Table of Contents

The global Natural Food Additives sector serves consumers worldwide with diverse solutions.

1. Industry Overview

$50.7 billion in 2026. $75.2 billion by 2033. That’s the trajectory of the natural food additives market, expanding at a compound annual growth rate of 7.3%. This sub-segment of the broader food additives industry—estimated at $135.44 billion in 2026—is outgrowing its synthetic counterparts, driven by an irreversible shift toward clean-label, recognizable ingredients. Natural food additives are substances derived from plants, animals, minerals, or microbial fermentation that perform the same functions as synthetic additives: preserving freshness, enhancing flavor, stabilizing texture, or adding color. What makes them distinctive is their provenance. Consumers today read ingredient decks with the same scrutiny as investors read balance sheets. A label listing “beet juice concentrate” instead of “Red 40” or “rosemary extract” instead of “BHA” signals trust. This isn’t a niche trend. The natural sub-segment is projected to grow at a 5.25% CAGR during 2026-2031 alone, as manufacturers worldwide reformulate to eliminate artificial chemicals. The food additive industry stands at an inflection point. Forces reshaping the industry—clean label demands, sustainability imperatives, and heightened regulatory scrutiny—are compressing the timeline for synthetic-to-natural transition. For B2B buyers in the Ingredients & Processing Aids segment, understanding the natural food additives landscape is no longer optional; it is a competitive necessity.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Natural Food Additives, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

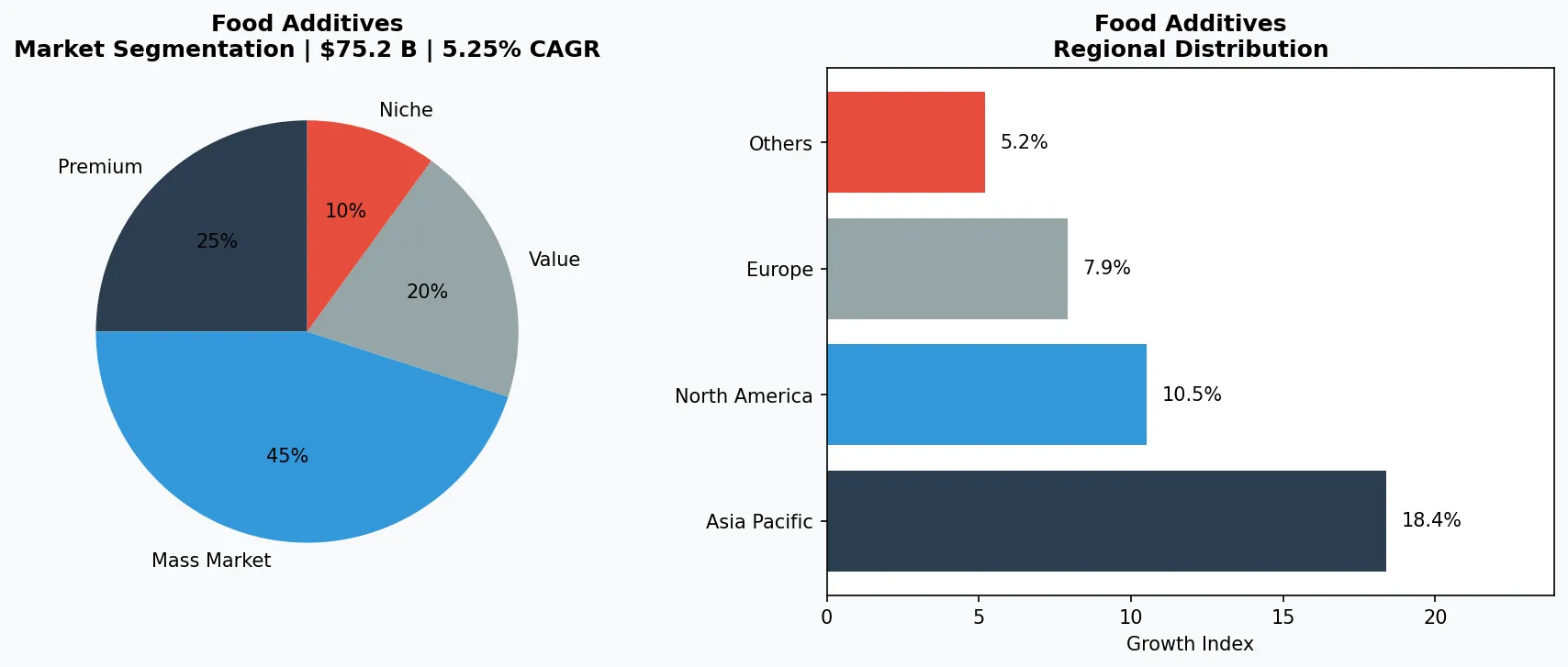

Key market segments and growth drivers in the Natural Food Additives sector.

