Table of Contents

The global Food Colors & Dyes Analysis sector serves consumers worldwide with diverse solutions.

1. Industry Overview

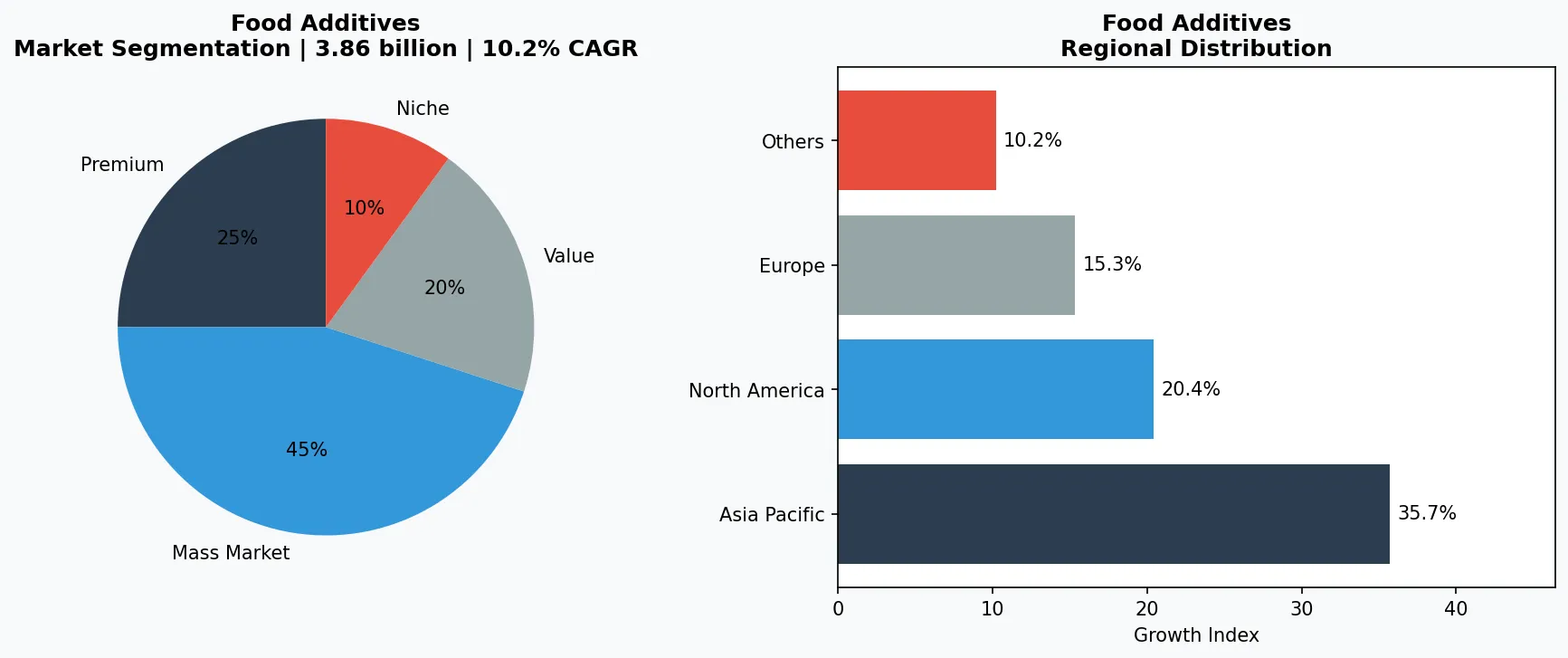

A single drop of synthetic Red 40 can color an entire batch of children’s candy, but it also carries a regulatory weight that is reshaping a $3.86 billion industry. The global food colors market, valued at that figure in 2026, is not just growing—it is fragmenting. Natural colors, nature-identical compounds, and petroleum-based dyes are competing for shelf space as consumer scrutiny intensifies. Within the broader food additives ecosystem, colors and dyes occupy a unique position: they are purely aesthetic yet psychologically powerful. Unlike preservatives or emulsifiers, which serve functional roles, colors are the silent salesmen of processed foods, influencing perception before a single bite. This sub-segment of Ingredients & Processing Aids now demands its own analytical lens, as the CAGR of 7.60% forecast from 2026 to 2034 hides stark divergences. Synthetic dyes, once dominant, now face a 10.2% CAGR surge in the United States alone—driven by both confectionery demand and reformulation pressures. Meanwhile, natural colors are racing to overcome supply-chain fragility. The market is valued at USD 4.32B in 2026 according to one estimate, but projections range from USD 5.9B by 2030 to USD 6.6B by 2033, reflecting data disagreements that underscore the sector's volatility. What is clear is that the analysis of food colors and dyes has become a strategic imperative for any B2B buyer navigating sourcing, compliance, and consumer trust.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Food Colors & Dyes Analysis, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Key market segments and growth drivers in the Food Colors & Dyes Analysis sector.

