Table of Contents

The global Vitamin Fortification in Foods sector serves consumers worldwide with diverse solutions.

1. Industry Overview

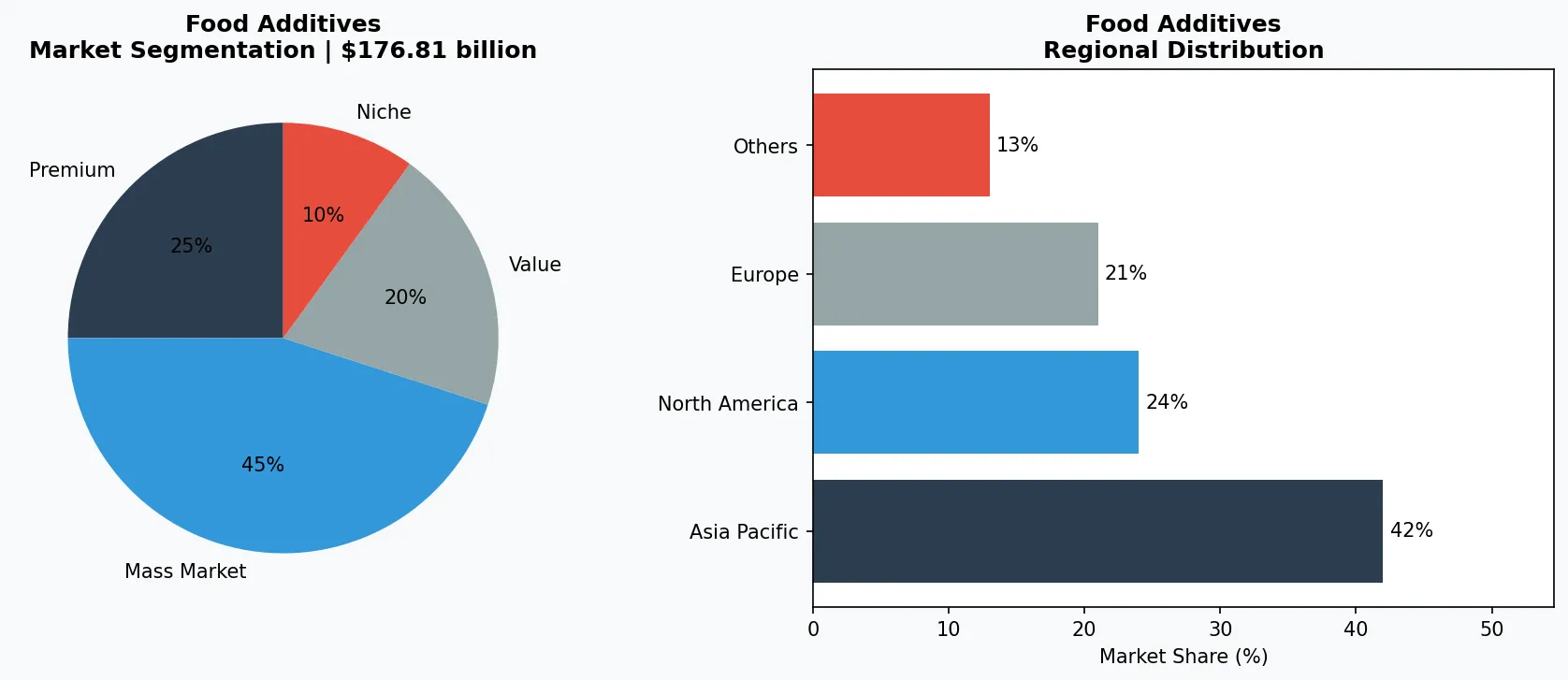

By 2026, one in every three packaged foods globally will rely on vitamin fortification, a market already valued at $176.81 billion. This is not a fringe niche—it is the fastest-growing segment within the food additives industry, projected to nearly double to $347.90 billion by 2034 at a compound annual growth rate (CAGR) of 8.83%. Vitamin fortification—the deliberate addition of essential micronutrients to staple foods and processed products—has moved from public health intervention to a core competitive strategy for food manufacturers. Unlike generic preservatives or colorings, fortification carries a dual promise: combating widespread micronutrient deficiencies while boosting product premiumization. The distinctive value lies in its ability to transform commodity foods into functional health carriers, appealing to both B2B buyers seeking differentiation and consumers demanding nutrient density. The Food Fortification Ingredients market alone is estimated at $15 billion and is on track to reach $25 billion, driven by regulatory mandates in over 80 countries and rising private-label innovation. For suppliers of food additives, this sub-topic represents a high-growth corridor where technical expertise in stability, bioavailability, and cost-effective premix solutions directly determines market share.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Vitamin Fortification in Foods, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Key market segments and growth drivers in the Vitamin Fortification in Foods sector.

2. Market Analysis

The global fortified foods market is projected to grow from $176.81 billion in 2026 to $347.90 billion by 2034, reflecting an 8.83% CAGR. This dramatic expansion is not a single-speed story—divergent growth rates reveal nuanced dynamics. Future Market Insights forecasts a 6.4% CAGR from 2026 to 2036, while other analysts peg a 5.3% annual growth between 2026 and 2033. The variance highlights two powerful drivers: mandatory fortification policies in developing economies and voluntary premium fortification in mature markets. The first driver is regulatory momentum. Nations like India, Nigeria, and Indonesia now mandate fortification of wheat flour, edible oils, and milk with vitamins A and D. This creates a stable, volume-driven demand for vitamin premixes. The second driver is the rise of functional foods in North America and Europe, where consumers actively seek out products with added vitamin D, B12, and folic acid for immunity and energy. Consequently, vitamin premixes—the core ingredient for cost-effective fortification—are expanding at a 6.5% CAGR from 2026 to 2033. B2B demand for ready-to-use premixes is soaring as manufacturers shift from in-house blending to specialized suppliers to reduce complexity and costs. The bottom line: the vitamin fortification market is now bifurcated between volume-driven government contracts and value-driven consumer goods, each demanding different additive formats and supply chain capabilities.

