tea suppliers to develop fresh-brewed options and cold-brew concentrates that can mimic the artisanal experience at scale. These operators are a key customer group for B2B suppliers who want to capture the next-generation tea consumer.

5. Market Trends

1. ORGANIC TEAS Go Mainstream

ORGANIC TEAS Go Mainstream — Organic certification has transitioned from a premium differentiator to a category baseline. The data confirms that organic teas are no longer a niche market; they are a prerequisite for many foodservice and retail buyers. Why it matters: Operators who fail to source organic options will lose shelf space to competitors. Example: Shamrock Foodservice Warehouse lists organic teas as a core part of their 2026 lineup.

2. MATCHA Diversifies Beyond Ceremony

MATCHA Diversifies Beyond Ceremony — Matcha is appearing in lattes, smoothies, and even protein blends. The trend is diversifying the product SKU base from single-grade powders to functional matcha mixes. Why it matters: Matcha’s versatility allows operators to charge premium prices while appealing to both traditionalists and fitness-focused consumers. Example: New Chinese-style tea drink operators are incorporating matcha as a topping and base ingredient, driving demand for both culinary and premium grades.

3. CAFFEINE-FREE Options Gain Traction

CAFFEINE-FREE Options Gain Traction — Rooibos, herbal infusions, and decaf teas are finding new audiences among consumers seeking pleasure, well-being, and versatility—especially for evening consumption. Why it matters: Caffeine-free teas extend the daypart for operators, replacing soda and alcohol in some occasions. Example: The market data shows caffeine-free options as one of the top three trends for 2026, with projections that they will account for a larger share of the U.S. tea market.

4. Protein Coffee and Loaded Teas Converge

Protein Coffee and Loaded Teas Converge — The boundary between coffee and tea is dissolving as operators introduce protein-fortified versions of both. Loaded teas—tea + protein, vitamins, or adaptogens—are emerging as a distinct product type. Why it matters: This cross-category innovation opens new revenue streams for foodservice operators who can offer functional beverages at any hour. Example: Industry guidance from the Coffee and Tea Industry Trends report flags that operators can buzz through 2026 by incorporating protein coffee and loaded teas into their menu.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities stand out for B2B buyers in the tea beverage category. First, invest in organic and certified-sustainable supply chains now; by 2026, organic will be a non-negotiable entry barrier for foodservice contracts. Second, develop matcha-based functional blends (e.g., matcha protein powder, ready-to-drink matcha lattes) to capture the crossover between wellness and premiumization. Both moves align with the 7.8% CAGR and the U.S. market’s $3.78 billion target.

The primary risk is supply chain volatility for specialty tea leaves—particularly organic matcha and single-origin teas. As demand outpaces cultivation, prices could spike, squeezing margins for operators who haven’t locked in long-term supplier agreements. Verity Rank recommends using supplier verification tools to vet sourcing partners’ certifications, capacity, and delivery timelines before the 2026 surge fully materializes.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Tea Beverage Category Report Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-24. All market figures are estimates and may vary from actual results.