2. Market Analysis

The global natural food additives market is projected to reach US$75.2 billion by 2033 from US$50.7 billion in 2026, expanding at a CAGR of 7.3%. This growth rate outpaces the overall food additives market, which is estimated to reach $203.65 billion by 2033 from $135.44 billion in 2026—meaning natural additives are capturing an increasing share of total spend. Three primary growth drivers underpin this acceleration. First, the clean-label movement. A 2025 consumer survey indicated that over 60% of global shoppers avoid products with artificial ingredients, directly fueling demand for natural preservatives, colorings, and flavor enhancers. Second, regulatory pressure. The European Union and North American agencies are tightening approvals for synthetic additives; in 2024, the EU further restricted titanium dioxide (E171) use, pushing confectionery and bakery producers toward natural alternatives like turmeric and paprika extracts. Third, cost parity gains. Advances in extraction and fermentation technology have lowered the price premium for natural additives from 40-50% a decade ago to 15-25% in 2025, making them accessible to mid-market brands. Regional dynamics favor Asia Pacific, which accounted for roughly 35% of natural additive consumption in 2025, led by China and India. However, North America shows the fastest per-capita growth, with natural flavor enhancers alone expanding at 8% annually as plant-based meat producers seek umami from yeast extracts and mushroom powders.

Market segmentation and regional distribution analysis for Natural Food Additives.

3. Product Categories

Natural food additives span multiple functional categories. **Preservatives** lead in volume, with rosemary extract and vinegar-based solutions replacing synthetic options like BHA/BHT. Rosemary extract, standardized for carnosic acid content, is now the go-to antioxidant for snack and meat processors. **Colorings** are the fastest-growing category, driven by consumer rejection of azo dyes. Beet juice (betanin), turmeric (curcumin), and spirulina extract now dominate red, yellow, and blue shades respectively in beverage and confectionery applications. **Flavor enhancers** are evolving beyond traditional yeast extracts. Fermentation-derived savory compounds from Aspergillus oryzae and lactic acid bacteria provide clean-label umami without monosodium glutamate labeling. **Sweeteners** represent a $12 billion sub-market, with steviol glycosides and monk fruit extract (mogrosides) leading growth. New enzymatic processing has reduced the bitter aftertaste of stevia, enabling 50% sugar reduction in carbonated soft drinks without compromising taste. Finally, **emulsifiers and stabilizers** are shifting from polysorbates to sunflower lecithin, acacia gum, and citrus fiber—ingredients that offer dual function as stabilizers and dietary fiber, appealing to the growing gut-health trend.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The natural food additives market is moderately fragmented, with a mix of global ingredient giants and specialized natural extract houses. **Leading multinational ingredient suppliers** are pivoting their R&D portfolios toward natural solutions, investing heavily in fermentation and plant extraction technologies. For instance, one major player launched a line of clean-label preservatives formulated with fermented rosemary and green tea extracts in 2025, targeting the $4 billion meat processing segment. **Specialized natural additive producers** focus exclusively on plant-based colorings and have carved out high-margin niches in organic candy and premium ice cream. Their strategy revolves around vertical integration—owning raw material farms for turmeric and beet—to ensure supply chain security and traceability. **Fermentation-focused biotech firms** are disrupting the flavor enhancer category by producing natural umami compounds through precision fermentation, achieving cost curves that undercut traditional yeast extract methods by 2027. **Regional champions** in Asia dominate supply of natural hydrocolloids like agar and gellan gum, leveraging local seaweed farming co-ops to offer price-competitive stabilizers for dairy-alternative beverages. These players collectively drive a competitive landscape where rapid innovation is rewarded, but strict regulatory adherence remains the key barrier to entry.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the food additives space.

5. Market Trends

1. 1. PLANT-BASED ADDITIVES

1. PLANT-BASED ADDITIVES SURGE

2. PLANT-BASED ADDITIVES SURGE — The use of plant-derived

PLANT-BASED ADDITIVES SURGE — The use of plant-derived additives is expanding beyond traditional herbs and spices. In 2025, new extraction techniques allowed water-soluble curcumin to be used in clear beverages, a segment previously closed to turmeric. This trend matters because it opens large-volume applications in sports drinks and flavored waters. Major beverage manufacturers are actively testing these formulations to replace artificial colors. TRANSPARENCY IN SOURCING | Blockchain-based traceability platforms now cover 20% of the natural vanilla supply chain, enabling buyers to verify origin and fair-trade status. This trend matters because natural additives command premium prices only when provenance is credible. One leading spice supplier implemented a QR-code system in 2024 allowing food manufacturers to audit every batch of natural extract. HEIGHTENED REGULATORY SCRUTINY | Global regulators are harmonizing definitions for “natural.” The FDA issued draft guidance in 2025 clarifying that “natural” cannot include highly processed derivatives, forcing reformulation of some fermented additives. This trend matters because it creates a temporary compliance cost but long-term competitive advantage for early adopters of minimal-processing methods.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities emerge for B2B buyers. First, the Asia-Pacific region offers 9% annual growth in natural additives as local food processors adopt global clean-label standards to export to Europe and North America. Suppliers who establish regional extraction facilities in Vietnam or India for spices and coconut-derived stabilizers can capture cost advantages. Second, the plant-based meat sector will consume over $1.5 billion in natural additives by 2029, specifically colorings that mimic meat browning and flavor enhancers that replicate animal umami. A key risk to weigh: supply volatility for raw botanicals. Climate events in 2024 reduced turmeric yields in India by 12%, causing price spikes for natural coloring. Buyers should negotiate multi-year contracts with volume flexibility and maintain a dual-sourcing strategy for critical additives like annatto and paprika extract.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Natural Food Additives Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-30. All market figures are estimates and may vary from actual results.