Market segmentation and regional distribution analysis for Vitamin Fortification in Foods.

3. Product Categories

Vitamin fortification spans three distinct product categories, each with specific applications within the food additives industry. First, single-nutrient premixes dominate staple fortification. Vitamin A palmitate is the most common additive in cooking oils and margarine, while vitamin D3 is added to dairy and plant-based milks. These premixes are typically oil-soluble and require encapsulation for stability—a technical challenge that drives B2B sourcing of specialty carriers. Second, multi-vitamin blends are the workhorses of breakfast cereals, energy bars, and infant formulas. These combinations often include B vitamins (thiamine, riboflavin, niacin), folic acid, and iron, formulated to meet specific regulatory standards (e.g., U.S. FDA enrichment guidelines). Third, novel fortification formats are emerging: water-soluble vitamin C and B-complex are now being microencapsulated for use in clear beverages and gummies—a trend that opens new opportunities for flavor enhancers and stabilizers within the same supply chain. For ingredient buyers, the key differentiator is not just the vitamin itself but the delivery system. A poorly stabilized vitamin premix leads to degradation and off-flavors, making carrier technologies (emulsifiers, antioxidants) as critical as the active nutrients. The market for these auxiliary additives is growing in lockstep with fortification demand.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The vitamin fortification supply chain is concentrated among a handful of global ingredient giants and specialized premix houses, though the competitive landscape is fragmenting rapidly. The largest players control the raw vitamin production—an oligopoly that sets base pricing globally. Their strategy focuses on vertical integration and cost leadership, producing bulk vitamins A, D, and E at scale. For B2B buyers, these suppliers offer reliability and regulatory compliance but limited customization. A second tier of players specializes in custom premix manufacturing. These companies differentiate through rapid formulation, clean-label options (non-GMO, organic carriers), and just-in-time delivery. They are the primary beneficiaries of the 6.5% CAGR in premix demand, as food brands increasingly outsource fortification blending to reduce inventory risk. A third emerging cohort includes regional producers in Asia-Pacific and Latin America, who combine lower labor costs with growing local regulatory mandates. These players are capturing the volume-driven government contracts for wheat flour and rice fortification. The competitive edge in this market no longer lies in vitamin synthesis alone—it has shifted to service: technical support for stability testing, label claims, and halal/kosher certifications. Ingredient buyers should prioritize suppliers with proven track records in their specific end-use application, whether beverage, bakery, or dairy.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the food additives space.

5. Market Trends

1. CLEAN LABEL FORTIFICATION

CLEAN LABEL FORTIFICATION — Consumers are demanding fortification without synthetic additives, pushing suppliers toward natural-source vitamins (e.g., vitamin D from lichen, beta-carotene from algae) and organic-compliant carriers. This trend raises formulation complexity but allows brands to command premium pricing. Major premix suppliers now offer 'clean label' portfolios that replace synthetic antioxidants with natural tocopherols.

2. MICROENCAPSULATION TECHNOLOGY

MICROENCAPSULATION TECHNOLOGY — To solve stability and taste challenges, microencapsulation is becoming a standard requirement in B2B vitamin premixes. Encapsulated vitamin C and B12 are now used in shelf-stable clear beverages and confectionery, preventing oxidation and masking bitterness. This trend directly increases demand for emulsifiers and stabilizers as encapsulation matrix materials.

3. BIOFORTIFICATION VS. ADDITIVE FORTIFICATION

BIOFORTIFICATION VS. ADDITIVE FORTIFICATION — A rising alternative to synthetic fortification is biofortification—breeding crops with higher inherent vitamin content (e.g., vitamin A-rich sweet potatoes, iron-fortified beans). While this competes with traditional additive fortification, it also creates a parallel market for food additives used in post-harvest processing. The two approaches are converging; for instance, biofortified grains may still require folic acid or vitamin D premixes in finished products.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two clear opportunities define the 2026-2034 horizon. First, the explosion of plant-based and alternative protein products creates a massive fortification gap. Dairy alternatives routinely lack vitamin B12 and D, making them prime targets for premix suppliers—a market estimated to add $7-10 billion in incremental additive demand. Second, personalized nutrition is moving from niche to mainstream; B2B buyers will increasingly demand modular premixes that allow brands to offer 'build-your-own-fortification' for subscription meal kits or custom beverage powders. The concrete risk is regulatory fragmentation. The European Union is tightening permissible vitamin levels (e.g., vitamin A upper limits), while the U.S. FDA is re-evaluating fortification waivers for novel foods. Ingredient buyers must invest in regulatory intelligence and flexible formulation capabilities to avoid costly reformulations or market access bans. The winners will be those who treat vitamin fortification not as a commodity additive but as a strategic platform for product innovation and compliance.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Vitamin Fortification in Foods Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-30. All market figures are estimates and may vary from actual results.