Table of Contents

The global Fresh Milk Selection Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Are you sure the milk you are sourcing today will meet consumer demands tomorrow? The global fresh milk market, valued at $XX million in 2025, is on a trajectory that demands more than just a price check. By 2033, the industry is projected to expand at a compound annual growth rate (CAGR) of XX%, driven by shifting dietary patterns, clean-label preferences, and logistical innovations. Fresh milk, defined as raw or pasteurized milk that has not been ultra-high temperature (UHT) processed, sits at the center of the broader dairy and egg products segment—a sector that together with yogurt, cheese, butter, and eggs represents the backbone of daily nutrition for billions. What makes fresh milk selection distinctive is its perishability: unlike cheese or butter, it requires a cold chain that starts at the farm and ends at the retail shelf within days. This guide cuts through the noise to help B2B buyers—procurement managers, foodservice operators, and wholesalers—navigate the complexities of quality, shelf life, origin, and certifications. With the global dairy foods market alone projected to grow from $1,063.47 billion in 2026 to $1,995.47 billion by 2034, the stakes for making the right sourcing decision have never been higher.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Fresh Milk Selection Guide, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Key market segments and growth drivers in the Fresh Milk Selection Guide sector.

2. Market Analysis

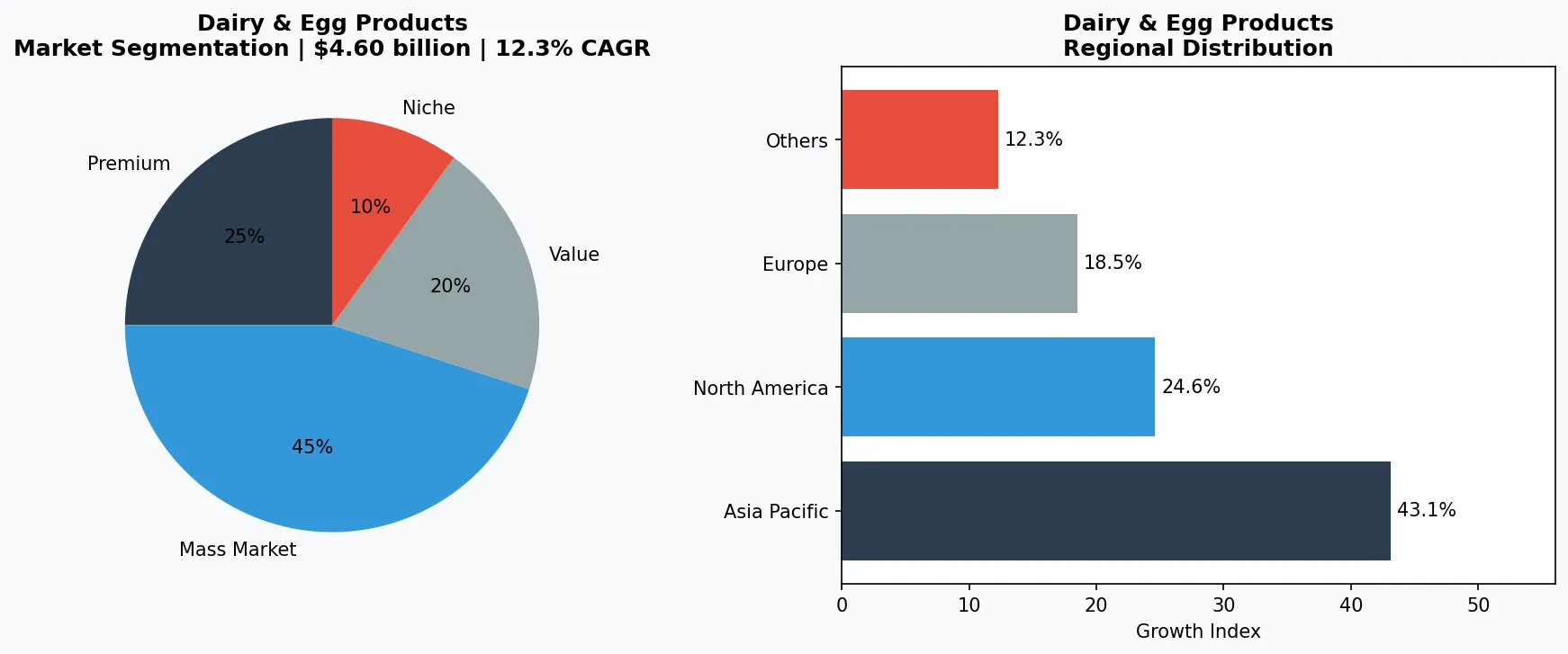

The fresh milk market operates within a larger dairy ecosystem that is experiencing robust expansion. According to recent forecasts, the global dairy foods market size will climb from $1,063.47 billion in 2026 to $1,995.47 billion by 2034, representing a CAGR of 8.18%. Within that, the fresh raw milk subsegment is expected to grow at an even faster clip—12.3% CAGR from 2026 onward. This growth is not uniform; it is being powered by three principal drivers. First, rising disposable incomes in Asia-Pacific and the Middle East are pushing consumers toward premium, pasteurized fresh milk over shelf-stable alternatives. Second, the dairy flavors market—valued at $4.60 billion in 2024 and forecast to hit $6.38 billion by 2030—is enabling product differentiation through flavored fresh milk offerings, which in turn expands the addressable market. Third, the 2026 outlook from the USDA Economic Research Service projects higher dairy exports on both milk-fat and skim-solids bases, driven by strong shipments in early 2026. For B2B buyers, these figures mean that competition for high-quality raw milk will intensify, making supplier verification—a core service of Verity Rank—more critical than ever. Buyers should also note that regional price volatility, particularly in Oceania and the EU, will require dynamic sourcing strategies rather than annual contracts.