2. Market Analysis

The food colors market presents a mosaic of conflicting growth narratives, all pointing upward. According to one widely cited report, the global market size is USD 3.86 billion in 2026, with a projected compound annual growth rate (CAGR) of 7.60% through 2034, culminating in USD 6.94 billion. Another analysis pegs the starting point at USD 4.50 billion in 2026, climbing to USD 6.60 billion by 2033 at a 6.6% CAGR. A third source estimates USD 4.32 billion in 2026, targeting USD 5.9 billion by 2030 at an 8.1% CAGR. These disparities matter: they reflect different segmentation scopes—whether natural, synthetic, and nature-identical categories are included, and how geographic weighting is applied. The United States artificial food dyes segment is expanding at a striking 10.2% CAGR from 2026 to 2033, far outpacing the overall market, as domestic confectionery and beverage giants reformulate to meet state-level bans. The primary growth drivers are threefold. First, clean-label movements are accelerating the shift from petroleum-based dyes to plant-based alternatives, with natural colors expected to command over 60% of new product launches by 2028. Second, the Asia-Pacific region, particularly China and India, is seeing a surge in processed food consumption, pushing demand for both natural and synthetic colors. Third, supply-chain disruptions from 2020-2025 have forced manufacturers to invest in local sourcing and buffer stocks, inadvertently increasing per-unit costs but improving reliability. The single biggest wildcard remains regulation: the European Union's ongoing reassessment of titanium dioxide and azo dyes could compress the synthetic segment, while the U.S. FDA's delayed response creates a patchwork of state-level rules that complicate national distribution.

Market segmentation and regional distribution analysis for Food Colors & Dyes Analysis.

3. Product Categories

The food colors and dyes market is organized into three distinct product types, each with its own supply chain and application profile. **Natural colors** are derived from plants, animals, insects, or microorganisms. Examples include anthocyanins from purple carrots, carotenoids from paprika, and carmine from cochineal insects. Natural colors now represent the fastest-growing sub-category, driven by consumer demand for 'clean labels' and ingredient lists free of E-numbers. However, they suffer from lower stability to heat, light, and pH shifts, requiring additional encapsulation technologies. The natural colors market is particularly sensitive to supply-chain constraints as climate events impact crop yields—a theme dominating 2026-2036 outlooks. **Synthetic dyes** are petroleum- or coal-tar-derived compounds such as FD&C Red 40 and Yellow 5. Their cost-effectiveness, bright hues, and stability make them irreplaceable in high-volume applications like soft drinks, candy, and baked goods. Despite regulatory and consumer backlash, synthetic dyes still hold the largest volume share, especially in the United States and emerging markets. The U.S. artificial food dyes market is expanding at a 10.2% CAGR as manufacturers develop newer, less controversial synthetic alternatives. **Nature-identical colors** are chemically identical to natural compounds but produced synthetically—beta-carotene made via fermentation or chemical synthesis is a key example. They offer the best of both worlds: the natural chemical profile without the agricultural variability. This segment is niche but growing, particularly in premium dairy and sports nutrition products where consistency is critical. Each product type also comes in liquid, powder, and gel forms, with powders dominating dry mixes and liquids preferred for beverage emulsions.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The competitive landscape of food colors is anchored by a handful of multinational ingredient powerhouses, each pursuing distinct strategies. **Sensient Technologies** has doubled down on natural colors, investing in proprietary stabilization technologies that allow plant-based pigments to withstand high-temperature processing. Its acquisition of a Chilean paprika extractor in 2024 strengthened its position in the carotenoid segment, and the company now supplies over 70% of the natural red colors used in North American yogurt. **Chr. Hansen** (now part of Novonesis) focuses on microbial fermentation to produce nature-identical colors like beta-carotene and lycopene, offering a vertically integrated supply chain that bypasses agricultural risk. Their strategy targets the pharma-grade food sector, where batch-to-batch consistency is non-negotiable. **Kalsec** specializes in natural color extracts from herbs and spices—primarily turmeric, paprika, and rosemary—and has developed a proprietary emulsion system that improves dispersion in beverages. Their approach is to partner directly with growers in India and Africa, locking in supply and traceability. While none of these players disclose exact revenue splits by color type, their R&D pipelines suggest a clear pivot away from purely synthetic portfolios. A notable non-traditional entrant is **Meridian Researches**, which provides the market intelligence that many of these players use to guide investment decisions. As a research firm, it does not manufacture colors, but its reports shape the strategic choices of suppliers and buyers alike, making it an influential player in the ecosystem's information layer.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the food additives space.

5. Market Trends

1. 2. CLEAN-LABEL REGULATORY

2. CLEAN-LABEL REGULATORY CRACKDOWN

2. 3. SUPPLY-CHAIN RESHORING FOR NATURAL

3. SUPPLY-CHAIN RESHORING FOR NATURAL COLORS

3. 4. ARTIFICIAL DYE RESURGENCE IN

4. ARTIFICIAL DYE RESURGENCE IN CONFECTIONERY

4. CLEAN-LABEL REGULATORY CRACKDOWN — What it is: Governments

CLEAN-LABEL REGULATORY CRACKDOWN — What it is: Governments worldwide are restricting synthetic dyes, with California's 2023 law banning Red 3 and other additives in school foods, and the EU's EFSA re-evaluating titanium dioxide and azo dyes. Why it matters: These regulations force reformulation cycles, increasing demand for natural alternatives and raising compliance costs for ingredient suppliers. Example: Chr. Hansen has accelerated its microbial color platform to offer cost-competitive alternatives to banned synthetics.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two clear opportunities emerge for B2B buyers. First, investing in nature-identical colors produced via fermentation offers a hedge against both regulatory risk and agricultural supply shocks—Sensient and Chr. Hansen are already scaling these, and smaller players can license their technologies for regional production. Second, the 10.2% CAGR of the U.S. artificial dye market indicates that synthetic producers willing to invest in next-generation formulations (lower toxicity, better bioavailability) can capture premium pricing. The single concrete risk is the acceleration of state-level bans in the U.S. creating a fragmented compliance landscape that raises logistics costs and limits national SKU uniformity. Buyers should prioritize suppliers with dual natural and synthetic portfolios to maintain flexibility.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Food Colors & Dyes Analysis Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-29. All market figures are estimates and may vary from actual results.