Market segmentation and regional distribution analysis for Fresh Milk Selection Guide.

3. Product Categories

Fresh milk selection begins with understanding the distinct product categories available in the market. **Whole milk** (typically 3.25% fat) remains the gold standard for creaminess and is preferred by bakeries and confectionery makers. Its higher fat content makes it ideal for producing premium yogurt and cheese, but it also requires stricter temperature control to prevent spoilage. **Skim and low-fat milk** (0.5% to 2% fat) are driven by health-conscious consumers, especially in North America and Europe. These products often undergo fortification with vitamins A and D to compensate for fat removal, a critical specification for procurement teams. **Organic fresh milk** commands a premium of 30% to 60% over conventional milk, and its market share is growing at a double-digit pace in markets like Germany and the United States. Certifications such as USDA Organic or EU Organic must be verified at the source. **Lactose-free fresh milk** is the fastest-growing sub-category, fueled by rising awareness of lactose intolerance, particularly in Asian and African markets. Enzymatic hydrolysis processes break down lactose into glucose and galactose, altering sweetness—a factor that recipe developers must account for. For B2B buyers, each category requires distinct supplier audits: whole milk demands consistent fat tests, organic needs chain-of-custody documentation, and lactose-free requires batch-level enzyme activity validation.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

Three major dairy groups dominate the fresh milk sourcing landscape, each with distinct strategies. **Nestlé S.A.** leverages its global cold-chain infrastructure to supply fresh milk to foodservice clients under the Nestlé Professional brand. The company’s 2025 focus is on regenerative agriculture partnerships with dairy farms in Latin America, aiming to reduce carbon footprint by 20% per liter by 2027—a key selling point for sustainability-conscious buyers. **Danone S.A.** emphasizes probiotic fortification in its fresh milk products, tying its selection criteria to gut health claims. In 2024, Danone launched a dedicated fresh milk line in India under the 'Pro+’ label, targeting the 12.3% CAGR raw milk market in the region. For B2B buyers, Danone’s traceability platform—accessible via QR code on bulk containers—offers a model for supplier transparency. **Fonterra Co-operative Group Limited**, the New Zealand-based giant, controls approximately 30% of the global dairy trade. Fonterra’s strategy centers on seasonal supply reliability: its pasture-fed fresh milk supply, sourced from 10,000 member farms, peaks from October to February, creating an arbitrage opportunity for buyers who can store or process surplus during those months. Each of these players is investing in digital verification tools—aligning perfectly with Verity Rank’s mission to help businesses verify supplier credentials before committing to long-term contracts.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the dairy & egg products space.

5. Market Trends

1. 1. **COLD-CHAIN

1. **COLD-CHAIN TRANSPARENCY

2. **COLD-CHAIN TRANSPARENCY — ** Buyers are increasingly

**COLD-CHAIN TRANSPARENCY — ** Buyers are increasingly demanding real-time temperature logs for fresh milk shipments. Startups like FreshByte offer blockchain-based monitoring that logs every degree fluctuation from farm to factory. Why it matters: A single hour above 4°C can halve shelf life, turning a premium product into a liability. Fonterra has already integrated similar IoT sensors across 80% of its tanker fleet. **PLANT-BASED CROSSOVER |** Dairy companies are blending fresh milk with plant proteins (oat, almond) to create hybrid products that appeal to flexitarian buyers. Danone’s ‘Silk Nextmilk’ in the US combines cow’s milk with almond and oat, reducing per-liter cost by 15% while maintaining dairy’s nutritional profile. This trend is driving a new sub-segment in procurement: 'blended fresh milk’ with specific fat and protein ratios. **REGENERATIVE LABELING |** Carbon footprint labeling on fresh milk cartons is becoming standard in the EU, with mandatory Digital Product Passports expected by 2027. Nestlé has started printing a 'Farm Carbon Score’ on its La Laitière fresh milk in France, giving B2B buyers a tool to compare suppliers’ environmental impact. **MICRO-ULTRA PASTEURIZATION |** New high-pressure processing (HPP) technologies extend fresh milk’s shelf life from 14 to 45 days without UHT’s cooked flavor. Companies like Elmhurst 1925 are adopting HPP for their fresh milk line, enabling longer export routes. For Verity Rank users, verifying that a supplier uses HPP vs. standard pasteurization is now a key quality differentiator.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities stand out. First, the 12.3% CAGR in fresh raw milk demand, particularly in South and Southeast Asia, creates a window for early-entering importers who can secure long-term supply agreements with verified producers in New Zealand and the US. Second, the rising dairy flavors market ($6.38 billion by 2030) opens avenues for value-added fresh milk products—think mango-flavored pasteurized milk for the UAE or matcha-infused milk for Japan—that command 25–40% higher margins than plain milk. The primary risk is regulatory fragmentation: the EU’s new deforestation regulation, effective 2025, requires full traceability of dairy feed ingredients like soy. Suppliers that cannot prove their feed’s origin will be barred from export to Europe. B2B buyers must prioritize suppliers with verified feed audits—a service Verity Rank can streamline through its due diligence platform. The message is clear: fresh milk selection in 2026 is not just about fat content or price per liter—it is about verifiable supply chain integrity in a rapidly scaling market.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Fresh Milk Selection Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-25. All market figures are estimates and may vary from actual results.